A 12 Billion Yuan Gamble on POE Localization: High-End New Materials Sector Welcomes Another Disruptor

China’s POE sector has finally achieved a major breakthrough! The first phase of Dingjide’s high-end new materials project, with an investment of 12 billion yuan, will officially begin production on September 30. This signifies that the long-monopolized polyolefin elastomer (POE) market, previously dominated by overseas manufacturers, is about to witness another key moment of domestic substitution.

Profit down 20% in the first half-year financial report

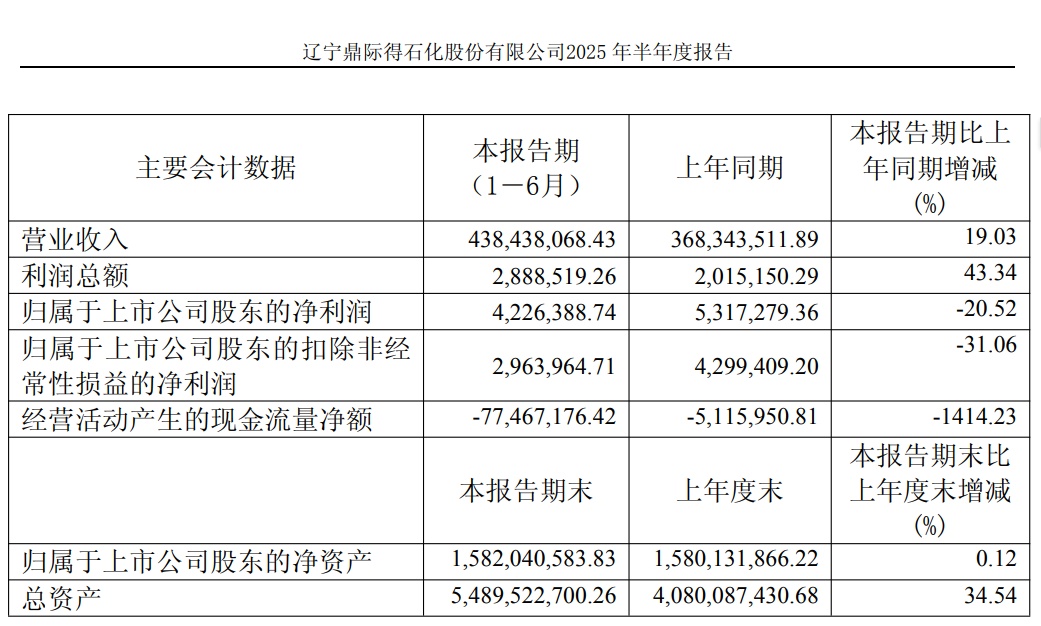

Recently, Dingji De Company announced its semi-annual report for 2025. In the first half of 2025, the company achieved operating revenue of 438 million yuan, a year-on-year increase of 19.03%; net profit attributable to shareholders was 4 million yuan, a year-on-year decrease of 20.52%; and net profit attributable to shareholders after deducting non-recurring gains and losses was 3 million yuan, a year-on-year decrease of 31.06%. In the second quarter of 2025 alone, operating revenue reached 239 million yuan, a year-on-year increase of 28.63% and a quarter-on-quarter increase of 19.71%; net profit attributable to shareholders was 8 million yuan, a year-on-year increase of 583.76% and a quarter-on-quarter increase of 325.40%; net profit attributable to shareholders after deducting non-recurring gains and losses was 8 million yuan, a year-on-year increase of 643.02% and a quarter-on-quarter increase of 255.31%.

In the first half of 2025, facing increased industry competition and the risk of raw material price fluctuations, the company remained steadfast in its strategic goals, deepened industry chain collaboration, and strengthened its customer customization service capabilities, ensuring smooth production and operations. Production and sales volumes remained stable with slight growth, consolidating the company's leading position in the fields of polymer material core additives and catalysts.Key focus areas POE Localization process, optimize POECatalyst system to enhance α-Olefin self-sufficiency rate.

Dingjide Company is one of the few domestic professional suppliers that possess both high-performance polymer material catalysts and chemical additives products. The company's main cooperative clients include state-owned enterprises such as the three major oil companies and Wanhua Chemical, as well as private refining companies like Baofeng Energy. Since 2024, affected by the macroeconomic situation, the chemical industry has been under significant downward pressure, with market demand declining and competition intensifying. The terminal sales prices of the company's products have dropped significantly, while the decrease in procurement prices of production raw materials has been much slower than the decline in terminal sales prices. Market demand has decreased, leading to a reduction in orders and gross profit. Meanwhile, the subsidiary, Petrochemical Technology, is in the project construction phase, resulting in a significant increase in related management expenses. Additionally, the costs of equity incentives are allocated according to regulations. These multiple factors have collectively led to an increase in overall expenses for the company and a narrowing profit margin.

Based on the data, it is evident that Dingjide's revenue and profit in the second quarter have improved quarter-on-quarter, signaling a "turning point" in performance. This indicates that the short-term pressures from previous product price fluctuations and increased project investments have gradually eased, while market attention is more focused on the upcoming POE (polyolefin elastomer) project.

Developing a New Growth Curve—POE

Dingji De Company, with its controlling subsidiary Petrochemical Technology as the main entity, is investing in the construction of a high-end POE new materials project. The project is planned in one phase and implemented in two stages, with a total construction period of 5 years.

The "POE High-end New Materials Project" by Dingjide has passed the investment amount change plan, with the total investment adjusted from the original 10 billion RMB to the current plan of approximately 12 billion RMB. The project is divided into two phases: Phase one primarily involves the construction of a 200,000 tons/year POE joint unit, a 300,000 tons/year α-olefin unit, and a 400 Nm³/h water electrolysis hydrogen production unit; Phase two mainly involves the construction of a 200,000 tons/year POE joint unit and a 250,000 tons/year carbonate unit.

The first phase is expected to be put into production in September, and the second phase is planned to be put into production by the end of 2027. After the project is operational, the estimated annual average revenue will be 11.1 billion yuan, which will effectively address the "bottleneck" issues, fill domestic gaps, and achieve partial import substitution.

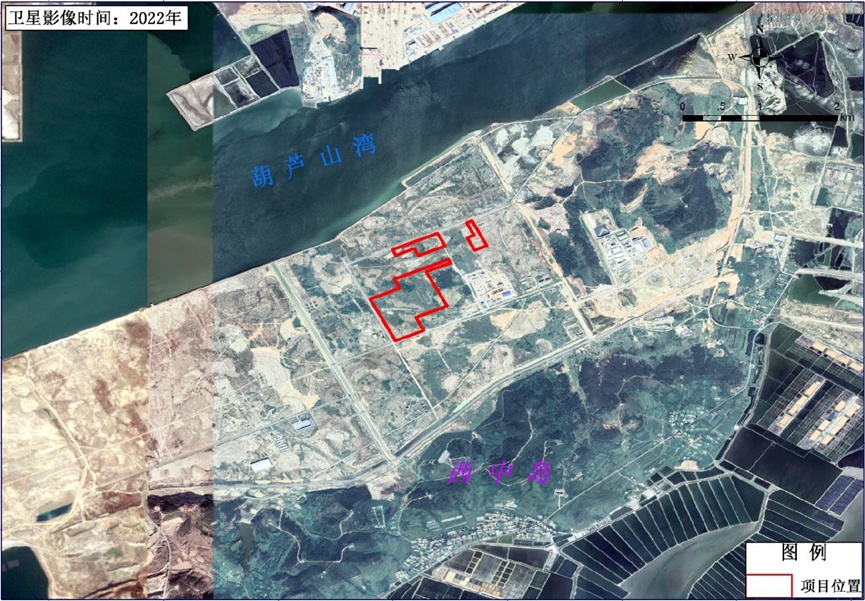

Image: Location of the POE project by Dingjide (Image source: Shuttle Dalian)

Public information shows that POE (polyolefin elastomer) materials combine flexibility and weather resistance, and are widely used in fields such as photovoltaic encapsulant films, automotive interiors, and medical consumables. In 2024, domestic consumption reached 910,000 tons. However, core production capacity has long been monopolized by overseas companies, with the domestic localization rate close to zero, indicating vast potential for import substitution. Since embarking on its POE project, Dingjide has constructed a cost barrier that is difficult for the industry to replicate by achieving full industry chain localization, making it a key factor in breaking the overseas monopoly. In the crucial catalyst segment, its investment is 65% lower than its peers (only 70 million RMB versus the industry’s 200 million RMB); the core raw material, alpha-olefin, is self-produced at half the cost; and in-house production of stabilizers avoids price fluctuations from external purchases. Final calculations show that after depreciation, the unit cost is only 10,000 RMB/ton. If the price of ethylene subsequently drops to 6,600 RMB/ton, the cost could be further reduced to 8,500–9,000 RMB/ton.

In June 2025, the pilot plant for the "High-end New Materials" project of Petrochemical Technology successfully commenced trial production with the joint efforts of the company’s management and all employees, and has produced qualified POE products. The production operation is stable, and the product specifications align with international standards for similar products, laying a solid foundation for the smooth commissioning of the Petrochemical Technology’s "High-end New Materials" project with an annual output of 200,000 tons of POE. The successful start-up of the pilot plant also validated the various indicators of the metallocene catalyst for POE independently developed and produced by Petrochemical Technology, reaching an industry-leading level.

Currently, this cost advantage has translated into landing certainty: according to disclosures, mainstream companies such as Dawn Polymer, Huitong Technology, and Kingfa Sci. & Tech. have reported that product performance meets expectations. Products for the photovoltaic sector have also passed in-depth testing by leading downstream photovoltaic enterprises, with weather resistance and mechanical properties meeting application standards. Framework procurement agreements are gradually being implemented, and order reserves are approaching saturation. According to the plan, the POE production line will officially commence operation in September. Industry analysis believes that the current POE market price is at a historical low. Coupled with the continuous growth in demand from domestic photovoltaic and automotive industries, and considering the projected domestic POE demand of 1.25 million tons by 2025, the logic of “rising volume and price” during the industry recovery period has become clear. Dingji is expected to leverage its cost advantage to quickly capture market share in the domestic substitution process, fully unleashing its performance potential.

Source: Liaoning News

3. POEDomestic production capacity breakthrough

In 2024, the domestic consumption of POE is approximately 910,000 tons, with an import dependency of over 90%, indicating a vast potential for domestic substitution.

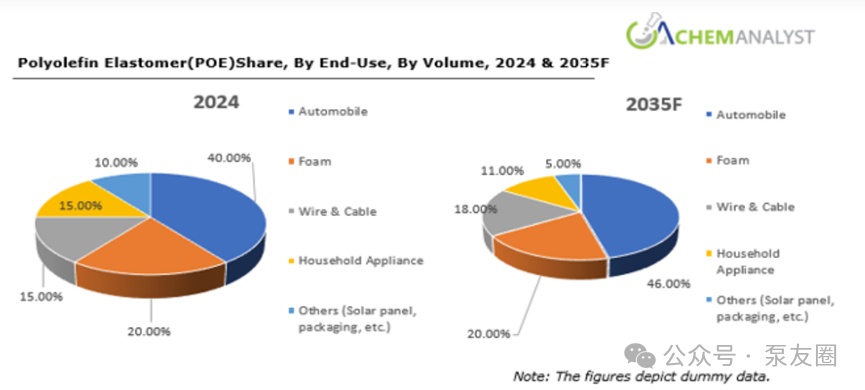

Specifically, global POE consumption is mainly focused on modification, including direct modification, graft modification, and foam modification, and is used in fields such as automobiles, photovoltaics, construction, and home appliances. Among these, the automotive sector accounts for as much as 51% of demand, followed by photovoltaics, construction, and home appliances, which account for 18%, 15%, and 11% respectively. For the automotive sector, downstream customers typically have high requirements for long-term stable supply and product quality consistency. In addition, with the continued rapid growth of global photovoltaic installations and the increasing penetration of POE films, photovoltaics has become the fastest-growing area of demand for POE products.

The future growth drivers of POE mainly come from the surge in photovoltaics, automotive lightweighting, rising demand for healthcare, and trends in sustainable material substitution.

Currently, China has proposed or is constructing approximately 5 million tons of POE production capacity, which will completely change the global supply landscape in the future (Source: Pump Friends Circle).

December 23, 2023BeioyiThe new product launch of Polyolefin Elastomer (POE) has been announced, with the successful commissioning of China's first industrialized POE production unit, independently constructed by Beo Yi Company. This facility is the first in the country to mass-produce polyolefin elastomers (POE) with an annual capacity of 30,000 tons, marking the official start of POE localization. On April 13, 2024, Beo Yi's domestically industrialized photovoltaic-grade polyolefin elastomer (POE) was successfully loaded and dispatched, heading to Changzhou Sveck Photovoltaic New Material Co., Ltd., thereby achieving the first batch sales of photovoltaic-grade products from the country's first industrialized POE unit.

Wanhua ChemicalAround 2016, Wanhua Chemical began the research and development of POE, positioning it as one of its fourth-generation products. The first phase of Wanhua's POE (polyolefin elastomer) project, with an annual capacity of 200,000 tons, is expected to be put into operation in the first half of 2024. The second phase, located at the Penglai site, with an annual capacity of 400,000 tons, is already under construction and is expected to be completed and put into operation by the end of 2025. By then, Wanhua's total POE production capacity will reach 600,000 tons per year.

Maoming PetrochemicalThe 50,000-ton/year POE unit operated steadily in June, with the load increased to 60%. The products are mainly general-purpose grades, filling the gap in the domestic mid-to-low-end market.

Jiangsu HongjingA 100,000-ton POE plant started trial production in June, with 70% of its capacity targeting automotive modified materials (already certified by BYD and CATL) and 30% supplying photovoltaic encapsulant films. It is equipped with a 100,000-ton α-olefin unit to achieve self-sufficiency in raw materials.

4. Opportunities and Challenges Behind the High-End New Materials Sector

Despite a 20.52% year-on-year decline in net profit in the first half of the year, Dingjidede is still pushing forward with its POE (polyolefin elastomer) project, which has a total investment of 12 billion yuan and is about to commence production in its first phase. This strategic choice clearly reflects the structural changes in the current chemical industry: the profits of traditional bulk chemicals continue to decline, and opening up new avenues in high-end new materials has become a necessary option.

Under the wave of domestic substitution, materials such as POE, which have long relied on imports, have become key areas for domestic enterprises to focus on. However, the path for domestically produced POE is not without obstacles. Companies like Dingji and others still face three major practical challenges:

First, technological stability is the core bottleneck for large-scale production. From successful pilot tests to continuous stable mass production, it is still necessary to overcome numerous challenges such as maintaining the activity of metallocene catalysts and ensuring batch consistency of products. This poses extremely high demands on process control and catalyst lifespan.

Secondly, the risk of a counterattack by international giants cannot be ignored. In the past, during the localization process of materials such as MDI and PC, overseas giants have adopted price reduction strategies to squeeze the profit margins of domestic companies. The POE market is still dominated by overseas leaders, and the possibility of a price war is relatively high.

Finally, the downstream certification cycle is long, especially for photovoltaic modules which require 6-12 months, and the automotive sector even needs up to 2 years, resulting in the domestic POE material market penetration being unable to improve rapidly, making it difficult to support performance in the short term.

Despite ongoing challenges, POE, as an indispensable material in the photovoltaic N-type cell and new energy vehicle lightweighting processes, has made a key breakthrough in localization. This high-barrier, high-value track is attracting more and more Chinese companies to heavily invest in the future.

Editor: Lily

Source: China Chemical Industry Park, Changjiang Securities, Pump Friends Circle, Chemical Industry Watch

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)