Oil Prices Break 100! PA6 Enters Strong Rally

Recent tensions in the Middle East have continued to escalate, with the US-Iran confrontation intensifying and the risk of navigation in the Strait of Hormuz increasing. The disruption of the strait has directly led to a substantial interruption in oil supply. Major oil-producing countries such as Iraq and Kuwait have begun to cut production, while the UAE is also facing storage saturation pressure, forcing it to manage its production levels. As a result, international oil prices have surged, with Brent crude oil temporarily breaking through the $100 per barrel threshold.

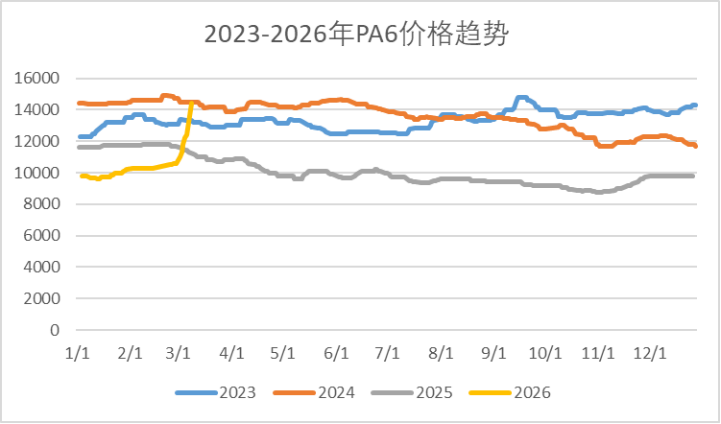

For PA6, the core driver of price volatility lies in cost pass-through. A sharp surge in crude oil prices has rapidly transmitted downstream, causing pure benzene prices to follow oil prices in a "six-week consecutive rise." Caprolactam, the direct raw material for PA6, has seen a significant price jump due to substantially higher production costs. Data shows that as of March 9, the market price of caprolactam in East China had risen to RMB 11,700 per ton, with a single-day increase of RMB 500 per ton, serving as the primary catalyst for the PA6 price hike.

From the current market performance, cost-driven factors and the synergy of supply and demand have driven the price of PA6 to rise significantly. As of March 9, the market quotation for conventional spun PA6 with bright fiber is between 15,000 and 15,800 yuan/ton, with a single-day increase of about 2,000 yuan/ton. In terms of specific varieties, the mainstream price of high-speed spun chips has risen to 15,000–15,000 yuan/ton, with a single-day increase of 2,250 yuan/ton. On the supply side, the current operating rate of the PA6 industry is around 73%, with some facilities under maintenance, and the overall inventory of finished products at factories is relatively low. More importantly, polymer factories had a large order intake before the Spring Festival, and there are still pending orders after the holiday, leading to a strong sense of price support and reluctance to sell among manufacturers. Some factories have even limited new orders, further supporting the price increase. On the demand side, the operating rate of the downstream textile industry has recovered to around 70%, entering the post-holiday inventory replenishment period, with spot purchases effectively supporting the price. Although high prices have restrained speculative buying, they have not undermined the upward trend.

It should be noted that while PA6 prices are rising, the industry's own structure and macroeconomic risks still need to be monitored. Currently, the domestic PA6 industry is facing structural overcapacity, with an adequate supply of mid-to-low-end products, while only high-end products have a gap. If the conflict eases and oil prices fall, the cost support will weaken, and PA6 prices may decline. Additionally, concerns about global "stagflation" are rising, with soaring oil prices suppressing consumption and corporate profits. If downstream demand recovery falls short of expectations, high prices will be difficult to sustain, thus limiting the upward space for PA6 prices.

Looking ahead, the Middle East situation has become the dominant factor influencing PA6 prices. In the short term, the geopolitical conflict is unlikely to subside quickly, and the blockade of the Strait of Hormuz is evolving from “logistical delays” into “actual supply disruption.” Institutions such as Goldman Sachs have warned that if Strait throughput remains persistently low, oil prices could approach historical highs. Against this backdrop, the cost-driven pricing logic remains robust. Combined with low inventory levels at PA6 production facilities and strong pricing-support intentions, PA6 market prices are expected to continue rising, with potential short-term upward pressure of RMB 200–300 per ton.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

LG Chem Declares Force Majeure on DOTP Exports! SABIC Joins Five Giants to Redefine EV Safety

-

Tao Lin: Tesla’s Supercharger Stations in China Surpass 2,500