Chinese companies going global in southeast asia: 36 Cases, 5 Golden Rules

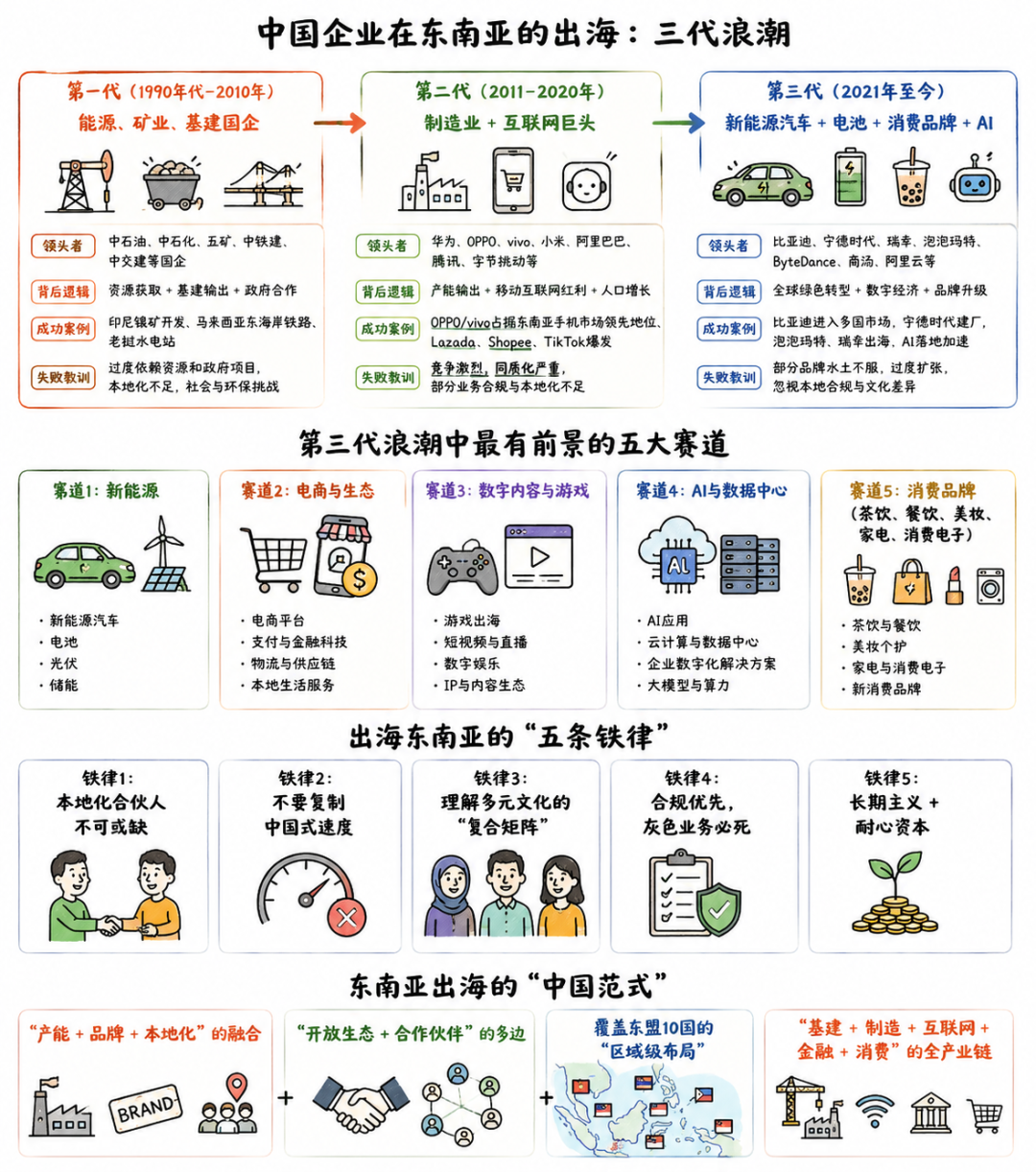

The overseas expansion of Chinese companies in Southeast Asia can roughly be divided into the following timeline:Three Generations of Waves:

·First generation(1990s-2010): Energy, Mining, Infrastructure State-Owned Enterprises

·Second Generation(2011-2020): Manufacturing Industry + Internet Giants

·Third Generation(2021 to present): New Energy Vehicles + Batteries + Consumer Brands + AI

The leaders of each wave, the underlying logic, the success stories, and the lessons from failures are all different.

The First Wave (1990s–2010): State-Led Energy and Infrastructure

From the 1990s to 2010 was the initial stage of China’s “Going Out” strategy, characterized by state-level resource security and strategic investment, with the main actors being —CNPC, Sinopec, CNOOC, PowerChina, CCCC, Chinalco, Sinosteel, and SINOMACH, etc.

Southeast Asia is one of the core destinations of China’s first wave of overseas expansion—oil and gas, minerals, and power.

Representative Cases

1. CNPC — Myanmar Natural Gas

From 2004 to 2013, CNPC took the lead in building the above-mentioned project.China–Myanmar oil and gas pipelineFrom Kyaukpyu Port in western Myanmar on the Bay of Bengal, crossing the entire country to Ruili in China’s Yunnan Province, and then onward to Guangxi, Guizhou, and Chongqing. This pipeline is a core part of China’s “overland energy lifeline,” currently transporting more than 5 billion cubic meters of natural gas and over 13 million tons of crude oil each year.

Sinopec - Indonesia

Sinopec acquired Indonesia through an acquisition in 2009.Natuna D-Alpha Gas FieldPartial equity stakes were the earliest major energy investments by Chinese state-owned enterprises in Indonesia.

CNOOC - Indonesia

CNOOC has multiple offshore oil and gas operational areas in Indonesia and is the main operator in the Strait of Malacca and the waters off eastern Indonesia.

4. POWERCHINA — Nam Ou Hydropower Station, Laos

The Nam Ou River Hydropower Station is a "cascade hydropower" project constructed by China Power Construction Group in Laos, consisting of seven power stations with a total installed capacity of 1.27 million kilowatts. It is the largest hydropower project in Laos and a core part of the "Battery of Southeast Asia" strategy.

5. MCC–Indonesia Ruiching Ferronickel

MCC Group established in Sulawesi in 2007.Ruiqing Nickel-Iron ProjectIt is an early representative of China's nickel-iron industry overseas, paving the way for the subsequent wave of nickel industrial parks in Indonesia.

6. China Railway—Indonesia Jakarta-Bandung High-Speed Railway

The Jakarta-Bandung High-Speed Railway is the first standard-gauge high-speed railway built by China overseas—142 kilometers long, with a maximum speed of 350 km/h, and opened in October 2023. CRRC supplied the high-speed EMUs, while China Railway International and China Railway Construction International undertook its construction, making it a landmark Chinese export to Indonesia.

The characteristics of the first generation and

Features:

Sovereign credit backing, long-term capital, high-level relationships with the host country’s government, and alignment with resource endowments.

Challenge: Translate the above content into English and output the translation directly, without any explanation.

Early-stage projects relied on “government relations” and lacked sufficient understanding of local laws, labor, and environmental regulations.

Lack of local operational experience - Many projects hire a large number of Chinese workers without cultivating local talent.

- Weak management of exchange rate risk - the depreciation of the Indonesian rupiah, Myanmar kyat, and Vietnamese dong has caused significant losses for Chinese enterprises multiple times.

ESG standards lag behind - environmental protests, labor accidents.

The second wave (2011–2020): manufacturing + internet giants

2011 was a “turning point” for Chinese manufacturing’s expansion into Southeast Asia: rapidly rising labor costs in China, the appreciation of the renminbi, and pressure for industrial upgrading prompted Chinese manufacturers to begin “actively relocating” overseas. At the same time, as the domestic market became saturated, Chinese internet companies began to globalize.

Manufacturing Industry Representative Cases

7. Hongdou Group — Sihanoukville Special Economic Zone, Cambodia

Wuxi Hongdou Group began constructing an "economic zone" in Sihanoukville, Cambodia in 2008, making it an early representative of Chinese private enterprises building parks overseas. Today, the Sihanoukville Economic Zone has approximately 200 resident companies and 35,000 employees.

8. Midea, Haier, TCL — Vietnam, Thailand

The three major Chinese home appliance companies began establishing manufacturing bases in Vietnam and Thailand in the 2010s.

·Midea Vietnam Factory(Beining and Pingyang): annual production capacity of 8 million air conditioners and 2 million washing machines.

·Haier Thailand Factory(Chonburi): Southeast Asia's refrigerator manufacturing base.

·TCL Vietnam FactoryTelevision and air conditioner exports to Europe and America.

Luxshare Precision, GoerTek - Northern Vietnam

The two major Chinese suppliers in the Apple supply chain, Luxshare Precision and Goertek, started establishing large factories in northern Vietnam (Bac Giang, Vinh Phuc) in 2017, becoming the core assembly providers for iPhones, AirPods, and Apple Watches in Vietnam.Luxshare Precision has more than 100,000 employees in Vietnam.is one of the largest Chinese-funded employers in Vietnam.

10. Shenzhou International, Bosideng — Southeast Asian Apparel

Shenzhou International, a leading Chinese apparel manufacturer and the largest supplier to Nike, Adidas, and Uniqlo, has established large-scale textile bases in Cambodia and Vietnam. Bosideng has set up down jacket production bases in Myanmar and Bangladesh.

11. Shandong Ruyi, Huafu Top Dyed Melange Yarn — Cambodia, Vietnam

A major Chinese textile dyeing and printing company has established an integrated cotton yarn, dyeing and printing, and garment production base in Cambodia and Vietnam.

12. Robam Appliances, Hisense — Southeast Asia

Robam Appliances has established kitchen appliance production bases in Thailand and Indonesia. Hisense has built Southeast Asia’s largest TV production line in Thailand.

Representative Internet Cases

13. Alibaba — Lazada

In 2016, Alibaba invested $1 billion in Lazada (one of the largest e-commerce platforms in Southeast Asia), and in 2017, it increased its stake to a controlling interest. In 2022, Alibaba continued to increase its investment. Lazada covers six countries: Indonesia, Malaysia, Singapore, the Philippines, Thailand, and Vietnam, making it a core part of Alibaba's Southeast Asia strategy.

14. Tencent System - Sea Group / Shopee

Tencent once held about a 23% stake in Singapore-based Sea Group (which operates Garena gaming, Shopee e-commerce, and SeaMoney financial services) and has since gradually reduced its holdings. Shopee is the largest e-commerce platform in Southeast Asia, with more than 450 million monthly active users and an estimated GMV of about US$110 billion in 2025.

15. JD.com — Tiki / J&T Express

JD.com invested in Vietnam’s Tiki (has since exited); meanwhile JD Logistics has deep cooperation with local logistics providers such as JNE. J&T Express (Jitu) is a courier company affiliated with BBK Electronics—the OPPO/vivo group—originating in Indonesia and listed in Hong Kong in 2023.

16. ByteDance—TikTok Southeast Asia

Since 2018, TikTok has made a major push into Southeast Asia. It now has over 150 million monthly active users in Indonesia, 65 million in Vietnam, 55 million in Thailand, 53 million in the Philippines, and 29 million in Malaysia—more than 300 million monthly active users in total.Southeast Asia is TikTok’s largest non-U.S. regional market globally.。

17. Meituan — Food Delivery (Exploration Stage)

Meituan began studying the Southeast Asian market in 2019, but progress was limited because Grab, Gojek, Foodpanda, and ShopeeFood had already established a stable market structure.

18. OPPO/vivo/Xiaomi/Transsion — Smartphones

Chinese mobile phone brands have aggressively entered Southeast Asia since 2014.

·OPPOEstablish assembly plants in Indonesia, Vietnam, Thailand, and Indonesia; Southeast Asian market share is approximately 22% in 2025.

·vivoThe market share in Southeast Asia is about 18%.

· Southeast Asian market share is approximately 16%.

· (Transsion): It ranks first in Africa, but its performance in Southeast Asia is average.

Chinese smartphones account for over 60% of the Southeast Asian smartphone market—one of the most important achievements of China's Internet + hardware going abroad.

Characteristics of the second generation

Features:

Respond to the impact of the China-U.S. trade war.

·Southeast Asia’s moderate labor costs (approximately 50–70% of China’s).

ASEAN Free Trade Area + RCEP brings tariff benefits.

The rapid rise of the Southeast Asian consumer market - young, urbanized, and widespread smartphone adoption.

Challenge: Translate the above content into English, output the translation directly without any explanation.

Insufficient localization depth — many manufacturing enterprises only relocate production lines to Southeast Asia, but lack operational depth in cultivating local management personnel and in building processes and supply chains.

Underestimating labor laws and union power — labor protests in Vietnam and Indonesia have repeatedly led to factory shutdowns.

Brand power is insufficient — apart from mobile phones, Chinese brands’ “premiumization” in Southeast Asian consumer markets (home appliances, automobiles, and food) still lags behind that of Japanese and Korean brands.

The Third Wave (2021–Present): New Energy + AI + Global Brands

2021 marked a new turning point for Chinese companies expanding into Southeast Asia. Several key changes took place that year:

·The U.S.-China trade war has entered a stage of "industrial decoupling."The restrictions in the semiconductor, AI, and biopharmaceutical fields are becoming increasingly strict.

·China’s new energy industry chain is globally leading.Batteries, photovoltaics, and electric vehicles are already in oversupply in China and must expand overseas.

·The infrastructure in the Southeast Asian market is already mature.Payment, logistics, e-commerce, and consumer mindset have all been established.

·The Belt and Road Initiative Enters Its Second Decade—Shifting from an infrastructure-led model to a three-pronged approach driven by “infrastructure + industry + digitalization.”

The core characteristics of the third wave.From “exporting production capacity” to “exporting systems”Chinese companies are no longer just relocating their factories there; they are moving entire industrial chains, brands, technologies, and ecosystems to Southeast Asia.

Representative Cases of New Energy

BYD - The King of Electric Vehicles in Southeast Asia

Since 2022, BYD has accelerated its expansion in Southeast Asia:

·Factory in Rayong Province, ThailandAnnounced investment in 2022, officially commenced production in July 2024, and expanded annual capacity to approximately 200,000 vehicles in 2025, it is BYD’s first overseas vehicle manufacturing plant.

·Indonesian factoryAnnounced an investment of $1.3 billion in 2024, construction to begin in 2025, and mass production in 2026.

·Vietnam, Malaysia, CambodiaFull coverage of the sales network.

In 2025, BYD’s market share in Thailand’s electric vehicle market exceeded 40%; it also grew rapidly in Singapore, Malaysia, and the Philippines.

Great Wall Motors - Thailand, Malaysia

In 2021, Great Wall Motors acquired General Motors’ Rayong plant in Thailand, which is the largest base for Chinese SUVs in Southeast Asia. The Ora, Tank, and Haval brands are sold in Southeast Asia.

21. SAIC-GM-Wuling — Indonesia

The Wuling Air EV (Indonesian version) was released in 2022, priced at approximately 18.5 million Indonesian rupiah (around $8,000). It is the best-selling electric vehicle in Indonesia, with a single model market share exceeding 55% by 2025.

Chery - Southeast Asia Multiple Countries

Since 2022, Chery has been opening stores on a large scale in Malaysia, Indonesia, Thailand, Vietnam, and the Philippines — in 2025, Chery’s electric vehicle sales in Malaysia continued to exceed BYD’s.

Geely - Proton (Malaysia)

In 2017, Geely acquired a 49.9% stake in Malaysia's national car Proton—using Proton to sell Geely's Boyue, Lynk & Co, and Zeekr in Southeast Asia, serving as a for Chinese brands "going overseas through a shell."

24. CATL—Indonesia Nickel Industrial Park

In 2022, CATL and an Indonesian state-owned enterprise.AntamJointly establish with Rock Lithium Industry.CBLProject — A US$6 billion investment to build a full-industry-chain battery base in North Maluku, comprising nickel smelting, battery precursors, cathode materials, and battery cells. This is the largest overseas investment by China’s battery industry chain.

25. Qingshan Holding - Sulawesi, Indonesia

Tsingshan Holding'sIMIP (Morowali Industrial Park, Indonesia)+IWIP (Weda, Indonesia) Bay Industrial ParkWith cumulative investment exceeding US$20 billion, it is the world’s largest production base for stainless steel and ferronickel. From here, the downstream chain extends to battery precursors, battery cathode materials, and battery cells.Chinese capital accounts for more than 90% of Indonesia's nickel industry chain.。

26. Huayou Cobalt, Liqin Resources, Weiming Environmental - Indonesia, Philippines

China’s “three nickel giants” have established large-scale nickel smelting and battery precursor plants in Sulawesi and Maluku, Indonesia, as well as in the Philippines.

27. LONGi Green Energy, JA Solar, Canadian Solar, Trina Solar — Vietnam, Malaysia, Thailand

The production capacity of China’s solar “photovoltaic four giants” in Southeast Asia:

· Approximately 30 GW of solar panel production capacity.

·MalaysiaAbout 15 GW, including the full industrial chain of silicon wafers, cells, and modules.

· Approximately 10 GW.

In 2024, the United States initiated an "anti-circumvention" investigation into solar products imported from Vietnam, Malaysia, Thailand, and Cambodia, and starting from 2025, will impose high tariffs (with some products exceeding 250%) which will have a significant impact on China's photovoltaic in Southeast Asia.

Representative Cases of Internet and Consumer Brands

28. Shein—Localized Supply Chain in Southeast Asia

Since 2022, Shein has established local warehouses and supply chains in Southeast Asia (Thailand, Indonesia, and Vietnam), with its revenue in Southeast Asia exceeding US$7.5 billion in 2025. Shein’s headquarters has been relocated to Singapore.

29. Temu (Pinduoduo overseas version) — Southeast Asia

Temu entered Southeast Asia in 2024—launching in the Philippines, Malaysia, and Thailand in August, and in Vietnam in November. By the end of 2025, Temu had over 20 million monthly active users in the Philippines and over 15 million in Malaysia.

30. TikTok Shop—The New King of E-commerce in Southeast Asia

TikTok Shop launched in Indonesia in 2022 and, by 2024, became the third-largest e-commerce platform in Southeast Asia, behind only Shopee and Lazada. In 2025, its GMV in Southeast Asia was approximately US$43 billion. However,Indonesia banned TikTok in September 2023. ShopTikTok re-entered Indonesia’s e-commerce market by acquiring Tokopedia, Indonesia’s largest local e-commerce platform, in a deal worth approximately $1.5 billion.

31. J&T Express — Southeast Asia

J&T Express (backed by the Bubugao Group, with investment from Duan Yongping, founder of OPPO and vivo) originated in Indonesia and has grown into one of the largest express delivery companies in Southeast Asia — with daily parcel volume in Southeast Asia exceeding 25 million in 2025. It was listed in Hong Kong in 2023.

32. Cainiao, JD Logistics, SF Express — Cross-border Logistics in Southeast Asia

Cainiao has established "Southeast Asia Distribution Centers" in Malaysia and Thailand; JD Logistics has set up overseas warehouses in Singapore and Malaysia; SF Express has acquired the Asian logistics giant Kerry Logistics, covering multiple countries in Southeast Asia.

33. miHoYo, Lilith, NetEase — Game Going Global

Chinese gaming companies’ performance in Southeast Asia: Genshin Impact has over 15 million monthly active users in Southeast Asia; Lilith Games’ AFK Arena and Rise of Kingdoms have long ranked near the top of the charts in Southeast Asia; NetEase’s Eggy Party and Naraka: Bladepoint are growing rapidly in Southeast Asia.

34. MIXUE, Luckin Coffee, Cotti Coffee — Food and Beverage Brands Going Global

Since 2022, Chinese tea beverage and coffee brands have been expanding aggressively into Southeast Asia.

·Mixue Ice Cream & TeaIn Indonesia, Vietnam, Malaysia, Thailand, and the Philippines, there are over 4,000 stores combined, making it the Chinese restaurant brand with the most outlets in Southeast Asia.

·Luckin CoffeeStarting from 2023, entering Singapore, Malaysia, and Indonesia.

·Cotti CoffeeRacing to enter Southeast Asia alongside Luckin.

·HEYTEA, CHAGEE, ChaPandaOpen stores in Singapore and Kuala Lumpur.

35. Florasis, Perfect Diary, JOOCYEE — Beauty Brands Going Global

Chinese emerging beauty brands made a concentrated push into Southeast Asia from 2023 to 2025—Florasis sold through TikTok Shop and Shopee in Malaysia, Indonesia, and Thailand; Perfect Diary entered offline channels in Singapore.

DJI - Drones

DJI is the absolute leader in consumer drones in Southeast Asia, with a market share of over 70%.

Characteristics and Challenges of the Third Generation

Features:

Complete industrial chain collaboration - from raw materials to batteries to vehicles to charging stations to financial services.

A threefold output of brand, technology, and localization — not just low price.

Capitalize on the consumption upgrade window—Southeast Asian consumers no longer see Chinese brands as synonymous with being “cheap.”

Ecosystem strategy—integrating TikTok, Shopee, logistics, payments, and influencers.

Unresolved Challenges:

Uncertainty regarding the United States' "anti-circumvention" tariffs.

Southeast Asian countries are wary of the “excessive concentration” of Chinese capital.

International standards on ESG, labor rights, and environmental protection.

The depth of talent localization.

Five tracks

Induce the most promising directions in the third wave, which can form.Five tracks:

Track 1: New Energy (Batteries + Electric Vehicles + Photovoltaics)

·Market sizeThe Southeast Asian electric vehicle market is expected to reach $300 billion by 2030.

·Core countriesThailand, Indonesia, Malaysia, and Vietnam.

·Core playersBYD, CATL, Tsingshan, Great Wall, Chery, Wuling, CATL, LONGi.

·Core OpportunitiesLocal assembly + local batteries + charging network + consumer finance + used car recycling.

Track 2: E-commerce and Ecology

·Market sizeSoutheast Asia’s e-commerce GMV is approximately US$125 billion in 2025 and is expected to reach US$400 billion by 2030.

·Core playersShopee (Tencent), Lazada (Alibaba), TikTok Shop (ByteDance), Temu (Pinduoduo), Shein.

·Core OpportunitiesLive streaming e-commerce + short videos + influencer marketing + local warehouses + overseas supply chain + cross-border payment.

Track 3: Digital Content and Gaming

·Market sizeSoutheast Asia’s digital entertainment market is approximately USD 20 billion per year.

·Core playersTikTok, miHoYo, NetEase, Lilith Games, Tencent Games.

·Core OpportunitiesLocalized game development + overseas publishing + IP partnerships + influencer economy.

Track 4: AI and Data Centers (see the next for details )

Track 5: Consumer Brands (Tea Beverages, Food & Beverage, Beauty & Cosmetics, Home Appliances, Consumer Electronics)

·Core playersMixue Ice City, Luckin Coffee, Haidilao, Huaxizi, Xiaomi, Haier, TCL, Midea.

·Core OpportunitiesThe consumption upgrade window for Southeast Asia’s 690 million population; China’s “cost-effectiveness + innovation” advantage.

Five Iron Rules for Expanding into Southeast Asia

The experiences and lessons learned from the three waves of Chinese companies going abroad to Southeast Asia can be summarized as follows.Five Ironclad Rules:

Rule 1: Local partners are indispensable

Southeast Asian countries each have powerful local conglomerates—Indonesia’s Sinar Mas, Lippo, and Salim Group; the Philippines’ SM, Ayala, and JG Summit; Thailand’s CP, TCC, and Central; Malaysia’s Genting, Berjaya, and Sime Darby; and Singapore’s Temasek-linked groups.Without a local partner, foreign-invested enterprises find it difficult to truly establish themselves.BYD’s joint venture with CP in Thailand, TCL’s partnership with VietHan in Vietnam, and Huawei’s collaboration with PT Telkom in Indonesia—all are worth referencing.

Iron Rule 2: Do Not Imitate the Chinese-Style Speed

Legal, regulatory, labor, land, and tax procedures in Southeast Asia are far slower than in China. The “aggressive playbook” of many Chinese companies—such as pouring in massive amounts of money to seize market share—can trigger vigilance and pushback from local governments. Indonesia’s ban on TikTok Shop, the Philippines’ ban on POGOs, and Malaysia’s requirement that Country Garden’s Forest City change its target buyers are all prices paid for violating this iron rule.

Iron Law 3: Understanding the "Composite Matrix" of Multiculturalism

Southeast Asia is not one market; it is 10 different markets.Indonesian Muslims, Thai Buddhists, Filipino Catholics, Singapore’s multicultural society, Vietnamese Confucian cultureProducts, marketing, and HR all need to be deeply localized. One of the keys to the success of Haidilao and Mixue Bingcheng in Southeast Asia is the deep localization of their menus, including halal versions, vegetarian options, and adjusted spice levels.

Rule 4: Compliance First, Gray Area Businesses Must Die.

Southeast Asia’s “gray businesses” have already been jointly cracked down on by the governments of various countries and the Chinese government. Companies that rely on “gray areas” will ultimately suffer a severe blow.Compliance, tax transparency, and ESG standards have already become hard thresholds in Southeast Asia.。

Iron Law 5: Long-Termism + Patient Capital

Southeast Asia is not a place to “make quick money.” Temasek’s success in Singapore took 50 years; Lee Kum Kee’s roots in Malaysia took 80 years; and Charoen Pokphand Group’s cooperation in China has lasted 40 years.Chinese companies willing to spend 10 years putting down roots in Southeast Asia.Only then will there be an opportunity.Become the next generation of global giants.。

The “Chinese Model” for Expanding into Southeast Asia

After more than three decades of practice, Chinese enterprises have developed a distinctive “go-global” model in Southeast Asia.

"Capacity + Brand + Localization" integration.

· “Open ecosystem + partners” multilateral.

A “regional-level presence” covering all 10 ASEAN countries.

"Full industry chain of 'infrastructure + manufacturing + internet + finance + consumption'."

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Kingfa Sci. & Tech., 1,000-Ton Pilot PEI Line Put Into Production! Polyetherimide: Who Is Laying Out the Market, and What Is the Production Capacity?

-

2026 Electronic Components Price Increase Notice

-

A Look at the Material Suppliers Behind SpaceX

-

Chinese companies going global in southeast asia: 36 Cases, 5 Golden Rules

-

Basf exits joint venture with cnpc! chinese refrigeration products sell explosively overseas! south korea plans to build chip factory