Middle East Triggers Supply Chain Tsunami: Plastic Orders Cut Off

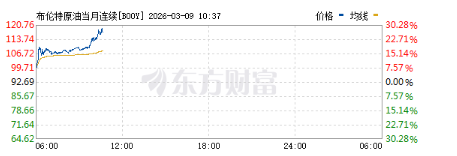

The Strait of Hormuz is engulfed in flames, nearly severing the global energy lifeline. WTI crude oil surges by 25% to break through $114 per barrel, while Brent crude climbs to over $110. This is not just a leap in numbers; it is a survival test that the Chinese plastic and coatings industries are undergoing. From "quote per order" to "suspension of sales," and from "razor-thin margins" to "deep losses," the upstream and downstream of the industry chain are undergoing a stress test of the utmost intensity.

"De-supply" Shockwave: Supply Chain Faces a Hard Break

The Strait of Hormuz—the vital artery for one fifth of global oil tanker traffic—now sees its daily oil flow drop by about 90%, equivalent to 18 million barrels of supply vanishing overnight.

What's even more frightening is that the chain reaction is accelerating: Iraq has cut 1.5 million barrels per day of supply, Kuwait has declared force majeure, and Qatar's world's largest LNG export facility has been completely shut down... JPMorgan warns that the scale of supply disruptions in the Gulf region could exceed 4 million barrels per day by this weekend, approaching 6 million barrels per day.

Alternative pipeline capacity is limited and has been attacked, onshore storage can only support for 22 days, and offshore floating storage is about to be depleted. Goldman Sachs warns: if the situation does not ease, the probability of oil prices breaking through $100 next week will significantly increase, and if it remains blocked in March, it could challenge the historical high of 2008.

Crude oil, the mother of the chemical industry, is now unleashing a “supply disruption storm” that is sweeping through China’s plastics and coatings industries with overwhelming force.

Plastic: From "Protecting Profit" to "Protecting Survival"

Crude oil, as the origin of the chemical industry chain, has seen its price volatility quickly transmitted to China's plastic market. For example, polypropylene futures have seen consecutive daily limits, with the main 2605 contract reported at 7,223 yuan/ton on March 3, a 5.99% increase; the spot price of draw-texturing grade in East China rose by more than 410 yuan within two days, reaching 7,050-7,200 yuan/ton.

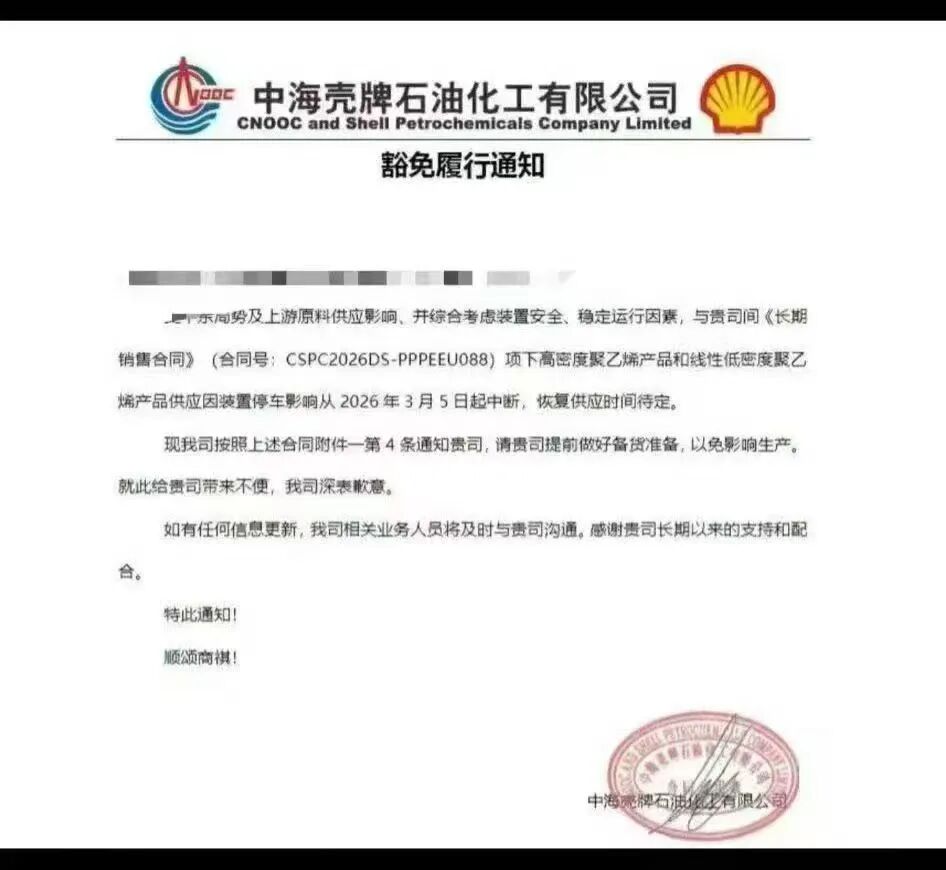

In terms of polyethylene, CNOOC and Shell Petrochemicals has officially notified its customers that due to the interruption of upstream raw material supply, the supply of high-density polyethylene and linear low-density polyethylene will be suspended starting from March 5, and the time of resumption is yet to be determined.

PVC prices have risen by more than 12% year-to-date, making it one of the strongest-performing general-purpose resins. Against this backdrop, some traders have opted to halt sales, further heightening market uncertainty.

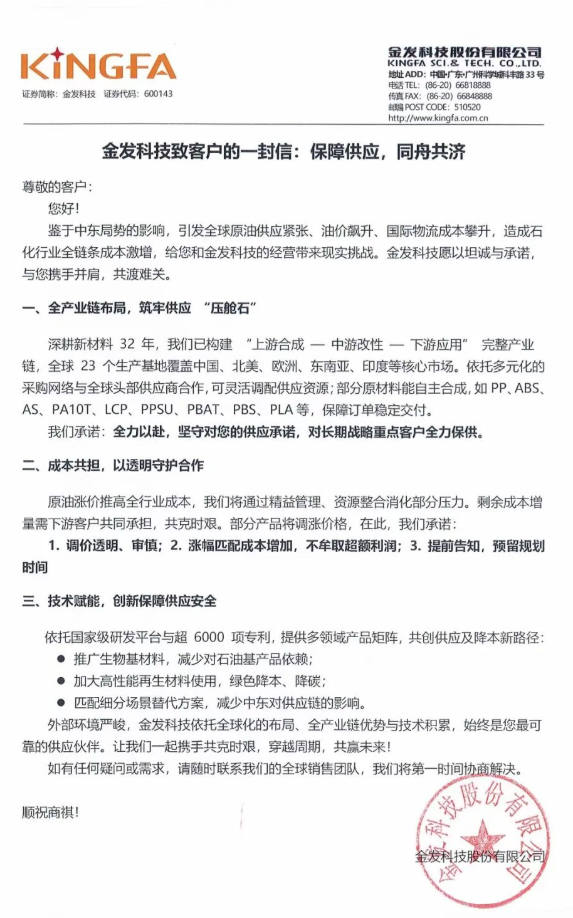

In response to this situation, some leading material companies have begun to take measures to stabilize expectations. For example, Kingfa Sci. & Tech. stated that it will ensure supply commitments to strategic customers, make the price adjustment process transparent and cautious, and reduce dependence on oil-based raw materials by promoting the use of bio-based materials and increasing the proportion of recycled materials.

Paint: The Crimson Twilight of Architectural Coating Emulsion

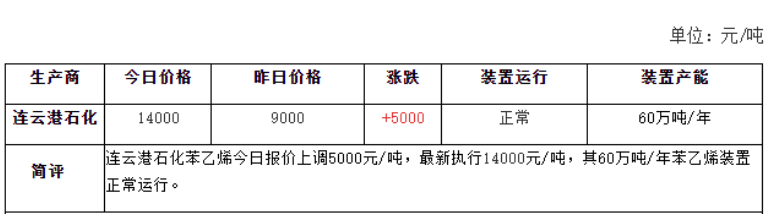

According to the latest market data, key monomer prices have surged dramatically: styrene has risen by over RMB 1,500 per ton compared to the same period last month; MEK (methyl ethyl ketone) has increased by approximately RMB 2,500 per ton; isooctyl acrylate by roughly RMB 2,000 per ton; and MMA (methyl methacrylate) by around RMB 1,700 per ton. These sharp increases have been rapidly passed through to the emulsion segment, with styrene-acrylic emulsions seeing a cost increase of about RMB 800 per ton and pure acrylic emulsions a cost increase of approximately RMB 2,000 per ton. Based on current raw material prices, the gross margin for most emulsion products has turned negative.

Due to raw materials being priced "daily" and supply-side price control, emulsion manufacturers are facing significant delivery losses on previously locked-price orders. This is the current reality of the coatings industry: earlier orders are turning into profit-sucking black holes.

Faced with a matter of survival, dairy companies have implemented strict controls: abandoning long-term contract pricing and fully shifting to "daily negotiation and order-by-order pricing," thereby passing cost risks downstream in real time. They are enforcing mandatory procurement based on actual needs and strictly prohibiting sales at zero margin. Winter stockpiling and fixed-price orders will be canceled outright if a deposit has not been paid or if delivery is not taken on time.

Outlook for the Future: When Will the Storm Subside?

Goldman Sachs estimates that if the Strait remains blocked through March, oil prices could challenge the 2008 historical highs. Qatar's Energy Minister and Macquarie Investment Bank have warned that if the conflict is not quickly resolved, the crude oil market could collapse within days, driving prices above $150 per barrel or even higher.

This means that cost pressures in the plastics and coatings industries are far from peaking.

For industry professionals, the current situation has entered a “wartime state”—the core contradiction has shifted from “insufficient demand” to “uncontrollable costs and supply disruptions.” Leading enterprises have built moats through vertical integration and financial hedging, whereas the majority of small and medium-sized enterprises (SMEs) face a dilemma: raising prices risks losing customers, while not raising prices leads to losses and potential bankruptcy.

This supply chain storm, triggered by geopolitical factors, is accelerating industry reshuffling; enterprises that respond more swiftly in terms of cost pass-through mechanisms, supply chain resilience, and technological substitution pathways will be more likely to survive this extreme stress test.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

LG Chem Declares Force Majeure on DOTP Exports! SABIC Joins Five Giants to Redefine EV Safety

-

Tao Lin: Tesla’s Supercharger Stations in China Surpass 2,500