Assets Once Owned by Dow and Arkema Put Up for Sale

High value-added assets, once considered "hot commodities," are now being put on the shelf.

On August 26, according to the Korea Economic Daily, SK Group is accelerating its restructuring to obtain new funds, and its subsidiary SK Innovation (SKI) is planning to sell its overseas business units acquired from Dow and Arkema through a bundled transaction.

These businesses include the Dow ethylene acrylic acid (EAA) and polyvinylidene chloride (PVDC) operations acquired in 2017 for $370 million, as well as the Arkema functional polyolefin business acquired in 2020 for $317 million. These acquisitions once reflected SK's ambition to enter the environmentally friendly high-value packaging market, but have now declined due to post-pandemic oversupply, intensified competition from China, and integration difficulties. At the same time, this sale is also part of SK Group's broader restructuring, involving petrochemical capacity cuts, subsidiary mergers, and multiple asset divestitures, driven by the industry's prolonged downturn and weaker-than-expected demand for electric vehicles.

"Bottom-fishing" the materials business of international giants

One major background to SKI's acquisition of related businesses from Dow and Arkema is the merger between Dow and DuPont. To avoid monopoly issues after the merger, both parties explored spinning off Dow's EAA business and independently operating DuPont's Nucrel EAA production line. Meanwhile, Arkema was also undergoing strategic adjustments to focus its business on specialty materials, intending to divest its plastics business (functional polyolefins business being part of Arkema's PMMA business).

These two acquisitions represented an excellent opportunity for SKI, originally Korea's first refining and chemical enterprise, to rapidly obtain world-class technology and supporting assets. SKI had high hopes for these businesses at the time, aiming to cultivate one of the world's top ten chemical companies. However, SKI now has to face the reality of deteriorating performance and integration difficulties. Currently, the group's strategic focus has also shifted.

In the second quarter of 2025, although SKI still reported a loss of nearly $300 million, its battery segment reached a turning point: SK On, its main subsidiary focusing on power batteries, achieved quarterly profitability for the first time. Currently, SK On is being integrated into its sister company SK Enmove (lubricants and immersion cooling fluids). Through business synergy and capital restructuring, they aim to build a top-tier comprehensive energy company for the electrification era.

If the West is not bright, is the East bright?

Chemical new materials are a fundamental industry of the national economy. High-performance polymers, functional composite materials, semiconductor materials, bio-based degradable materials, nano-catalytic materials, chemical energy storage materials, and photoelectric conversion materials, among others, play important roles in emerging strategic industries. In the past two years, high-end polyolefins represented by EAA have become one of the focal points for domestic new material enterprises.

From 2021 to 2023, Satellite Chemical, a leading domestic acrylic acid company, has partnered with SKGC to introduce their technology through a joint venture. They plan to invest approximately 3.8 billion yuan to jointly construct a project with a capacity of 90,000 tons per year for an EAA facility. The first phase of the 40,000-ton project is still under construction and was originally planned to commence production by the end of 2025. This project is also SKGC's first related facility in Asia, following their installations in the United States and Spain, which have a combined capacity of about 60,000 tons.

At present, EAA (ethylene acrylic acid copolymer) is considered a "small but refined" new material, with relatively low global market demand. Before Satellite Chemical entered the market, nearly 90% of the market share was held by DuPont (72,000 tons/year), INEOS (57,000 tons/year), Mitsui (56,000 tons/year), SK, and ExxonMobil (28,000 tons/year). This type of high-molecular polymer, produced by the copolymerization of ethylene and acrylate monomers, is mainly used in downstream sectors with relatively low added value, such as soft packaging for food and pharmaceuticals, as shown in the figure below (photographed at Chinaplas 2024):

|

|

From the perspective of domestic substitution, since this application field involves product certification in the aseptic industry and the certification process is lengthy, major companies such as Tetra Pak and Combi may still rely mainly on imported products for some time in the future.

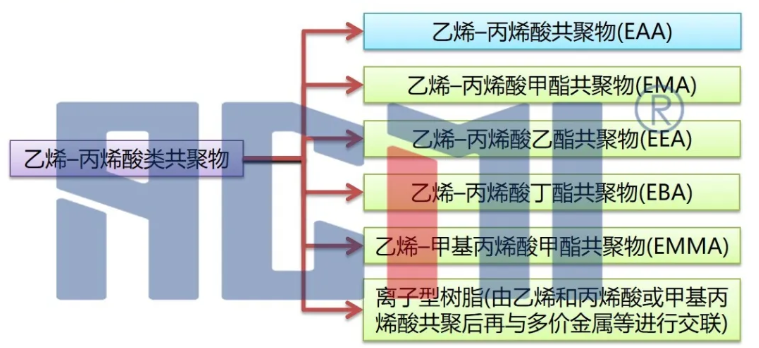

However, depending on the type of acrylate monomer used during polymerization, these materials can be further extended into various products such as EMA, EEA, EBA, and EMMA, each with its strengths, capable of tapping into different downstream markets.

EMA's downstream sectors span across medical, modified plastics, and automotive lightweighting: from medical gloves and aseptic packaging to the room temperature toughening of high polymers such as ABS, PA, PC, PET, and PP, and further to automotive sound insulation and foaming materials. The global market is dominated by the United States, with major producers including DuPont, Dow, ExxonMobil, Westlake Chemical, Arkema, Borealis, and SKGC. Among them, DuPont holds the global lead in both quality and scale with a full range of general, food-grade, and film-grade capacities.

EEA can be extended downstream to modified plastics and the electronic and electrical fields. Blending and modifying it with olefins or engineering polymers can improve the impact resistance of polyamides and polyesters. In addition, EEA has good electrical insulation properties and can be used for electrical insulation materials.

In recent years, with the continuous development of industries such as special wires and cables, high-end packaging films, and sealants in regions/countries like Europe, America, and Japan, the downstream applications of EBA have been constantly expanding. The market size of this material is growing at a rate of over 10%. It can be used as an adhesive and coating additive, as well as in the bonding and heat-sealing layers of multi-layer composite films, and as a substitute for rubber in the backing adhesive of nylon carpets. Currently, only a few companies globally, such as DuPont, Arkema, Westlake Chemical, Germany's LUKOIL, and Spain's Repsol, have production capabilities.

Compared with several other products, EMMA has higher hardness and rigidity, as well as transparency. These characteristics give it great potential for applications in the fields of transparent packaging, automotive interior parts, optical lenses, and other optical products.

It is also worth mentioning that from a production perspective, the process flow of materials like EAA is similar to that of EVA, both of which are improved based on high-pressure polyethylene production units. There have been large domestic petrochemical enterprises that have planned to trial-produce EAA products on their EVA units.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)