220 Billion Chemical Giant Forecasts: Chemical Industry Chain Restructuring, Who Will Be the Top Winner?

Due to geopolitical risks, the oil price benchmark has shifted upwards, causing a reshuffle in the chemical industry chain. Who will be the big winner at the front? A leading listed company with a market value of nearly 220 billion yuan has given the answer: coal chemical industry.

“The upward trend in oil prices will further amplify the cost advantage of coal-to-olefins.” At the recently held 2025 Annual and 2026 First-Quarter Earnings Briefing, Liu Yuanguan, Director and President of Baofeng Energy, stated that the company achieved substantial year-on-year and quarter-on-quarter growth in its first-quarter performance, and its second-quarter performance will remain stable with modest growth, albeit subject to fluctuations in product prices.

The company's management also stated that 2026 is expected to be the last year of the peak period for new polyolefin capacity deployment in the domestic market. The polyolefin industry is at an important turning point in the capacity cycle, and geopolitical conflicts have further accelerated this timing. The company's annual target for olefin production and sales is 5.6 million tons.

Oil-coal price spread expands, the year of polyolefin bottoming out and rebound?

At the earnings conference held on the same day, Liu Yuanguan further projected that in 2026, profitability in coal-to-olefins will steadily improve. The polyolefins industry is expected to bottom out and rebound: global polyolefins demand will grow steadily, and with domestic capacity expansion significantly slowing after 2026 and high-cost overseas capacity along with outdated domestic capacity gradually exiting the market, the supply-demand imbalance in polyolefins will markedly improve.

Coal-to-olefins refers to the production of methanol from coal and coke oven gas, followed by the production of polyethylene, polypropylene, EVA, and other products from methanol.

The olefins business is the core pillar of Baofeng Energy, and its production process relies on the coal-to-olefins route. According to the company's 2025 annual report, the revenue from olefins products reached 37.61 billion yuan, accounting for 78.28% of total revenue; coking products and fine chemical products followed, with revenue proportions of 15.60% and 5.66%, respectively.

While the industry's fundamentals are improving, what is the cost difference between different olefin production processes?

The larger the oil-coal price difference, the more significant the cost advantage of coal-to-olefins.

According to Guotou Securities, the obstruction of the Strait of Hormuz has driven oil prices above $100 per barrel. The break-even point for coal-to-olefins is only $45–$50 per barrel, and the widening cost gap has given coal-based chemical industry a cost advantage of over 30% compared to oil-based chemical industry. According to industry insiders, the oil-to-coal price ratio has reached a ten-year high due to the current Middle East conflict.

Regarding international oil prices, executives of Baofeng Energy stated that global crude oil prices are expected to remain volatile overall in 2026. Even if the Middle East conflict ends, oil prices are unlikely to return to normal levels within two months. Moreover, affected by the conflict, overseas countries may increase their oil reserves in the future; therefore, “oil prices at a relatively high level may persist for an extended period.”

In terms of coal prices, it is expected that the operating center in 2026 will slightly decrease compared to 2025. In 2026, China's coal supply and demand will still maintain a relatively loose state. On the demand side, it is mainly affected by the continuous substitution of new energy power generation, with domestic coal demand for thermal power continuing to face pressure; on the supply side, it is expected to remain stable overall under the regulation of national policies.

Choice data shows that the polyolefin price index touched its short-term low in 2022 and again in 2025. The index remained in a downward trend throughout 2025. At the start of 2026, the index was still hovering near the bottom, but it quickly surged to a high level in early March and has since been fluctuating within a range.

Olefin project reaches full production in 2025, with a significant increase in profits in the first quarter.

As of the disclosed first-quarter results on April 23, Baofeng Energy reported dual growth in revenue and net profit. In the first quarter of 2026, the company achieved revenue of RMB 13.237 billion, an increase of 22.90% year-over-year, and attributable net profit of RMB 3.661 billion, up 50.23% year-over-year. Notably, the olefins segment saw its per-ton gross profit rise by RMB 641 compared to the fourth quarter of the previous year.

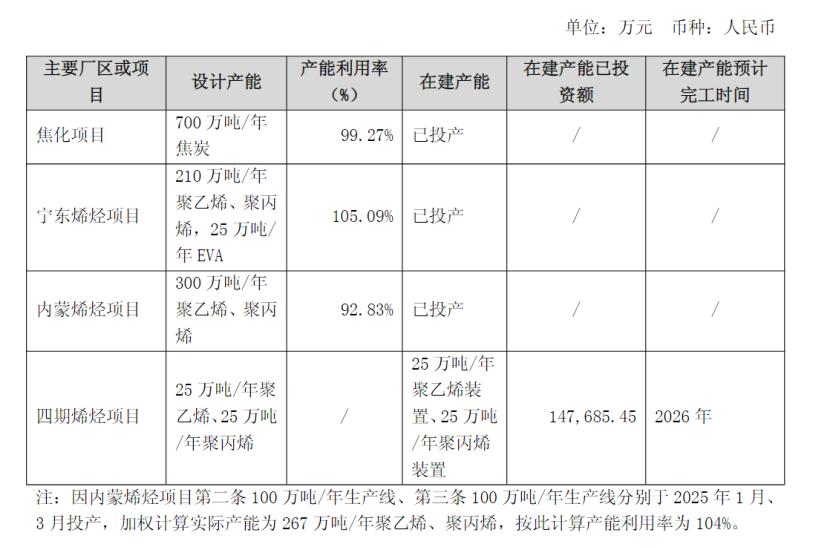

The core driver of revenue growth stems from the progress of new projects: the Inner Mongolia olefins project has reached full production, leading to a year-over-year increase in olefins production and sales volume. Specifically, in 2025,Baofeng EnergyThe Inner Mongolia base's 3-million-ton-per-year coal-to-olefins project—the largest single-site facility of its kind globally—has reached full production capacity. The company's total olefins capacity now stands at 5.2 million tons per year, making it the largest coal-to-olefins producer in China, accounting for approximately 34% of the nation's total coal-to-olefins capacity.

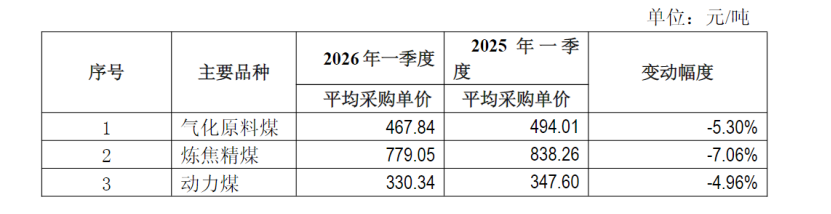

At the same time, Bao Feng Energy further reduced its raw material costs. The company's first-quarter report showed that the procurement costs of the three core raw materials—gasification coal, coking coal, and power coal—were 467.84 yuan/ton, 779.05 yuan/ton, and 330.34 yuan/ton, respectively, each declining by 5.30%, 7.06%, and 4.96% year-over-year. In addition, Bao Feng Energy is a leading company in the coal-based olefins integrated industry, with strong cyclical resistance capabilities.

Bao Feng Energy 2026 First Quarter Report

Recently, the company stated on the interactive platform that in March this year, due to the Middle East geopolitical conflict, the price of international polyolefin market was relatively higher compared to the domestic market, and the company's polyolefin exports in that month increased significantly compared to previous years. The company has obtained the qualification for self-operated import and export, and maintains good cooperation with professional foreign trade institutions. It has now established a relatively complete overseas sales channel and has a group of stable international clients. In the future, the company will continue to focus on the overseas market, steadily expand its international business layout, and dynamically optimize the proportion of domestic and overseas sales according to market conditions.

Regarding the annual target, management plans for the Inner Mongolia project to achieve olefin production and sales of 3.2 million tons, and for the Ningdong project to achieve production and sales of 2.4 million tons. Currently, the company is experiencing robust production and sales, with all production facilities operating stably at high capacity; no major maintenance shutdowns are scheduled for 2026. The selling price of polyolefin products in the second quarter is expected to increase from the first-quarter level.

On April 22, the company stated on the Interactive E platform that "revenue from olefin products" not only refers to polyethylene, polypropylene, and EVA products, but also includes the revenue from by-products, such as propylene, mixed C4, coal-based mixed pentene, sulfur, and olefin liquefied gas.

Baofeng Energy's Production Capacity and Operation Status Source: 2025 Annual Report

Regarding new projects, the company stated that the Ningdong Phase IV olefin project (with an annual capacity of 500,000 tons) is under construction and is scheduled to start production by the end of 2026. The Inner Mongolia Phase II olefin project and the Xinjiang olefin project are currently awaiting approval from the National Development and Reform Commission.

Looking further ahead, where will the core growth come from? Liu Yuanguan responded that first, production capacity will continue to grow. Ongoing and reserved projects are proceeding in an orderly manner, existing production facilities are operating at high load and stable conditions, and the scale effect continues to be released, leading to steady growth in operating performance. Second, product structure will be optimized and upgraded. The proportion of high-value-added products such as photovoltaic-grade EVA and high-end polyolefins will continue to expand, enhancing profitability. Third, green and low-carbon transition will empower the industry. Green hydrogen and green electricity coupling with chemical production are being steadily advanced.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

First Time Surpassing $3 Billion! First Time Surpassing 100,000 Tons! Cathay Biotech’s 2025 Performance: Chemical Production Fully Phased Out, Biological Method Wins

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Completion And Commissioning! Evonik’s Four Major Projects Officially Launched