Polyester Inventory Under High Pressure, Structural Differentiation In May Market

The first round of U.S.-Iran talks in April failed to reach consensus, causing significant fluctuations in international crude oil prices. The trading logic in the polyester raw materials market gradually shifted from cost-driven to supply-expectation-driven, as the polyester market also transitioned from cost support to a supply-demand imbalance-driven dynamic. By the end of April, downstream weaving enterprises' willingness to restock continued to weaken, while demand from the soft drink sector steadily recovered, leading to divergent trends in the polyester market. Looking ahead to May, crude oil will still provide some cost support, but end-demand will remain divergent, likely resulting in a distinctly structural market pattern for polyesters.

Amidst geopolitical tensions, polyester raw materials surged and then fluctuated in April, but the textile terminal "Silver April" peak season was below expectations. At the end of the month, the polyester market showed a divergent trend. Polyester companies actively reduced production to support the market, leading to a relatively mild decline in raw material and finished product prices, while the price of conventional gray cloth fell faster. At the end of the month, the pressure on new order negotiations for weaving increased. To avoid the risk of raw material and inventory devaluation, some weaving companies collectively shut down before the May Day holiday, and the negative demand feedback was transmitted upstream, leading to a continuous accumulation of polyester finished product inventory. Looking ahead to May, rising temperatures may drive a marginal improvement in non-fiber demand, but as the traditional textile peak season nears its end and cost pressures persist, it will be difficult for terminal demand to substantially recover, and the pressure on polyester inventory reduction remains high.

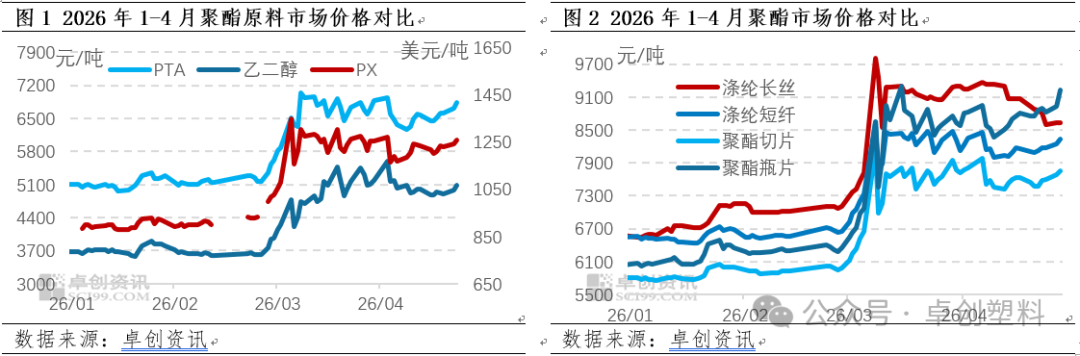

4Monthly polyester raw material market fluctuates widely, polyester price trends show divergence.

In April, the trading logic of the polyester industry chain shifted, leading to market price differentiation. The price center of the entire industry chain moved upward synchronously. Although the first round of talks between the US and Iran did not reach a consensus, both sides released signals of continued dialogue, leading to a cooling of risk-aversion sentiment. The market's main driving logic gradually shifted to supply and demand patterns, cost transmission, and export performance. In late April, the price trends of industry chain products became more diversified: upstream ethylene glycol fluctuated downward, while PX and PTA showed strong resistance to declines. On the product side, polyester filament prices continued to fall, while polyester bottle resin prices fluctuated strongly upward. Looking at individual products, ethylene glycol prices were under pressure due to increased coal-based plant operations and increased import arrivals, leading to an overall surplus in the market. PX and PTA, however, saw a clear expectation of supply contraction due to concentrated maintenance of facilities, supporting their strong resistance to price declines. On the demand side, both domestic and foreign demand for textile and clothing remained weak, with polyester filament companies mainly adopting price reductions to promote sales, leading to continuous price declines. Polyester bottle resin, on the other hand, benefited from improved overseas demand, with order transfers from the Middle East due to regional conflicts, along with a recovery in domestic demand driven by rising temperatures, jointly driving the strong rebound in bottle resin prices.

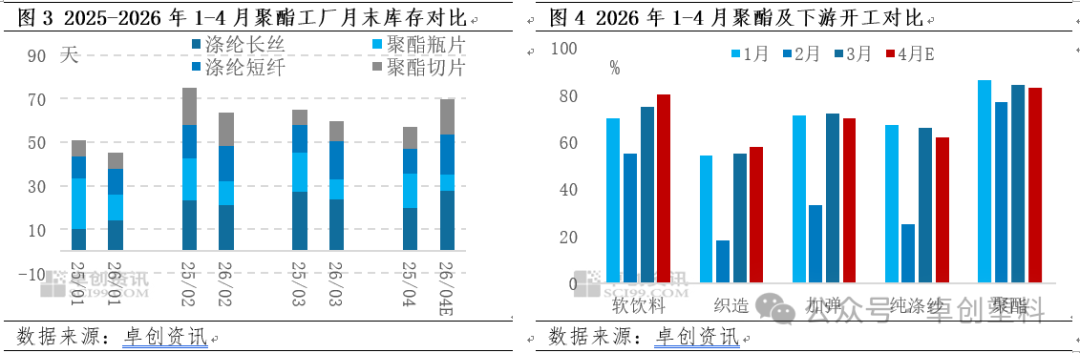

4Monthly accumulation of polyester products, polyester market demand is diverging

In April, the polyester industry shifted from destocking to restocking, with most polyester products experiencing inventory buildup, except for polyester bottle chips, which continued the destocking trend. According to statistics from Zhuochuang Information, as of April 24, the end-of-month inventories of polyester filament yarn, polyester staple fiber, and polyester chip all showed a sequential increase, while the inventory of bottle chips remained low and stable. The main reasons are: due to the wide fluctuation in costs, new orders for grey cloth were insufficient, and the downstream textile market experienced a peak season that was not as strong as expected; as the "Silver April" neared its end, the operating rate of weaving did not rise but fell; moreover, the average operating load of draw-texturing and pure polyester yarn in April also showed a significant sequential decline, leading to a slowdown in the demand for polyester products such as polyester filament yarn and polyester staple fiber, forcing enterprises to restock. On the other hand, the soft drinks market maintained a high level of activity, with the operating rate steadily rising to around 80% in April. Along with the demand for summer and holiday stockpiling, this supported a robust demand for polyester bottle chips, leading to continuous destocking. Overall, the downstream demand for polyester exhibited a divergent trend, with "textile and apparel weakening, and beverages remaining strong."

5Monthly cost support remains relatively strong, but the polyester market exhibits structural divergence.

In May, the two raw materials for polyester still have room for upward movement, with overall cost support for the industry remaining relatively strong. Currently, the Middle East peace talks are progressing slowly, and the recovery of international oil supply is proceeding at a sluggish pace. Coupled with the imminent onset of the U.S. summer driving season—characterized by heightened fuel demand—crude oil has demonstrated notable resilience against price declines, providing strong positive impetus to polyester feedstocks. By product type: PTA prices are supported indirectly by the stalled geopolitical negotiations and disrupted logistics through the Strait of Hormuz, which have tightened crude oil supply. Additionally, concentrated plant maintenance has accelerated industry-wide inventory drawdowns, making a bullish trend highly probable for May. The average monthly price is expected to reach RMB 6,650/ton, up 1.13% month-on-month. Ethylene glycol (EG) prices remain closely tied to the Middle East situation; delayed progress in peace talks continues to disrupt imports and feedstock supply, further strengthening expectations of inventory drawdowns and providing modest upward price momentum. However, once risk premiums dissipate, a relatively pronounced correction is anticipated. Thus, EG prices are expected to rise initially before declining in May, with the average monthly price projected at RMB 4,750/ton, down 5.85% month-on-month. Overall, underpinned by Middle East geopolitical developments and seasonal strength in crude oil demand, short-term cost support for the polyester industry remains robust, albeit with structural divergence.

On the supply and demand side, overall polyester operating rates in May have limited room for improvement, while downstream demand has weakened locally, resulting in a relatively weak industry supply-demand fundamental. Major polyester producers’ production cut plans will continue through the end of June. Affected by divergent profitability across product categories, only PET bottle-grade chip operating rates are expected to rise modestly, while operating rates for other varieties remain largely stable; industry-wide operating rates are expected to stay slightly above 80%. However, the resumption of a 360,000-ton production facility earlier this year and the commissioning of a new 300,000-ton facility in early May will still drive a moderate increase in market supply. On the demand side, domestic textile and apparel consumption is gradually weakening, while export orders face high uncertainty this year. Post-Labor Day holiday, the recovery in weaving and texturing plant operating loads has lagged behind previous years; weaving plant operating rates are expected to rebound to 63%, and texturing plant operating rates to 78%. Meanwhile, as the soft drink consumption season enters its peak, downstream capacity utilization for PET bottle-grade chips is expected to rise to 85%, returning to levels typical for this time of year.

Overall, the boosting effect of geopolitical conflicts on the polyester market in May will gradually weaken, and market dynamics will revert to supply-demand fundamentals. Downstream industries’ ability to absorb raw material cost increases will determine the fluctuation range of polyester prices. Under the combined influence of cost support and supply-demand conditions, the polyester market in May is expected to maintain a structurally differentiated pattern, with relatively strong price floor support. By product type: PET bottle-grade chips exhibit strong willingness to follow raw material price increases, and supported by steady demand, prices are expected to rise notably, with an average monthly price forecast at RMB 9,050/ton, up 3.48% month-on-month; polyester filament, backed by industry-wide production cuts and promotional sales strategies, is expected to enter a phase of steady price recovery once enterprises successfully shift inventory to downstream weaving sectors, with an average monthly price forecast at RMB 8,907/ton, down 1.63% month-on-month.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

First Time Surpassing $3 Billion! First Time Surpassing 100,000 Tons! Cathay Biotech’s 2025 Performance: Chemical Production Fully Phased Out, Biological Method Wins

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Completion And Commissioning! Evonik’s Four Major Projects Officially Launched