As March draws to a close, can the polypropylene market reverse its downturn?

1. Supply side: Increased maintenance may alleviate pressure, but the suppression from new capacity expansion still exists

Maintenance concentrated release: In mid-to-late March, domestic petrochemical enterprises enter the peak maintenance period, with an increase in planned maintenance facilities (such as Jiujiang Petrochemical, some production lines of Shanghai Petrochemical, Beihai Refining, etc.). Most of the previously shut-down enterprises do not have plans to resume operations. New capacities, such as the 500,000 tons from Inner Mongolia Baofeng, have not yet been put into full production, and it is expected that the supply of polypropylene will decrease in the late part of the month.

High fluctuation in operating rate: International crude oil prices are declining, oil company profits are recovering, and the operating load rate of oil-based PP is expected to slightly increase.

2, Demand side: slow recovery, orders without growth expectations

Plastic weaving industry: Order changes are not significant, operating rates remain stable, terminal demand is mainly for rigid restocking, and new orders are limited.

Plastic film industry: Orders for films such as CPP and BOPP are average, traditional peak season characteristics have not appeared, the market transactions are light, providing weak support to PP.

Non-woven fabric industry: demand is weak, prices remain stable, and there are no significant signs of recovery in end consumption such as hygiene products.

Daily necessities and injection molding industry: order recovery pace is slow, raw material inventory is being digested, purchasing intentions are cautious.

3, Cost and price: crude oil decline weakens support, spot prices under pressure

Data source: Jinlianchuang

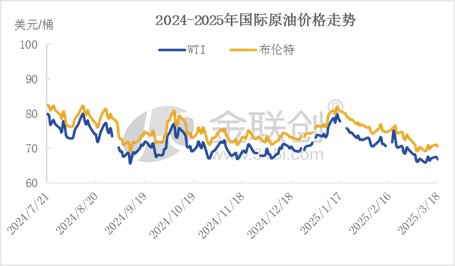

Crude oil prices weaken: International oil prices continue to fall due to the escalation of trade wars and OPEC's increased production, with US oil dropping to around $68 per barrel and Brent to around $71 per barrel, shifting PP production costs downward and weakening price support.

Spot and futures联动压制: Futures market volatility drags down spot prices, lacking momentum for an increase. 注:这里的“联动压制”直译为"联动压制"可能不完全符合英文表达习惯,但根据要求直接翻译。若需更自然的表达,可以调整为"joint suppression"或类似表述,不过这超出了直接翻译的要求。按照指示,保持了原样。

4, Inventory and Sentiment: De-stocking is Expected to Accelerate, but Practitioners Lack Confidence

Petrochemical inventory is neutral to low: As of March 19, the two-oil inventory is 800,000 tons, 35,000 tons lower than the same period last year. Entering the late part of the month, the two-oil companies will start issuing orders for assessment, and it is expected that the inventory reduction will accelerate.

Market expectations are cautious: although increased maintenance provides short-term benefits, the recovery in demand is below expectations. Coupled with the release of new production capacity and low-cost resources, the influx of resources from Shandong Yulong Petrochemical into the North China and East China markets has a significant impact on low-cost resources, leading to insufficient confidence among industry players.

Market forecast, in the short term, due to the continuous decline of polypropylene futures suppressing sentiment, some resources are being sold at a loss, forcing petrochemical companies to lower prices. However, with current prices at low levels and supply-side pressure easing, it is expected that the PP market will consolidate at a low level in the near future, with limited room for further declines. It is predicted that the mainstream price of drawing in East China will fluctuate within the range of 7250-7400 yuan/ton. In the medium term, as petrochemical maintenance becomes more concentrated and downstream demand peaks, this may drive prices to rebound with fluctuations. However, the uncertainty of demand growth may limit the increase in prices.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift