Cost Supply Jointly Pushes PC Prices Up, Can "Silver Ten" Continue After the Holiday?

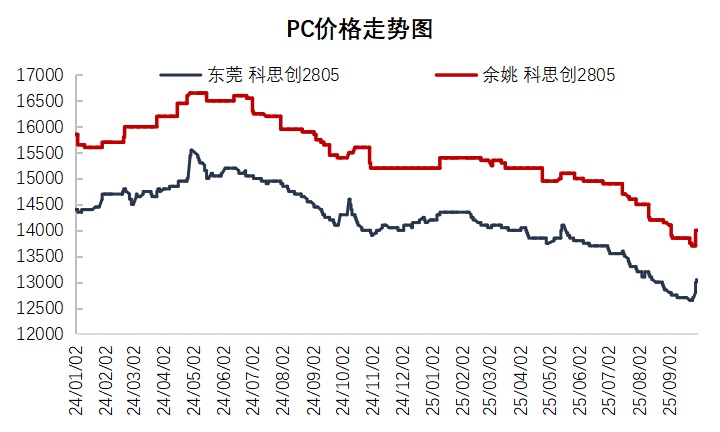

Recently, domestic polycarbonate (PC)The PC market, which had been in a prolonged slump, began a wave of volatile upward movement starting from mid to late September. The shift in the market's focus is not driven by strong demand, but rather...Cost pressures continue to increase. Maintenance expectations are concentrated on the supply side.The result of joint action. AsAs the traditional peak season of "Golden September and Silver October" enters its later stage, whether the PC market can continue its upward trend after the holiday has become a focal point of industry attention.

Cost provides strong support, supply shrinkage expectations, jointly promote.PC price increase

The core driving force behind the price increase of PC comes from strong support on the cost side and expected contraction on the supply side. As a key raw material for PC production, bisphenol A accounts for a significant proportion of production costs; approximately 0.9-0.95 tons of bisphenol A are required to produce 1 ton of ordinary PC via the phosgene method. Since late August, due to the impact of industry profit losses, some bisphenol A facilities have undergone early maintenance or reduced operating rates, leading to a tightening supply that has rapidly pushed prices up. Although the initial price increase for PC lagged, the price gap between upstream and downstream narrowed to 2400 yuan/ton, the lowest level of the year, which has significantly increased cost pressure on the industry, forcing the market to stabilize and support prices.

The shift in supply-side expectations has become another key driver of rising prices.In late September, after the announcement of the maintenance plans by enterprises such as Lihuayi Weiyuan, the market realized that the supply contraction for the fourth quarter was a foregone conclusion. According to statistics, in October, a total of 45 PC units in China will undergo maintenance, involving a production capacity of 467,000 tons. Among them, Lihuayi Weiyuan's 130,000-ton unit will undergo 45 days of maintenance, and Jiaxing Teijin's 150,000-ton unit will undergo one month of maintenance. Combined with maintenance of foreign units such as LG Chem and Thailand Mitsubishi, both domestic and foreign supplies are showing a reduction trend. Under the expectation of supply contraction, holders are reluctant to sell and are firm on prices, while traders are increasing their operations to fill the gaps, collectively pushing the market focus upward.

PC Market Outlook: Fluctuating Upward Amidst Mixed Factors

After the National Day holiday,The PC market is about to enter a critical period in October. Its trend will be the result of a three-way game between cost, supply, and demand, and it is expected to show an overall pattern.Fluctuating with a strong bias.The pattern is established, but the upward space may be limited.

1. Raw material Bisphenol A: Support remains, but upward momentum is lacking.

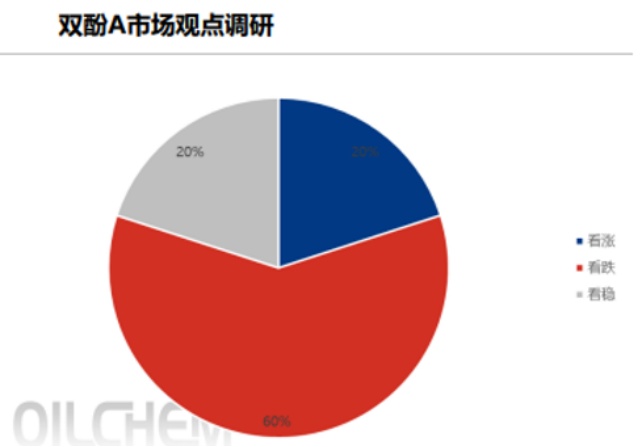

Raw material bisphenol The bisphenol A sector faces difficulties in providing sustained positive support. Although there are plans for maintenance involving three bisphenol A units, including Changchun Chemical, in October, with a total annual capacity of 770,000 tons, the overall supply in the industry remains relaxed. 60% of market participants are bearish on the October bisphenol A market, primarily due to the expected commissioning of new units combined with weak downstream demand. It is anticipated that the bisphenol A market will predominantly experience weak fluctuations in October. While the low operation level of bisphenol A may weaken the cost transmission momentum for PC (polycarbonate), the current PC price is at a historical low, which can still provide bottom support from the cost side.

2. PC Self-Supply: Certain Reduction is the Biggest Advantage

The core benefit for the PC market in October undoubtedly comes from the supply side. As mentioned earlier, the concentrated maintenance at the beginning of the fourth quarter will lead to a significant tightening of supply. In addition, inventory levels at both factories and traders are currently low, with most factories relying on pending orders for support. This "low supply, low inventory" situation gives sellers strong confidence to maintain prices, and it is expected that market quotes will still have room for increase after the holiday.

3. Downstream and terminal demand: Mild improvement, but difficult to become a strong engine.

The performance on the demand side will be the key to determining the extent and duration of the price increase.

- Downstream industry differentiation:Starting from mid to late September, orders in downstream modified industries have shown a significant improvement, leading to an increase in procurement of phosgene-based PC, which has been the main driving force behind recent market activity. However, demand from other application areas remains sluggish, with overall basic demand providing support but lacking momentum for price increases.

- Terminal Consumer OutlookIn the fourth quarter, traditional consumer electronics and home appliances enter a seasonal peak, and orders are expected to increase sequentially. The automotive industry may also accelerate production to achieve annual targets.PC demand provides certain support. However, overall, the recovery of terminal consumption is limited, making it difficult to serve as a strong driver for a significant increase in the PC market.

In summary, after the holiday.The PC market is expected to experience a volatile upward trend amid the "strong supply benefits" and the "weak demand reality."

Short term (In October, under the dual effects of cost support and reduced supply, the price level of PC will continue to rise, making the market more inclined to increase than to decrease. Pay close attention to the pricing dynamics of various factories and the actual implementation of their maintenance plans.

Medium to long term (From November to December: The market may show a "rise first, then fall" pattern. In November, due to ongoing maintenance, the tight supply situation will be maintained, and prices may continue to rise. After December, as maintenance facilities gradually restart, supply pressure will increase. If demand does not keep pace, there is a risk of price correction.

Risk Warning: Two points need close attention. One is whetherPC prices continue to rise, but cost transmission remains sluggish. The possibility of production cuts at some non-integrated PC factories may increase, which could further strengthen benefits from the supply side. Secondly, there is the downstream acceptance of price increases and the sustainability of procurement. If the demand for restocking after the holiday is quickly released and then falls into a wait-and-see situation, the market's upward momentum will significantly slow down.

Author: Zhuan Suo Shi Jie Market Research ExpertZhao Hongyan

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift