Polypropylene Weekly Review: Geopolitical Tensions Drive Market Rollercoaster

I. Key Market Focus Points This Week

Production: This week, the output of polypropylene in China was 722,600 tons, a decrease of 45,700 tons from last week's 768,300 tons, a decline of 5.95%; compared to the same period last year's 777,400 tons, it decreased by 54,800 tons, a decline of 7.05%.

In terms of demand: This period, the overall operation rate of the downstream industries of polypropylene has increased slightly. The operation rates of plastic weaving, BOPP, PP pipes, and transparent PP industries have risen, while the rest have declined. BOPP companies are actively delivering previous orders, increasing their operation rate; the plastic weaving industry, benefiting from the approaching spring fertilizer preparation, sees an increase in the demand for fertilizer bags, coupled with an increase in the use of cement bags, leading to a significant rise in the operation rate; the demand for PP pipes has increased with the resumption of infrastructure construction; large and medium-sized enterprises in the transparent PP sector have stable orders, and their operation continues to improve. The daily injection molding, PP nonwoven, CPP, and modified PP industries are significantly affected by the substantial increase in costs, with limited capacity to follow price increases and poor price transmission, leading to a decrease in their operation rates. The overall performance of the downstream industries is mixed, with rising costs restraining the enthusiasm for operation. It is expected that the overall operation of the downstream industries may slightly decline next week.

In terms of inventory: As of March 11, the total commercial inventory of polypropylene in China was 938,400 tons, a decrease of 10,800 tons from the previous period, down 1.13% month-on-month. Among these, the inventory of producers increased 0.38% month-on-month, the inventory of traders decreased 3.08% month-on-month, and the inventory of port warehouses decreased 8.23% month-on-month. By grade, the inventory of filament grade decreased 8.28% month-on-month, and the inventory of fiber grade decreased 13.97% month-on-month.

II. Review of This Week's Market Trends

Source: Longzhong

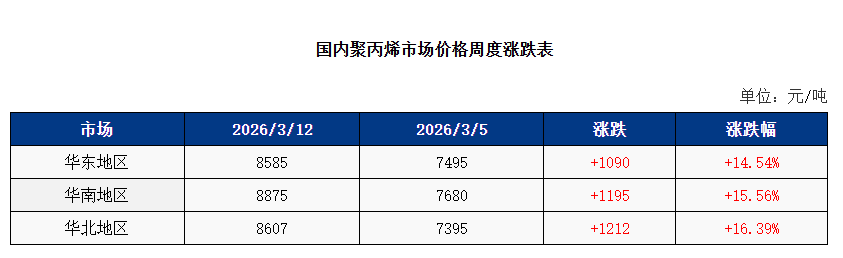

This week, the polypropylene market experienced a rollercoaster trend dominated by the Middle East geopolitical situation. Spot prices in the East China, South China, and North China regions all saw significant increases. The average price in East China was 8,585 yuan/ton, up 1,090 yuan/ton from last week, a rise of 14.54%. The average price in South China was 8,875 yuan/ton, up 1,195 yuan/ton from last week, a rise of 15.56%. The average price in North China was 8,607 yuan/ton, up 1,212 yuan/ton, a rise of 16.39%. As of the 12th, the national average price for granulate was 8,657 yuan/ton, up 1,163 yuan/ton from last week, a rise of 15.52%.

At the beginning of the week, geopolitical tensions escalated, logistics through the Strait of Hormuz were disrupted, and refining facilities in the Middle East were impacted, weakening market expectations for de-escalation and tightening supply expectations for energy, thereby driving up international crude oil prices. Polypropylene prices surged in tandem, with a single-day increase of RMB 2,061 per ton. Later, as the Middle East situation eased temporarily, international oil prices retreated, prompting polypropylene prices to adjust downward rapidly; producers slashed prices by RMB 1,600 to 2,000 per ton in a single day, and spot prices followed suit. Following this sharp volatility, market speculation subsided, and industry participants adopted a more cautious, wait-and-see stance. The market entered a phase of high-level consolidation, focusing in the near term on absorbing the recent volatility and reverting to fundamentals.

III. Market Forecast for Next Week

It is expected that the polypropylene market will mainly experience fluctuation to digest the price increase next week, with opportunities for further price exploration. More upstream refineries are taking preventive measures to reduce loads, providing strong support from the cost side, and the market focus is likely to shift upwards. However, the downstream sector finds it difficult to pass on the high cost of raw materials, limiting the progress of transactions.

The key points focus on three aspects: first, supply continues to shrink, with the scope of plant shutdowns and reduced capacity expanding from South China to East China, further increasing supply pressure; second, demand is gradually recovering, with downstream production increasing, but price volatility is intensifying, adding procurement pressure on the downstream; third, the cost side remains strong, with expectations of tight oil supply pushing oil prices higher, and high import costs of propane keeping PDH cost support strong.

Overall, the polypropylene market is expected to fluctuate with an upward bias next week, presenting opportunities for price increases.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Middle East Tensions Escalate Sharply: How Polyolefins Respond Amid Soaring Risk Premium

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

LG Chem Declares Force Majeure on DOTP Exports! SABIC Joins Five Giants to Redefine EV Safety