Li bin and lei jun "sound the alarm," another chip crisis is looming

With the rapid development of artificial intelligence technology, the global demand for high-performance memory chips in data centers is exploding. Now, this trend is triggering a supply chain crisis affecting the automotive industry.

Recently, multiple analysis institutions, including Wells Fargo, UBS, and S&P Global, have issued warnings, pointing out that due to the continued tight supply of DRAM (Dynamic Random Access Memory) chips, automakers may face severe cost pressures and production disruption risks as early as 2026.

The root of this crisis lies in the fact that chip manufacturers are prioritizing production capacity for the more profitable and faster-growing data center and AI markets, while the automotive industry, with less than 10% share of the global DRAM market, has weak bargaining power.

DRAM prices have seen astonishing increases. A Wells Fargo report indicates that DDR5 spot prices are more than 8 times higher than their 2024 average, and DDR4 prices are more than 16 times higher.

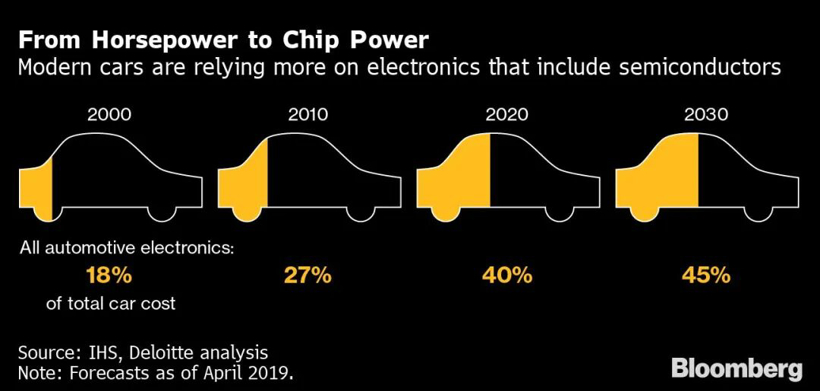

While the current DRAM cost per vehicle is only about $50 to $110, the dual pressure of rising prices and supply shortages could significantly squeeze automakers' profit margins, especially impacting electric vehicles and high-end models that rely heavily on chips.

Analysts predict that global DRAM demand will grow by approximately 26% in 2026, while supply will only increase by about 21%, implying a supply shortfall of roughly 14%. Concurrently, major chip suppliers, including Micron, Samsung, and SK Hynix, are accelerating the shift of their production capacity towards high-end products like High Bandwidth Memory (HBM), further reducing chip sources for the automotive industry.

While this crisis shares similarities with the 2021 chip shortage, its drivers are more concentrated, as the expansion of AI infrastructure reshapes the global semiconductor supply chain landscape. Automakers must not only contend with surging prices but also face potential production line shutdowns due to chip supply disruptions.

AI demand squeezing the automotive industry

Actually, as early as last December, Meng Qingpeng, Vice President of Supply Chain at Li Auto, frankly stated: "In 2026, the automotive industry will face an unprecedented storage chip supply crisis, with a fulfillment rate of potentially less than 50%." Subsequently, in early January of this year, NIO founder Li Bin stated that the current rise in memory prices is putting enormous pressure on the automotive industry.

During a livestream in January, Xiaomi Auto Chairman Lei Jun also mentioned the price of the new Xiaomi SU7, stating, "Memory prices are increasing quarterly, rising 40% to 50% last quarter. It's said that they will continue to rise in the first quarter. According to this trend, the memory alone for a car will increase by several thousand yuan this year."

Actually, the core conflict of the current DRAM supply chain tension stems from the explosive growth in demand for AI data centers and the steady rise in chip demand from the automotive industry competing for resources.

With the increasing popularity of generative AI applications like ChatGPT, tech giants such as Google, Meta, and Amazon are experiencing a surge in demand for High Bandwidth Memory (HBM) and high-end DRAM, which offer significantly higher profit margins compared to traditional DRAM products used in the automotive industry.

Samsung, SK Hynix, and Micron, the three major giants, are therefore significantly shifting their capital expenditures and production capacity towards data centers, and even gradually phasing out older process chips such as DDR4, which are still widely used by automakers. S&P Global points out that this shift in capacity is not a temporary adjustment but a structural change, as the profitability and growth prospects of AI data centers far exceed the automotive market.

The automotive industry is at a double disadvantage in this round of competition. Firstly, its market share is small, accounting for less than 10% of global DRAM demand, making it difficult to compete with tech companies that order hundreds of thousands of wafers at a time in procurement negotiations. Secondly, it lags behind in technology; due to long certification cycles and high reliability requirements, automobiles often use chip manufacturing processes that are one to two generations behind consumer electronics.

Nowadays, as chipmakers accelerate the phasing out of older production lines in pursuit of higher profits, automakers are forced into a situation where the supply of older chips is dwindling and the capacity for new chips is insufficient.

Wells Fargo estimates that the top ten automotive Tier 1 suppliers will consume approximately 54% of global automotive DRAM by 2025, with BYD, Tesla, and Aptiv leading the way, indicating that supply chain risks are more concentrated among leading companies.

Furthermore, data on the supply gap further confirms the urgency of the crisis. Wells Fargo forecasts DRAM demand growth of 26% in 2026, while supply will only increase by 21%. UBS points out that the price increase of some automotive chips has already exceeded 100%.

More critically, capacity expansion takes time. IBK Securities suggests that new factories of Samsung and SK Hynix will not reach mass production until 2028, making it difficult to alleviate the supply shortage before then. Furthermore, the shortage of memory chips is spreading from consumer electronics to the automotive sector, as all industries share the same silicon wafer-based production capacity.

S&P Global warns that the window of time for automakers to redesign systems and secure supplies is narrowing; failure to adjust in time could lead to production disruptions between 2026 and 2028.

This shortage also has key differences from the 2021 chip crisis, which was triggered by a combination of factors including supply chain disruptions due to the pandemic, pull-forward demand for consumer electronics, and a rebound in automotive demand. This current crisis, however, is more focused on memory chips, and its driving factor is singular and clear: the artificial intelligence investment boom.

This means the solution is no longer just waiting for production capacity to recover, but requires the automotive industry to re-evaluate its chip strategy, including technological upgrades, supply chain reshaping, and even in-depth collaboration with chip manufacturers.

02How should car companies respond?

It is not difficult to see that this round of memory chip shortages will have diverse impacts on the automotive industry. The most immediate impact is cost pressure. Although the current DRAM cost per car is less than $200, S&P Global expects that new contract prices may increase by 70% to 100% year-on-year by 2026. High-end models, due to more autonomous driving and entertainment systems, may have a single-vehicle chip cost as high as $2,000.

It is difficult for consumers to absorb all of these additional costs, especially given the fierce price competition in the electric vehicle market, and manufacturers' profits will be significantly squeezed. Wells Fargo points out that signs of panic buying have emerged, which could drive up prices and disrupt production schedules, creating a vicious cycle.

UBS warns that production disruption risks, with shortages potentially disrupting global auto production as early as the second quarter of this year. The most affected will be electric vehicle manufacturers that are heavily reliant on advanced chips, such as Tesla, Rivian, and BYD, as these companies' models are more digitized and have greater memory requirements. Traditional automakers such as Ford and GM will be less affected, but high-end models will also face challenges.

First-tier suppliers upstream in the supply chain are also finding it difficult to remain unaffected. Companies like Visteon and Aptiv, which primarily provide high-tech cockpits and advanced driver-assistance systems, will face delays in order delivery directly due to the chip shortage. If the chip supply remains tight, the possibility of some vehicle models being discontinued between 2026 and 2027 is not an exaggeration.

To cope with the crisis, the automotive industry can seek solutions from both short-term relief and long-term transformation. Short-term strategies include securing supply, adjusting configurations, and passing on costs. It is understood that some automakers have attempted to sign long-term agreements with chip manufacturers, but with limited success, as production priority still favors data centers. Dealerships may alleviate pressure by simplifying configurations and extending delivery times.

In the long run, the automotive industry must accelerate technological iteration and supply chain autonomy. For example, Tesla has independently developed AI chips and maintains close cooperation with Nvidia; BYD has also invested in chip production, although its current products are relatively basic. More automakers may be forced to redesign their electronic architectures to reduce reliance on single chips, or shift to more advanced processes such as DDR5, but this requires time and significant investment.

It can be said that this crisis has revealed the deep-seated vulnerabilities of the automotive supply chain. With the advent of the software-defined vehicle era, chips have transformed from ordinary components into strategic resources. In the future, automakers may need to be more deeply involved in chip design, invest in chip production capacity, or establish equity-based partnerships with suppliers.

S&P Global suggests the automotive industry establish a more flexible supply system while promoting chip standardization to reduce reliance on specific models. For consumers, this may lead to fewer options, longer wait times, and potentially higher prices when purchasing vehicles in the coming years, especially for high-end technology-equipped models.

In short, the memory chip shortage triggered by artificial intelligence is pushing the automotive industry into a new supply chain storm. This crisis is not only about cost and production, but also forces the industry to rethink its position in the global semiconductor ecosystem.

Companies that can quickly adapt and proactively deploy chip strategies will likely gain a greater competitive advantage after the crisis, while those who react slowly may face the risk of being eliminated. In this era where chips are the core competitiveness, the transformation of the automotive industry is destined to be full of challenges.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Key Players: The 10 Most Critical Publicly Listed Companies in Solid-State Battery Raw Materials

-

Vioneo Abandons €1.5 Billion Antwerp Project, First Commercial Green Polyolefin Plant Relocates to China

-

EU Changes ELV Regulation Again: Recycled Plastic Content Dispute and Exclusion of Bio-Based Plastics

-

Clariant's CATOFIN™ Catalyst and CLARITY™ Platform Drive Dual-Engine Performance

-

New 3D Printing Extrusion System Arrives, May Replace Traditional Extruders, Already Producing Car Bumpers