Medtronic acquires neurovascular company for $550 million

On March 10, 2026, global medical device giant Medtronic announced that it would acquire U.S. neurointerventional device company Scientia Vascular for $550 million (approximately RMB 3.9 billion), which includes potential milestone payments and an earn-out mechanism, with the transaction expected to close in the first half of fiscal year 2027. This is Medtronic's latest move following its February 2026 acquisition of cardiovascular diagnostic technology company CathWorks, marking that the global medical device industry's M&A wave is concentrating on the neurovascular field at an unprecedented speed.

I. Medtronic’s Strategic Gap-Filling: Enhancing Neurovascular “Access Capabilities”

Medtronic’s core rationale for this acquisition is “precise gap-filling.” As an early pioneer in the neurovascular interventional market, Medtronic boasts a robust portfolio of therapeutic devices—including liquid embolics, stent retrievers, and flow diverters—but has a notable gap in the “access” segment (i.e., precise delivery of guidewires and microcatheters to the lesion site). Scientia Vascular precisely fills this gap.

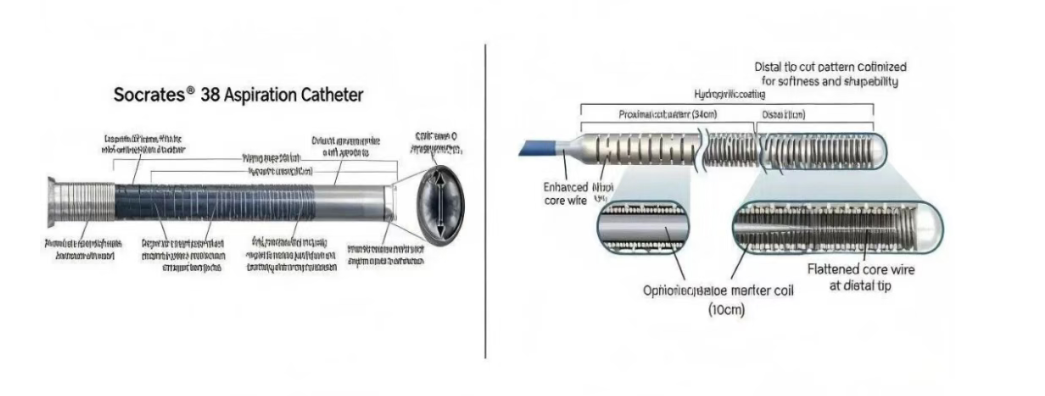

Scientia Vascular was founded in 2007 and is headquartered in Salt Lake City, Utah, USA. It currently has about 310 employees and focuses on developing neurointerventional devices for the treatment of complex cerebrovascular diseases. Its core products include the Aristotle guidewire, Plato 17 microcatheter, and Socrates 38 aspiration catheter, which utilize patented microfabrication technology to achieve faster and more reliable access in the complex and tortuous cerebral vascular anatomy.

According to third-party estimates, Scientia Vascular's revenue in 2025 is approximately $35 million, implying a price-to-sales (P/S) multiple of about 16.7x for this acquisition. Medtronic expects the transaction to be slightly dilutive to adjusted earnings per share in fiscal year 2027, but it will gradually become accretive following integration.

Linnea Burman, the head of Medtronic's Neurovascular business, clearly stated: "Scientia's guidewire and catheter products can seamlessly integrate with Medtronic's existing products, enabling Medtronic to support the entire surgical process for hemorrhagic and acute ischemic strokes." This means that Medtronic is building a complete surgical procedure solution from establishing vascular access to lesion treatment.

II. Giants Intensely Layout: The Neurovascular Track Enters an Integration Period

Medtronic's move is not an isolated incident. Over the past year, global medical device giants have carried out several high-profile acquisitions in the neurovascular field, forming a clear trend of industry consolidation.

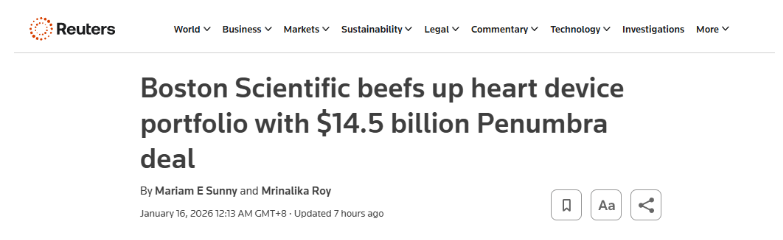

Boston Scientific: $14.5 Billion Acquisition of Penumbra

On January 15, 2026, Boston Scientific announced a $14.5 billion acquisition of Penumbra, a leading company in the neuro and peripheral intervention field, marking the first billion-dollar merger of 2026 and the second-largest acquisition in Boston Scientific's history. Penumbra mainly provides products in the neurovascular field, such as mechanical thrombectomy (thrombus aspiration systems), coils, and access catheters. Its revenue is expected to reach $1.4 billion in 2025, with a year-over-year growth of 17.3%-17.5%.

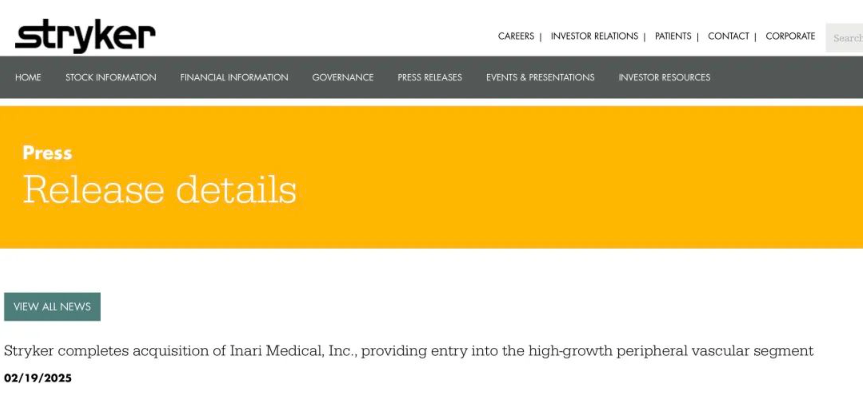

Stryker: Acquires Inari Medical for $4.9 Billion

In February 2025, Stryker completed the acquisition of Inari Medical for $4.9 billion, incorporating venous thrombectomy solutions into its neurovascular business portfolio. Inari Medical specializes in the treatment of venous thromboembolism (VTE), and its FlowTriever and ClotTriever systems have significant advantages in the fields of pulmonary embolism and peripheral vascular thrombectomy.

After the acquisition, Inari contributed $590 million in revenue to Stryker within 10 months, with a year-over-year growth of 52.3% in the second quarter of 2025, becoming Stryker's fastest-growing business segment.

III. Market-driven: Stroke Treatment Enters the Era of “End-to-End Competition”

The neurovascular sector has become a hotspot for M&A, driven by a vast market potential and clear clinical needs.

A large patient base and growth potential

Globally, approximately 12 million new stroke cases occur annually, making it one of the leading causes of death and long-term disability. With population aging and changing lifestyles, the overall burden of stroke continues to rise. Meanwhile, the widespread adoption of interventional techniques such as mechanical thrombectomy has made minimally invasive treatment a cornerstone in the management of acute stroke.

From the perspective of market size, the Chinese market for interventional medical devices for neurovascular diseases is growing rapidly. The market size in 2024 is 13.256 billion yuan, and it is expected to reach 19.722 billion yuan in 2025. By disease type, hemorrhagic stroke medical devices account for the largest share, with a size of 7.136 billion yuan in 2024, representing 53.83%; acute ischemic stroke medical devices are the fastest-growing sub-market, with an estimated compound annual growth rate of 33.0% from 2020 to 2026.

The global neurovascular interventional device market size is also considerable. According to Hengzhou Chengsi Research, the global neurovascular interventional device market size is approximately 10.87 billion yuan in 2024, and is expected to approach 14.02 billion yuan by 2031, with a compound annual growth rate of 3.7% over the next six years. Another report shows that the global neurovascular devices & interventional neurology devices market sales are expected to reach 32.81 billion yuan in 2031, with a compound annual growth rate of 5.0% (2025-2031).

From single equipment to full process solutions

In recent years, the industry logic of neurovascular therapies has been undergoing profound changes. In the past, many medical device companies held advantages only in specific segments of the stroke treatment pathway—for example, thrombectomy devices, aneurysm embolization materials, or imaging equipment. However, as technologies mature and the market expands, leading companies are increasingly inclined to build comprehensive product portfolios covering the entire treatment continuum.

A typical neurovascular interventional surgery generally includes several steps such as establishing vascular access, reaching the lesion site, and completing thrombectomy or embolization treatment. Each step corresponds to different types of devices. Those who can provide a more complete product system are more likely to form a stable usage ecosystem in clinical practice.

This shift from "single-device competition" to "competition based on end-to-end solutions" is precisely the core rationale driving major acquisitions. By acquiring companies to fill gaps in their product portfolios and building a complete closed-loop system—from access to treatment—has become the common strategic choice for industry leaders.

IV. Technology-Driven: Intelligence and Precision Have Become Competitive Focus Areas

M&A in the neurovascular field is not only for scale expansion but also for acquiring key technology platforms.

Intelligent algorithms become the core competitiveness

Penumbra’s most critical asset is not its thrombectomy catheter, but rather its globally unique CAVT (Computer-Assisted Vacuum Thrombectomy) intelligent algorithm. Traditional thrombectomy procedures heavily rely on the operator’s experience, whereas CAVT revolutionizes the process by real-time analysis of thrombus composition and optimization of aspiration pressure, transforming complex procedures into standardized, data-driven workflows. This represents not merely a technological upgrade, but a paradigm shift in surgical practice.

Boston Scientific's acquisition of Penumbra is essentially about buying the "operating system" for future endovascular procedures. Once CAVT technology is integrated into its coronary and peripheral product lines, Boston Scientific will establish a technological generational gap over its competitors across all vascular beds.

Materials and Structural Innovation

The core technological advantage of Scientia Vascular lies in its patented micro-machining technology. By removing material from nitinol hypotubes, it creates guide wires and catheters with micro-features (such as ring structures and interconnected beams). Compared to traditional braided and coil-reinforced devices, these have superior flexibility, support, and torque control capabilities.

The innovative potential of neurointerventional consumables in the future also includes directions such as material innovation, structural optimization, intelligence, and domestic substitution. Biodegradable materials, as well as more elastic and durable materials, may become better choices for interventional procedures; the shape and structure of consumables can be optimized according to the type of pathology and anatomical characteristics to meet different treatment needs; integrating sensors and navigation technologies enables neurointerventional devices to have real-time feedback and higher precision.

V. Reshaping of the Competitive Landscape: From a Tripartite Standoff to Super Giants

M&A waves are completely reshaping the competitive landscape of the neurovascular market.

Market share reshuffle

Prior to the acquisition, the neurointerventional market was dominated by Medtronic (26%), Stryker (19%), Johnson & Johnson (15%), Penumbra (13%), and MicroVention (5%). Following the transaction, the combined Boston Scientific + Penumbra entity captured a 28% market share, ascending to the top position and directly challenging Medtronic’s leadership.

Medtronic needs to accelerate the iteration of its pipeline flow-diverting devices, and may increase investment in R&D or acquisitions in intelligent technologies to cope with competitive pressures. Stryker will strengthen the clinical promotion of products such as Surpass Evolve, while seeking breakthroughs in the field of intelligent assistance. Johnson & Johnson may accelerate external acquisitions in its Cerenovus business to compensate for technical shortcomings.

Dual pressure in the Chinese market

The Chinese neurointerventional market is projected to reach RMB 17.5 billion by 2026, with a compound annual growth rate (CAGR) exceeding 20%. However, the domestic localization rate has increased from 12.3% in 2020 to 38.7% in 2024. Domestic enterprises—including MicroPort NeuroTech, PEGASUS Medical, and Sinovasc—have rapidly penetrated grassroots markets by leveraging cost-effective solutions.

However, the entry of Boston Scientific and Penumbra will create a dual squeeze: In top-tier hospitals, physicians will increasingly favor the standardized surgical protocols enabled by CAVT’s intelligent algorithms—a technological barrier that domestic companies will struggle to replicate in the short term, thereby reinforcing the technology moat; in the grassroots market, Boston Scientific may adopt a “equipment placement + consumables bundling” strategy to rebuild its brand moat in county-level hospitals, further squeezing the survival space of domestic companies.

VI. Future Outlook: Industrial Evolution in the Era of Intelligent Transformation

Technology Evolution Directions (2026-2030)

Investment Strategy Iteration

Short-term (1-2 years) focus on integration progress and competitor reactions. Opportunities lie with third-party software companies providing intelligent solutions to industry giants. Mid-term (3-5 years) in the Chinese market, look for companies with global intellectual property and substantive breakthroughs in AI algorithms or biodegradable materials. Simultaneously, pay attention to local leaders that can penetrate county-level healthcare through unique business models.

A global merger and acquisition boom in the medical device industry is increasingly concentrating on the neurovascular sector—not only reflecting capital’s preference but also representing an inevitable trend in industrial development. The enormous clinical demand for stroke treatment, rapid advancements in neurointerventional technologies, and the competitive paradigm shift from single-device offerings to comprehensive, end-to-end solutions collectively drive this trend.

Medtronic's acquisition of Scientia Vascular, Boston Scientific's acquisition of Penumbra, and Stryker's acquisition of Inari Medical have not only altered the strategic layouts of these companies but also reshaped the competitive landscape of the entire industry. As intelligence and platformization become new focal points of competition, the neurovascular field is shifting from "device-driven" to "intelligence-driven." Future competition will not only be about product comparisons but also the contest of ecosystems and technology standards.

For indigenous Chinese enterprises, this presents both challenges and opportunities. Against the backdrop of accelerating consolidation by industry giants, the previous strategy of domestic substitution based solely on cost-effectiveness is no longer sustainable. Instead, enterprises must shift toward technological innovation and internationalization, seeking breakthroughs in next-generation technologies such as AI algorithms and biodegradable materials to secure a competitive position in the future.

The merger and acquisition wave in the neurovascular sector continues, and this battle for the “brain” has only just begun.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Middle East Tensions Escalate Sharply: How Polyolefins Respond Amid Soaring Risk Premium

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

LG Chem Declares Force Majeure on DOTP Exports! SABIC Joins Five Giants to Redefine EV Safety