Haitian, Yizumi, Tri-Ring... 10 Listed Plastic Machinery Companies Release Half-Year Reports! Overseas Markets Become Performance Growth Champions

Recently, Chinese listed plastic machinery companies have successively released their “report cards” for the first half of 2025, showing a marked trend of “the strong stay strong while polarization intensifies.” Leading companies have achieved double growth in revenue by leveraging technological advantages and global, while some companies are facing dual pressures from intensified market competition and business restructuring.

Next, let's follow the editor to take a look.Haitian International, Yizumi, Tederic Machinery, Topstar, Jinming MachineryLet’s look at the performance of leading plastic machinery companies and industry trends!

A summary of the semi-annual financial reports of the top ten listed plastic machinery companies.

Haitian International: Profit and Revenue Both Increase in the First Half of the Year, Overseas Markets Become an Important Growth Engine

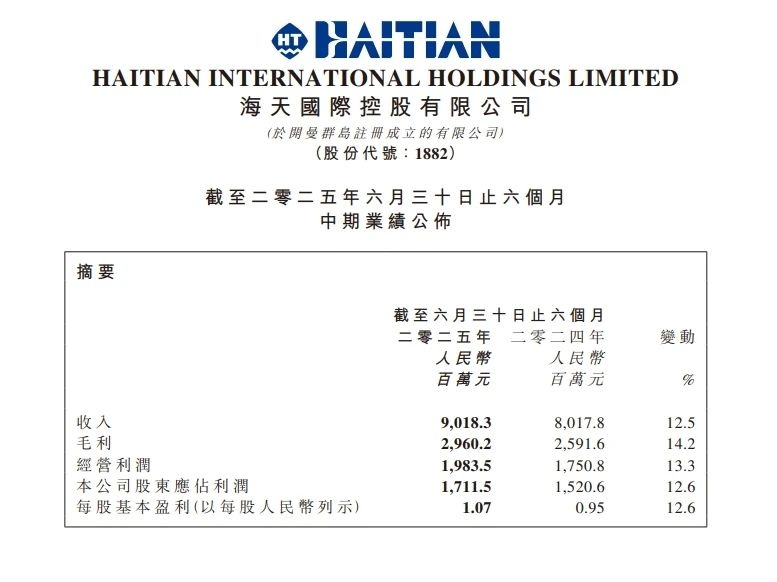

Haitian International's performance for the first half of 2025 shows that during the reporting period, the company achieved revenue of 9.018 billion yuan, representing a year-on-year increase of 12.5%; gross profit reached 2.96 billion yuan, up 14.2% year-on-year; profit attributable to shareholders was 1.712 billion yuan, an increase of 12.6% year-on-year; basic earnings per share were 1.07 yuan, up 12.6% year-on-year. Overall, the company continued to demonstrate steady growth in its operating performance.

During the reporting period, the overseas market became the most prominent growth highlight. Leveraging years of strategic deployment and accumulation, the company’s localized supply chain and delivery capabilities in regions such as Southeast Asia have been continuously strengthened, enabling it to precisely capture the demand growth brought about by industry chain adjustments. In the first half of the year, overseas sales reached 3.818 billion yuan, representing a significant year-on-year increase of 34.7%, and the proportion of total revenue rose to 42.3%, making it the core driver of growth. The domestic market demonstrated strong resilience, achieving stable business development on a high base by deeply cultivating niche sectors and expanding key customers, with sales revenue reaching 5.201 billion yuan, a year-on-year increase of 0.3%.

From the perspective of industry drivers, the accelerated development of downstream industries, represented by new energy vehicles, has led to a continuous release of demand for injection molding machines, with all series of products maintaining a growth trend. Among them, benefiting from the growth in demand for daily consumer goods overseas, as well as the domestic new energy vehicle and home appliance industries, the Mars and Jupiter series achieved rapid growth. In the first half of the year, sales revenue from injection molding machines reached 8.637 billion yuan, a year-on-year increase of 12.1%; sales revenue from components and services reached 381 million yuan, a year-on-year increase of 21.0%.

Yizumi: Both revenue and net profit grow, with sales of all three major businesses increasing by over 10% year-on-year.

Recently, Yizumi released its semi-annual report for 2025. During the reporting period, the company achieved total operating revenue of 2.746 billion yuan, representing a year-on-year increase of 15.89%. The net profit attributable to shareholders of the listed company was 345 million yuan, a year-on-year increase of 15.15%. In addition, R&D investment amounted to 133 million yuan, up 8% year-on-year.

According to the announcement, the performance growth in the first half of the year was mainly attributed to the improvement in industry prosperity and the accelerated implementation of the globalization strategy. The company continuously enhanced operational efficiency by increasing R&D investment and product innovation, optimizing supply chain management, and effectively reducing production and operating costs. For example, through technological innovation to consolidate core businesses and diversified synergy driving, the sales of the company's three main businesses all achieved growth in the first half of the year. Among them, the injection molding machine business achieved sales revenue of 1.932 billion yuan, a year-on-year increase of 13.09%; the die casting machine business achieved sales revenue of 556 million yuan, a year-on-year increase of 33.29%; and the rubber machine business achieved sales revenue of 119 million yuan, a year-on-year increase of 23.85%.

Among them,The injection molding machine business is the company's core business, contributing more than 70% of the revenue.The growth was mainly driven by improved operational efficiency and increased sales efforts. The die-casting machine business showed remarkable growth, with a year-on-year increase of over 30%. The growth in the rubber machine business was attributable to strong order fulfillment and the rapid expansion of overseas operations.

It is worth mentioning that in the first half of 2025,Yizumi's overseas revenue reached 749 million yuan, a year-on-year increase of 27%, accounting for 27.28% of total revenue.From the data, it can be seen that the globalization strategy that the company has been promoting in recent years has begun to show results. It is reported that Yizumi has now established subsidiaries in 12 countries and regions, with over 86 service outlets across overseas regions. By 2024, the company's overseas market revenue has reached 1.395 billion yuan, accounting for 27.54% of the total revenue, with a year-on-year growth of 27.45%.

Sinochem Equipment: Net loss of 18.37 million yuan in the first half of the year! Major asset restructuring launched after significant loss reduction

On August 25, Sinochem Equipment released its 2025 semi-annual report. The report shows that the company’s operating revenue for the first half of the year was 658 million yuan, a year-on-year decrease of 85.39%; net profit attributable to shareholders was -18.3759 million yuan, a year-on-year increase of 93.60%; net profit attributable to shareholders excluding non-recurring gains and losses was -26.8148 million yuan, a year-on-year increase of 94.77%; basic earnings per share were -0.04 yuan.

The company's main business involves the research and development, production, and sales of rubber and plastic machinery as well as chemical equipment, and provides systematic services and solutions for rubber and plastic equipment and other chemical equipment. The composition of main business revenue is as follows: injection molding equipment 36.78%, extrusion equipment 30.71%, reaction molding equipment 13.34%, drying equipment 8.42%, others 4.74%, vulcanizing equipment 3.36%, engineering, supervision, and technical services 2.66%.

Previously, Sinochem Equipment disclosed plans to issue shares to acquire 100% equity of Yiyang Rubber & Plastic Machinery Group Co., Ltd. ("Yiyang Xiangji") held by China Chemical Equipment Co., Ltd., and 100% equity of Bluestar (Beijing) Chemical Machinery Co., Ltd. ("Beihua Ji") held by Beijing Bluestar Energy-saving Investment Management Co., Ltd., while simultaneously raising supporting funds. This transaction is expected to constitute a major asset restructuring. Sinochem Equipment stated that the company will further integrate the internal equipment sector assets of China Sinochem to enhance the securitization rate of state-owned assets. The company hopes to take this opportunity to achieve turnaround and profitability as soon as possible.

Terry Machinery: Net profit of 56.397 million yuan in the first half of the year, a year-on-year increase of 27.09%

On August 29, Terry Machinery released its semi-annual report, posting operating revenue of 584 million yuan, up 1.16% year-on-year. Net profit attributable to shareholders of the listed company was 56.397 million yuan, an increase of 27.09% year-on-year. Net profit attributable to shareholders of the listed company after deducting non-recurring gains and losses was 53.186 million yuan, up 31.93% year-on-year.

Jinying Co., Ltd.: Net Profit Turns to Loss! Achieved Total Operating Revenue of 586 Million Yuan in the First Half of 2025

On August 27, Golden Eagle Co., Ltd. disclosed its semi-annual report for 2025. In the first half of 2025, the company achieved a total operating revenue of 586 million yuan, a year-on-year decrease of 12.11%; net profit attributable to shareholders was a loss of 8.7692 million yuan, compared with a profit of 36.8263 million yuan in the same period last year; net profit after deducting non-recurring gains and losses was a loss of 9.2931 million yuan, compared with a profit of 32.9181 million yuan in the same period last year; net cash flow generated from operating activities was 102 million yuan, compared with -186 million yuan in the same period last year. During the reporting period, the basic earnings per share of Golden Eagle Co., Ltd. was -0.024 yuan, and the weighted average return on net assets was -0.928%.

According to available information, Zhejiang Jinying Co., Ltd. is mainly engaged in the manufacturing and sales of complete sets of flax, wool, silk, and spun silk textile machinery and equipment. Its business also covers linen spinning, silk spinning, weaving, dyeing and finishing, and garment manufacturing, as well as injection molding machinery series equipment and the research, development, manufacturing, and sales of lithium battery cathode materials. The composition of its main business income is as follows: textiles 55.03%, injection molding machines and accessories 27.94%, textile machinery and accessories 10.51%, others (supplementary) 2.48%, garments 2.12%, new energy battery materials 1.66%, and other 0.26%.

Datron Machinery: Achieved a net profit of HKD 4.07 million for the interim period.

On August 27, Datong Machinery announced that for the six months ending June 30, 2025, revenue from continuing operations amounted to HKD 996 million, an increase of 11.6% year-on-year; gross profit was HKD 186 million, an increase of 21.1% year-on-year; profit for the period was HKD 4.07 million, compared to a loss of HKD 3.071 million for the same period last year.

In the mechanical manufacturing business, Datong Machinery stated that factors such as US tariffs, domestic overcapacity, and the sluggish recovery of the real estate market have increased the pressure on its injection molding machine manufacturing business to balance order volume and profitability. As a result, sales revenue from this business in the first half of the year decreased compared to the same period last year. In addition, there was a significant decline in export business.

Huayan Precision Machinery: Revenue increased by 24.8% in the first half of the year, with overseas income surging by 143%

Huayan Precision Machinery is one of the earliest domestic enterprises to enter the PET preform injection molding equipment sector. According to its 2025 semi-annual report, the company achieved operating revenue of 290 million yuan, a year-on-year increase of 24.8%; net profit attributable to shareholders was 36.52 million yuan, up 9% year-on-year; and net profit attributable to shareholders excluding non-recurring gains and losses was 32.87 million yuan, an increase of 11.2% year-on-year. In the second quarter, the company achieved operating revenue of 160 million yuan, a year-on-year increase of 37.5%; and net profit attributable to shareholders was 22.44 million yuan, up 13.8% year-on-year.

The company stated that the performance growth is attributed to its proactive expansion into overseas markets, resulting in a rapid increase in product export volume; the company’s active investment in research and development and the launch of new products have enhanced its industry competitiveness; the favorable industry conditions have driven an increase in product demand; the company’s fundraising project (the intelligent bottle preform molding system expansion and construction project) was completed and put into operation on January 31, 2025, thereby enhancing the company’s delivery capacity.Overseas sales revenue reached 110 million yuan, representing a year-on-year increase of 142.99%, accounting for 38.17% of the company's total revenue.

Huayan Precision Machinery's main products include preform intelligent molding systems, preform molds, and related supporting products. The independently developed Epioneer series of high-end preform intelligent molding systems can be equipped with cavity preform molds for production, characterized by multiple cavities, high speed, high efficiency, and energy saving, representing a high level of preform molding technology in China. Currently, the company's customers span various sub-sectors such as drinking water, beverages, edible oil, and daily chemical products, having accumulated extensive customer resources both domestically and internationally, with high market recognition. In the international market, the company's products have achieved significant success in the Southeast Asian market and have entered the preform molding equipment markets in countries or regions such as Africa, the Middle East, New Zealand, Turkey, and Australia.

Topstar: Revenue Down 37%, Gross Profit of Injection Molding Equipment Business Increases

According to Topstar's financial report for the first half of 2025, the company achieved a revenue of 1.086 billion yuan, a decrease of 36.98% compared to 1.723 billion yuan in the same period last year. The significant decline was primarily due to a 67.20% contraction in the scale of the intelligent energy and environmental management system business. The company is advancing its strategic transformation of "focusing on products and reducing projects," proactively adjusting this business to optimize its structure. Although the scale of product-related business has steadily increased, with revenue growing by 22.66% year-on-year, it could not offset the impact of the decline in the intelligent energy and environmental management system business.

By business segment, the industrial robot segment grew by 22.55%, with self-produced multi-joint industrial robots increasing by 80.86%, demonstrating the effectiveness of product competitiveness and market strategies. The injection molding machine segment saw a decrease in revenue from traditional hydraulic injection molding machines due to product line structure optimization. However, supporting equipment and automatic feeding systems grew by 29.64%, resulting in an overall segment revenue decrease of 0.87% year-on-year. Nevertheless, with the optimization of the traditional hydraulic injection molding machine product structure, the segment’s gross profit margin improved, increasing by 6.46 percentage points year-on-year. The supporting equipment and automatic feeding system business for injection molding machines achieved operating revenue of RMB 149.3034 million, a year-on-year increase of 29.64%, with gross profit margin up by 3.58 percentage points year-on-year. The main reason for the revenue growth is the company’s outstanding market position for related products. On the basis of optimized sales strategies and improved product quality, coupled with significant results from overseas market expansion, related orders grew rapidly.

Daliylong: Net profit for the first half of the year was 90.8675 million yuan, a year-on-year increase of 217.89%.

In the semi-annual report for 2025, Dali Long demonstrated that the company achieved an operating income of 957 million yuan in the first half of the year, marking a year-on-year growth of 57.35%. The net profit attributable to shareholders reached 90.8675 million yuan, reflecting a year-on-year increase of 217.89%. The basic earnings per share were 0.4557 yuan. During the reporting period, the company continued to focus on research and innovation in core key components around blow molding technology, heating technology, aseptic sterilization processes and equipment, filling technology, end-stage packaging, and automation control technology. Efforts were also made towards standardization and modularization, optimizing, improving, and innovating the entire product series.

Jinming Precision Machinery: Half-year performance rebounds, net profit attributable to parent company increases by 12.11% year-on-year.

Jinming Precision Machinery focuses on two core businesses: high-end plastic machinery manufacturing and high-performance films. According to its 2025 semi-annual report, during the reporting period, the company achieved operating revenue of 226 million yuan, compared with 232 million yuan in the same period last year, remaining basically flat year-on-year; net profit attributable to the parent company’s owners reached 7.2549 million yuan, representing a year-on-year increase of 12.11%.

As a professional film production equipment manufacturer and solution provider integrating R&D, design, production, sales, and service, the company offers customized high-end intelligent equipment and actively promotes the application of industrial big data in intelligent manufacturing. Its film products (biaxially oriented films and high-barrier functional flexible packaging films) possess excellent performance and are widely used in various fields such as new energy, displays, home appliances, building materials, pharmaceutical packaging, and automobiles. Among them, high-barrier films are operated by the subsidiary Jinjia New Materials.

Industry Trend: Globalization Layout Dual-motor drive

Analyzing the financial reports of the above plastic machinery companies comprehensively, four major trends can be clearly seen:

Industry concentration continues to increase, with a clear trend of differentiation.On one hand, leading companies in the plastic machinery industry are continuously expanding their market share by leveraging their scale advantages, technological accumulation, and global layout capabilities. On the other hand, some plastic machinery companies faced operational difficulties in the first half of the year and need to achieve breakthroughs through asset restructuring and strategic transformation. In the first half of the year, Sinochem Equipment's operating income dropped significantly by 85.39% year-on-year, with a net profit loss attributable to the parent company amounting to 18.3759 million yuan. Jinying Holdings achieved a total operating income of 586 million yuan in the first half, with a net profit loss attributable to the parent company of 8.7692 million yuan. Although Datong Machinery's overall revenue increased by 11.6%, the sales of its injection molding machine manufacturing business decreased compared to the same period last year.

The overseas market has become the core engine of growth.The overseas market has become the most important growth engine for leading plastic machinery companies. Among them, Haitian International’s overseas sales surged by 34.7% year-on-year, with the proportion of total revenue rising to 42.3%. Yizumi’s overseas revenue reached 749 million yuan, a year-on-year increase of 27%, accounting for 27.28% of total revenue. Huayan Precision Machinery achieved overseas sales revenue of 110 million yuan, a year-on-year increase of 142.99%, accounting for 38.17% of the company’s total revenue.

Technological innovation creates differentiated competitive advantages.Plastic machine companies taking the specialization route have also demonstrated strong resilience. For example, Dalian YiLong's continuous R&D investment in areas such as bottle blowing technology and aseptic sterilization processes and equipment has paid off in the market, achieving a 217.89% year-on-year increase in net profit. Tederic Machinery saw a 27.09% increase in net profit despite a slight 1.16% increase in revenue. Huayan Precision Machinery is targeting the high-end product market, and its independently developed Epioneer series high-end preform intelligent molding systems have successfully entered emerging markets in Southeast Asia, Africa, and the Middle East.

Changes in the demand structure of downstream industries drive product technology upgrades.The continuous release of demand from downstream industries represented by new energy vehicles, household appliances, and high-end packaging has driven the growth of high-end injection molding machines. Haitain International's Mars and Jupiter series have achieved rapid growth by adapting to the needs of the new energy vehicle and household appliance industries; Yizumi's die casting machine business has benefited from a 33.29% increase in investment in the new energy vehicle industry chain; Jinming Precision's high-barrier membrane products have expanded applications in the new energy field. These all reflect the driving effect of downstream demand upgrading on the equipment manufacturing industry.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

【Overseas News】Shipping traffic in the Strait of Hormuz has sharply declined! South Korea approves the reorganization of Liuzhi Petrochemical; Italy shuts down the PE plant

-

Versalis Shuts Down Polyethylene Plant in Brindisi, Italy

-

[Overseas News] US Senate Approves Bill! SABIC Collaborates with Saudi Automobile Brand! Anti-fog Biodegradable Film Launched