Middle East Conflict Sparks Global Polypropylene (PP) Price Surge, With Asia Seeing Largest Increase

According to data from S&P Global Energy’s Platts, global polypropylene (PP) prices have risen across the board since March, driven by the outbreak of hostilities in the Middle East.

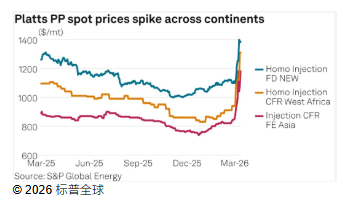

According to Platts, the price of polypropylene homopolymer injection molding grade in Europe has increased by 220 euros per ton since early March. On March 13, the ex-works spot price for northwest European homopolymer injection molding grade was 1,200 euros per ton.

In the African market, the Platts-assessed North Africa PP raffia grade cost and freight (CFR) spot price on March 11 was $1,290/mt, up $190/mt week on week, marking the largest weekly increase since the price assessment was launched on March 17, 2021. Additionally, Platts data shows that the CFR price for raffia grade in West Africa has risen by 39% since the outbreak of the conflict.

The Asian market posted the most significant gains. Platts assessed the Far East Asia PP injection-grade CFR spot price at $1,180 per metric ton, up $330 per metric ton from March 2.

The recent price increase is driven by multiple shocks triggered by the Middle East conflict, including suppliers in the region suspending quotations, leading to tighter supply, and rising costs of raw materials and energy, which have resulted in some producers in Asia and Europe suspending PP production.

Supply situation of PP and PE in the Middle East

According to S&P Global Commodity Insights’ CERA data, the Middle East accounts for nearly 25% of global polypropylene (PP) and polyethylene (PE) exports.

Previously reported by PRC, shipping in the Strait of Hormuz has been substantially interrupted, causing several major container shipping companies to suspend shipments from the Persian Gulf, leading to a significant reduction in exports from the region.

"Producers have refused to confirm the," said a European trader, reflecting the decrease in supplies from the Middle East to Europe.

Prices from various sources in the African and Turkish markets have declined, with sellers attributing the decrease mainly to fluctuations in upstream costs and continued rising freight rates. For a long time, Middle Eastern suppliers have dominated the African and Turkish markets, but in the face of rapid changes, most of their quotations were withdrawn within a few days of being issued.

Local distributors have expressed skepticism about the delivery timelines of Middle Eastern suppliers due to the halt in shipping through the Strait of Hormuz and regional port congestion. Some suppliers are attempting to transport goods from the east coast of Saudi Arabia to the west coast by land, but market participants note that such a logistics solution is technically challenging.

West African producers said that since March 2, with most quotes withdrawn or suspended, local trade activities have basically come to a standstill.

Turkish producers stated that, for urgent procurement needs, Russian and domestic Turkish sources have become alternative options, while Middle Eastern supplies face uncertain delivery timelines and Asian supplies are largely unavailable. According to industry sources, although overall consumption remains sluggish during Ramadan, some processing enterprises are urgently procuring raw materials to meet delivery commitments to European customers after Ramadan, driving a modest rebound in demand this week.

Producers lower operating rates

S&P Global Energy data shows that Asia's crude oil imports have decreased by 15.6 million barrels per day, causing a ripple effect on downstream production.

On the upstream side, the reduction in propane and naphtha feedstock supply has prompted producers to lower their operating rates, further exacerbating the supply tightness caused by a decline in import volumes.

On the Korean side, LG Chem has reduced the operating rates of all its naphtha crackers at the Yeosu and Daeesan sites to a minimum of 60%. In the downstream sector, producers such as Thailand's IRPC and Taiwan's Formosa Plastics have declared force majeure due to rising feedstock prices.

Multiple European producers have also suspended acceptance of new orders to ensure supply for contractual commitments, resulting in a severe shortage of PP spot supply. This week, LyondellBasell announced that its European polyolefins production operations have entered force majeure due to high energy and raw material costs.

As the conflict continues and maritime conditions in the Persian Gulf remain tense, market participants are preparing to cope with further tightening of supplies and persistently high raw material prices.

“The market has already realized that the longer the Middle East supply disruption lasts, the greater the eventual impact will be,” said a European producer.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

Tao Lin: Tesla’s Supercharger Stations in China Surpass 2,500

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Catl “wins big”: Beyond Batteries, What Else Can It Sell?