China's Fifth Round Collective Price Increase for Titanium Dioxide Falls Short of Consumer Market Expectations

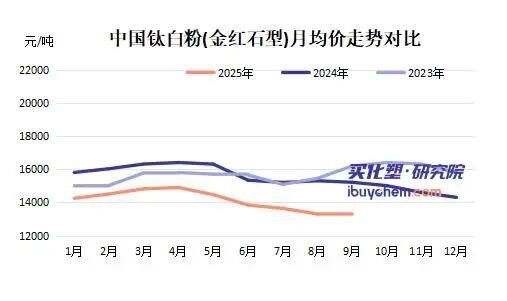

According to Huizheng Information andBuy Chemicals and PlasticsAccording to the research institute's data, from mid-September to early October 2025, Chinese titanium dioxide suppliers implemented the fifth round of price increases, raising domestic trade prices by 300 RMB/ton and export prices by 40-50 USD/ton. As a result, the cumulative increase over the five rounds reached 1900-2400 RMB/ton. However, the actual market prices compared to the same period last year and the beginning of the year have declined (the market price of rutile titanium dioxide dropped by 12.55% year-on-year and by 6.63% since the beginning of the year). This reflects the complex market contradictions behind the price increases.

Titanium dioxide is facing weak demand on the consumer end, and the price transmission mechanism is failing.The main downstream application of titanium dioxide is in architectural coatings; however, the current real estate industry is sluggish, leading to insufficient demand for architectural coatings. The competition in the terminal market is fierce, making it difficult for coating companies to pass the rising costs of titanium dioxide onto consumers, resulting in price increase notices being challenging to implement. Research from the Buy Chemical Plastics Research Institute indicates that despite multiple price hikes by companies, actual market prices have not risen but rather fallen due to weak downstream demand. This shows that the support from the domestic market is weak, and price increases are more of a "passive response" from suppliers rather than being driven by demand.

As the world's largest producer of titanium dioxide, China's export volume of titanium dioxide has declined year-on-year, with international trade barriers intensifying.From January to August 2025, China's total titanium dioxide exports amounted to 1.1901 million tons, marking a year-on-year decrease of 7.95% (a reduction of approximately 102,800 tons). Among these, the export of chloride process titanium dioxide fell by 3.38%, while the export of sulfate process titanium dioxide dropped by 8.96%. This decline partly stems from anti-dumping investigations and tariff barriers imposed by various countries on Chinese titanium dioxide (such as anti-dumping measures by India and the EU), which have obstructed exports. Meanwhile, import data also shows weakness, with total imports at 50,500 tons, a year-on-year decrease of 20.16%, indicating a deteriorating global trade environment and insufficient outward growth momentum for China's titanium dioxide.

While foreign and domestic trade are facing difficulties, the cost pressures for titanium dioxide enterprises continue to increase.The main raw materials for the production of titanium dioxide are titanium ore and sulfuric acid. In recent years, due to environmental policies, rising energy prices, and other factors, upstream costs have continued to climb. For example, titanium ore prices have remained high, and energy and environmental costs in the sulfuric acid production process have increased. Suppliers have attempted to transfer the cost pressure through five rounds of price increases, but insufficient downstream demand and market competition have led to an actual decline in market prices. This reflects that cost-driven price increases are being hindered on the demand side, compressing the profit margins of enterprises.

On September 13, Venator Asia announced the suspension of production, while some factories in Europe were closed due to the energy crisis and environmental pressures, reducing the global supply of titanium dioxide.Theoretically, this is beneficial for China's titanium dioxide exports and price increases, but the actual decline in export data indicates that weak global demand and trade barriers have offset the positive effects of reduced supply. Chinese titanium dioxide companies are trying to seize the market by raising prices, but constrained by weak domestic and export demand, global changes have not brought significant benefits.

Currently, the five rounds of price increases reflect the struggles of suppliers under pressure from costs, global supply, and internal factors. However, insufficient market demand and obstacles to exports have significantly diminished the effectiveness of these price hikes, resulting in an overall weak market. In the short term, the titanium dioxide market is likely to continue in a state of "high prices but low sales," making it difficult for price increases to be sustained. Companies need to optimize their product structure (such as developing high-end products using the chloride process) and explore emerging markets to address these challenges.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift