Auto Industry Profit Margin Drops to 3.2% in Q1, Reflecting Sector-Wide Struggles

In the first quarter of 2026, China's automotive industry released a set of noteworthy figures. According to data cited by Cui Dongshu’s WeChat account, the industry’s profits declined by 18% year-on-year, and the sales profit margin fell to a low of 3.2%. Examining this phenomenon from the perspectives of cost structure and profit distribution across the supply chain reveals deep-seated structural pressures facing the automotive industry.

Upstream costs remain high, and the automotive industry’s profit margins continue to narrow.

According to statistics cited by Cui Dongshu's WeChat account, China's automobile production from January to March 2026 totaled 7.15 million units, a 6% year-on-year decline; the industry's total revenue was approximately RMB 2.4128 trillion, down 0.2% year-on-year; while total costs reached RMB 2.1406 trillion, up 0.7% year-on-year.

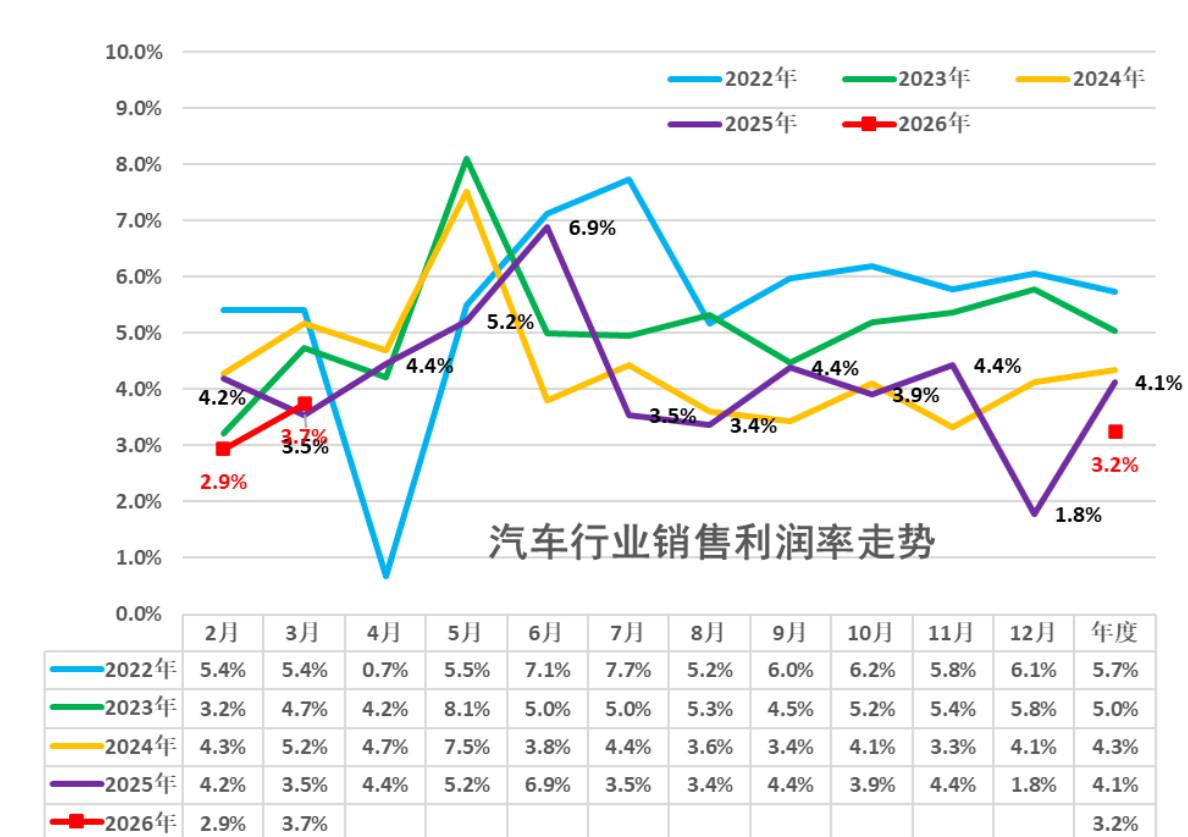

Image source: Cui Dongshu

Under the dual pressures of declining revenue and rising costs, the total profit of the automotive industry in the first quarter was only 784 billion yuan, a year-on-year decrease of 18%, with the sales profit margin further dropping to 3.2%. Although the profit margin for March alone warmed up to 3.7%, an improvement from 2.9% in January-February, it still has a significant gap compared to the 6% average profit margin of downstream industrial enterprises.

The decline in profits is closely related to the continuous rise in upstream raw material prices from a more macro industrial perspective.

The price of lithium carbonate, from a low point of about 75,000 yuan/ton in 2025, climbed all the way up to breaking through 180,000 yuan/ton in the first quarter of 2026, an increase of more than double. According to Shanghai Nonferrous Metals Market (SMM) quotes, the average price of lithium carbonate in the first quarter stabilized within the range of 150,000 to 160,000 yuan/ton, a significant increase compared to the same period last year. According to relevant institutions' calculations, the rise in lithium carbonate prices alone could potentially increase the battery cost per electric vehicle by about 3,000 to 5,000 yuan. The prices of commodities such as copper and aluminum are also at relatively high levels in history, with the prices of 6 types of non-ferrous metals in the first quarter increasing by 11.8% to 30.4% year-on-year.

Against this backdrop, the non-ferrous metals industry saw a significant increase in profits in the first quarter of 2026, and the high volatility of lithium carbonate prices also activated the profit elasticity of lithium mining companies.

According to data released by the National Bureau of Statistics for the first quarter, profits of nationally designated industrial enterprises rose by 15.5% year-on-year, exceeding RMB 1.69 trillion. Profits in the equipment manufacturing sector increased by 21% year-on-year, while those in the high-tech manufacturing sector surged by 47.4%. Profits in the raw materials manufacturing sector grew by 77.9% year-on-year in the first quarter, with the non-ferrous metals industry seeing a remarkable profit increase of 116.7%.

Image source: Huaban.com

In the upstream sector, lithium battery-related listed companies have shown particularly strong first-quarter performance. As of April 27, 2026, a total of 29 listed companies in the lithium battery supply chain have disclosed their first-quarter earnings reports, with 15 reporting year-over-year growth in net profit and 3 turning losses into profits. CATL reported attributable net profit of RMB 20.738 billion for the first quarter, an increase of 48.52% year-over-year, exceeding the full-year net profit of any Chinese automaker in 2025 except BYD.

Upstream lithium mining companies have seen their earnings surge by several times. In contrast, lithium battery export prices have continued to decline, while domestic battery prices have kept rising, putting greater profit pressure on automakers that do not directly engage in battery production.

The sustained high level of upstream raw material prices is causing the impact on the automotive industry to deepen from the cost side to the operational side. On one hand, batteries, the core component with the highest cost proportion in electric vehicles, have seen their prices rise along with lithium carbonate, directly increasing the cost of vehicle manufacturing. However, due to intense price competition at the end-user level, automakers find it difficult to fully pass on the increased costs to consumers, resulting in a significant compression of profit margins.

From the perspective of single-vehicle cost, the automotive industry's single-vehicle cost in the first quarter has increased to 299,000 yuan, a growth of 6.3%, higher than the 5.4% growth rate of single-vehicle revenue, leading to a decrease in single-vehicle gross profit to 11,000 yuan, a decline of 13.2%.

On the other hand, automakers that do not possess battery production capacity are at a disadvantage in pricing negotiations, while companies with vertical integration capabilities have a relatively greater buffer in terms of costs. Moreover, the structural imbalance between surging upstream profits and sharply declining downstream profits may lead to continued loss pressures for some small automakers if upstream resource prices remain high, potentially accelerating industry consolidation.

Policy Guidance and Competition Regulation: External Variables to Alleviate Profit Pressure

Faced with the continued decline in industry profit margins, relevant policy sectors have begun to intervene and regulate.

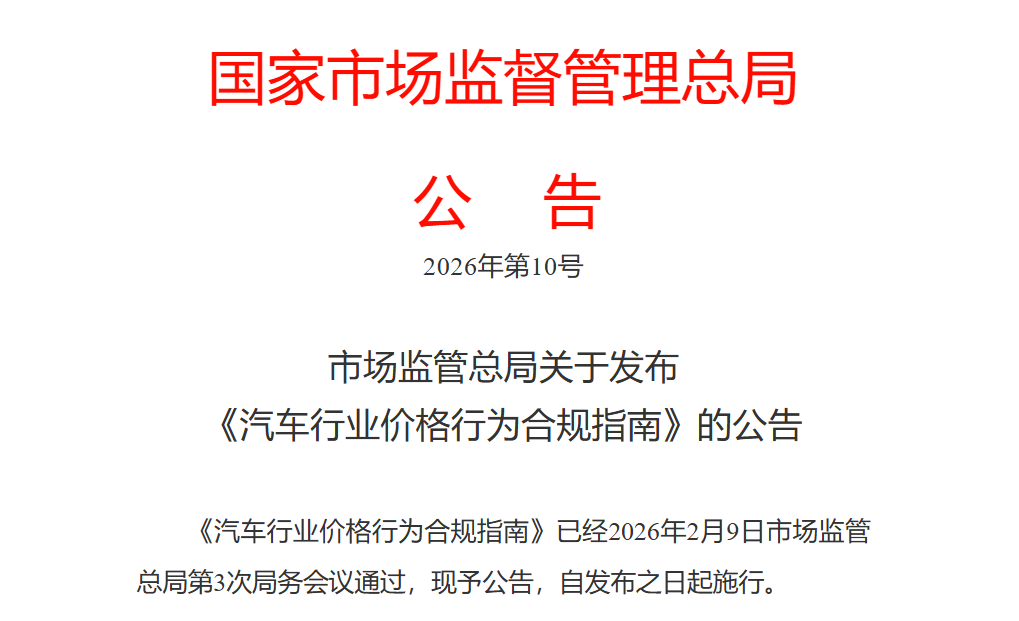

In the latter part of the first quarter, the Ministry of Industry and Information Technology, the National Development and Reform Commission, and the State Administration for Market Regulation jointly held a symposium with new energy vehicle industry enterprises, clearly stating that they will strengthen price monitoring and cost investigations and severely crack down on predatory pricing and other forms of cutthroat competition.

Source: State Administration for Market Regulation

The State Administration for Market Regulation has previously issued the “Compliance Guidelines for Automotive Industry Pricing Practices,” establishing regulatory red lines against collusive pricing, predatory pricing, and other such practices. Meanwhile, measures to further implement the Anti-Unfair Competition Law have also been rolled out. As the national campaign against “neijuan” (excessive internal competition) continues to advance, upstream industries’ profitability is expected to improve further.

From the internal logic of industrial chain profit distribution, car manufacturers not controlling battery production capacity is the structural reason for their weak position in cost negotiations. Cui Dongshu clearly pointed out, "The problem of car manufacturers not producing batteries is serious, and their profits will continue to decline."

Against the backdrop of persistently high upstream resource prices and consecutive increases in battery prices, automakers lacking vertical integration capabilities face mounting profit pressure. In the medium to long term, extending operations upstream to gain control over core component production capacity may become one of the key pathways for automakers to improve their profit structure.

Overall, the profit pressure on the automotive industry caused by the high cost of upstream raw materials in the first quarter is expected to be somewhat marginally relieved in subsequent quarters, against the backdrop of the continuous regulation of industry competition by the three departments. In this process, the trend of upstream resource prices and the ability of car manufacturers to control costs in core components such as batteries will be the two key factors influencing the extent of the relief.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

First Time Surpassing $3 Billion! First Time Surpassing 100,000 Tons! Cathay Biotech’s 2025 Performance: Chemical Production Fully Phased Out, Biological Method Wins

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Completion And Commissioning! Evonik’s Four Major Projects Officially Launched