Jushi Chemistry Reports Loss of 119 Million Yuan

Recently, Jushi Chemical, a leader in the flame-retardant modified plastics segment, released its 2025 annual earnings preview. On one hand, it reported a significant 49.78% year-over-year reduction in losses, signaling marginal improvement in its core business; on the other hand, it still posted a full-year loss of RMB 119 million, with issues such as shrinking net assets and drag from a single business segment remaining unresolved. As a company listed on the STAR Market, Jushi Chemical continues to face an arduous path toward profitability.

Core Data Breakdown: Significant Loss Reduction, but Underlying Concerns Remain

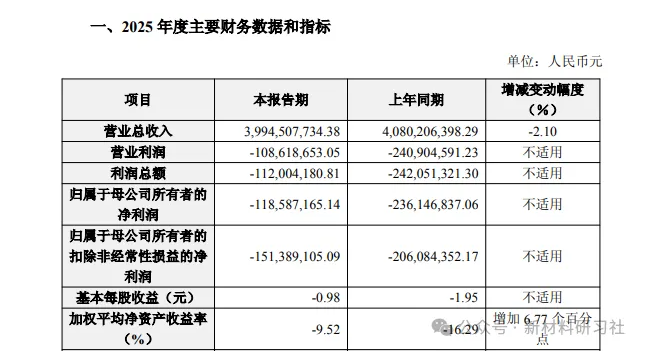

Revenue slightly declined, scale stabilizedIn 2025, the company achieved total operating revenue of RMB 3.995 billion, a slight decrease of 2.10% compared to RMB 4.080 billion in the same period of the previous year, maintaining overall revenue stability without significant fluctuations.

Significant reduction in losses, but profitability remains weakNet loss attributable to shareholders was RMB 118.6 million, an improvement of RMB 117.6 million compared to the net loss of RMB 236 million in the same period last year, representing a nearly 50% reduction in losses. However, the non-GAAP net loss attributable to shareholders was RMB 151 million, which is over RMB 30 million worse than the reported net loss, indicating that the core business remains fundamentally weak in profitability.

Net assets shrink, shareholders' equity under pressureAt the end of the reporting period, the equity attributable to the parent company amounted to RMB 1.183 billion, a decrease of 9.29% from the beginning of the period; the net asset value per share declined from RMB 10.75 to RMB 9.75, a drop of 9.30%, with continuous losses directly eroding the company’s net assets.

The indicator has improved but remains negative.Basic earnings per share improved from RMB -1.95 to RMB -0.98, and the weighted average return on net assets increased from -16.29% to -9.52%. Although there is a notable improvement, both metrics remain deeply negative, indicating that profitability has not yet achieved a substantive breakthrough.

In short, Ju Shi Chemical's performance in 2025 was characterized by "stabilization after decline" but not yet "returning to profitability." The reduced losses stemmed from the company's proactive optimization efforts rather than explosive growth in its core business.

"Burden Shedding" + Dual-Wheel Drive of Main Business Improvement

As a leader in the flame-retardant modified plastics sector, Polyrock Chemicals' ability to achieve nearly a 50% reduction in losses is not by chance, but primarily due to three key measures:

1. Divest loss-making subsidiaries

In 2025, the company's biggest move was to divest the continuously loss-making subsidiary, CrownZhen Technology — this subsidiary, which was acquired in 2021, not only incurred losses year after year but also orchestrated fake transactions in the first half of 2023, leading to an inflated revenue of 157 million yuan for Jushi Chemical, making it a veritable "anchor" on performance.

Ultimately, Jushi Chemistry sold it for a consideration of 50,000 yuan, and required the original shareholders to pay a performance compensation of 60 million yuan. At the same time, it merged or liquidated other poorly performing subsidiaries, thereby cutting off the sources of losses and reducing operating costs.

Core business recovery, marginal improvement is obvious.

The company’s core business—modified plastics—achieved modest growth in both annual revenue and gross profit, with outstanding performance across its three key sub-segments.

Optical display materials: Profitability improved due to lower raw material prices, coupled with increased production capacity and yield.

Private-label hygiene products: Performing well in the Nigerian market, with declining raw material prices and shipping costs, coupled with stable local currency exchange rates, resulting in steady improvement in business profitability.

Hubei EPP Foaming Project: After capacity ramp-up, unit fixed costs are reduced through cost allocation, and process optimization further lowers costs, gradually unlocking benefits.

3. The low base effect of the previous year helped reduce the loss.

In 2024, the company prudently recorded substantial impairment provisions for fixed assets, intangible assets, goodwill, and other assets, which positively contributed to reducing losses in 2025 and resulted in a more pronounced year-over-year improvement.

The core problem of not turning losses into profits: three restrictive factors blocking the way

Despite significant progress in reducing losses, Jushi Chemical has not yet escaped the loss-making situation, primarily constrained by three unfavorable factors, which have become the "stumbling blocks" for profit recovery.

1. Liquefied Petroleum Gas (LPG) business: the largest drag on performance

This business originated from the company's investment in the bankruptcy reorganization of Anhui Haide Chemical in 2023. In 2025, due to fluctuations in international oil prices, there was a short-term imbalance in the supply and demand of raw materials and a sharp fluctuation in prices, which not only disrupted production schedules but also further narrowed the gross profit margin. Ultimately, this led to a significant decline in revenue and an exacerbation of losses, becoming the key reason why the company failed to turn a profit.

2. New capacity ramp-up: Cost pressures remain high

In June 2025, the halogen-free flame retardant expansion project of subsidiary Chizhou Jushi commenced trial production. However, during the capacity ramp-up phase, unit fixed costs remained high, while depreciation, administrative expenses, and financial expenses all increased simultaneously. The new project’s benefits have yet to materialize, and instead, it has temporarily diluted the company’s overall profitability.

More notably, the project, originally scheduled to reach its intended operational status by October 2025, has been postponed to June 2026, implying that the profit contribution from the new capacity will have to wait for a while longer.

Fiscal fraud penalty, years of performance pressure

Notably, shortly before the release of its performance, Jushi Chemical was penalized for financial fraud. In early February 2026, the Guangdong Securities Regulatory Bureau issued an “Administrative Penalty Decision,” finding that the company and its subsidiary engaged in sham trading activities lacking commercial substance during the first half of 2023, thereby fraudulently inflating operating revenue by RMB 157 million. The company and relevant responsible individuals were collectively fined RMB 6.7 million.

Historically, Jushi Chemical has faced prolonged pressure: in 2023, its attributable net profit was RMB 0.29 billion (with a non-GAAP net loss of RMB 0.25 billion); in 2024, it reported an attributable net loss of RMB 2.36 billion; and although it is expected to significantly narrow losses in 2025, this will mark its second consecutive year of net losses, with non-GAAP net losses projected for three consecutive years.

As a company listed on the STAR Market in 2021, Jushi Chemistry's issue price was 36.65 yuan per share. As of the close on March 5th, the stock price was 28.45 yuan, with a total market value of 3.45 billion yuan, and the stock price has experienced some short-term fluctuations.

The company also admitted in the announcement that although the loss narrowed year-on-year, it is still in a state of overall loss. For this leading company in the flame-retardant modified plastics sector, the key to profit recovery in 2026 depends on three points:

Can the liquefied petroleum gas business stabilize and get rid of the drag of losses?

Whether the Chizhou Jushi halogen-free flame retardant capacity expansion project can be completed and reach full production as scheduled, unlocking a new profit growth driver.

Whether cost control can continue to deliver results and whether the profitability of core operations can be further enhanced.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Middle East Tensions Escalate Sharply: How Polyolefins Respond Amid Soaring Risk Premium

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

LG Chem Declares Force Majeure on DOTP Exports! SABIC Joins Five Giants to Redefine EV Safety