Us military launches missiles! international crude oil falls over 10% in one week, early june becomes key turning point

This week’s international crude oil market can truly be described as “thrilling.”

The international crude oil market experienced its sharpest swing in sentiment so far this year — from a plunge at the start of the week driven by expectations of peace talks, to a midweek rebound triggered by U.S. airstrikes, and then another sharp sell-off over the weekend as demand concerns weighed on prices. Brent fluctuated violently in the $92–$100 range throughout the week. Its settlement price on May 29 was $92.05 per barrel, down 11.1% from last Friday’s $103.54. WTI closed at $87.36 per barrel, down 9.6% for the week. Oman crude oil futures tumbled 5.96% to $97.32, while Murban crude fell to $92.35. The market’s central contradiction has shifted from “whether an agreement can be reached” to “demand destruction amid an armed standoff” — with Cushing inventories falling below the psychologically important 20 million-barrel mark while signs of weak global demand emerged at the same time, bulls and bears are locked in an intense battle at extreme levels. Traffic through the Strait of Hormuz has fallen to 21 vessels per day, with about 1,550 ships trapped in the Persian Gulf. The end-of-month Islamabad negotiation window has passed, and whether a breakthrough can be achieved in early June has become the most critical variable determining the direction of oil prices this summer.

On May 30 local time, U.S. Central Command issued a statement saying that on May 29, U.S. forces struck a Gambia-flagged vessel attempting to sail to an Iranian port while carrying out blockade measures in the Gulf of Oman.

The statement said that the US military detected the cargo ship "Lian Star" in international waters heading towards an Iranian port along the Gulf of Oman. The US military subsequently issued more than 20 warnings to the vessel, informing it that this action was in violation of the US blockade order. After the crew failed to comply with the instructions, a US military aircraft launched a Hellfire missile at the ship's engine room, causing the vessel to stop heading towards Iran.

The U.S. Central Command said that, while the ceasefire with Iran remains in effect, U.S. forces have struck five commercial vessels and redirected 116 ships to fully enforce the blockade measures.

As of May 31, 2026, international crude oil prices have retreated sharply from elevated levels, with the geopolitical risk premium having contracted significantly. Expectations of weak global demand are dominating the short-term market, and domestic crude oil futures have weakened in tandem. The expected sharp cut in refined oil product prices on June 4 has materialized. The market’s key points of contention are currently centered on progress in U.S.-Iran negotiations, U.S. crude inventories, OPEC+ production cut compliance, and Federal Reserve monetary policy. In the short term, oil prices are likely to remain weak and range-bound, while the medium- to long-term tight balance between supply and demand continues to provide underlying support.

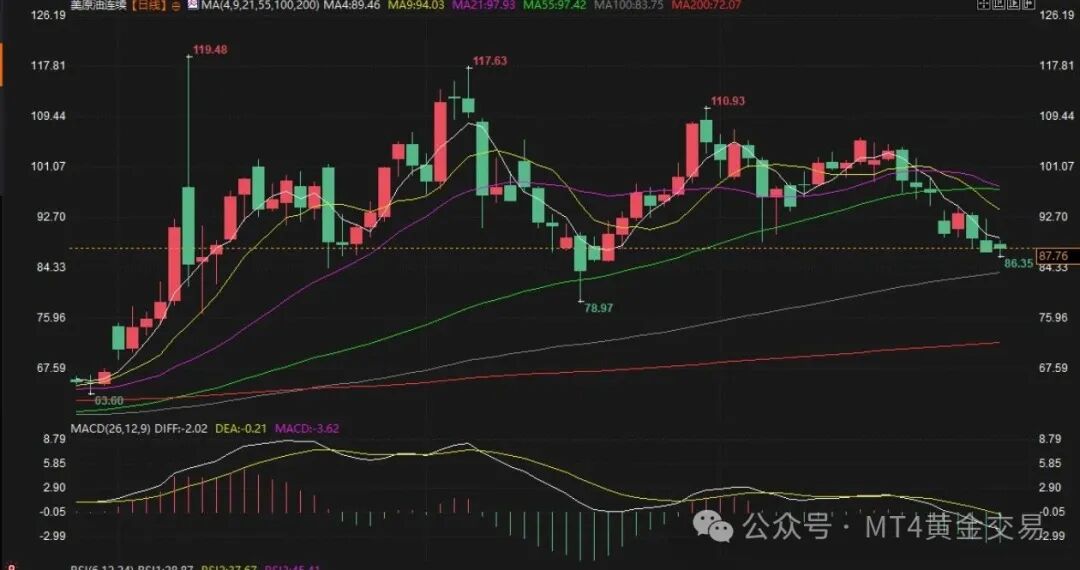

Real-time crude oil prices

International Market: The WTI New York crude oil July contract closed at $86.08 per barrel, plunging 1.72% in a single day and down 9.1% for the week. The Brent crude oil July contract closed at $89.51 per barrel, down 1.35% on the day. Overall, in May, it has fallen nearly $20 from its high of $112, as the previous geopolitical speculation bubble continues to be unwound.

Domestic market: The Shanghai crude oil SC main contract 2607 closed at 579.8 yuan/barrel, down 1.61% for the day. The domestic market followed the weak trend of the international market. Refinery crude oil purchase prices were simultaneously adjusted down to 575-583 yuan/barrel. Downstream refineries remain cautious, replenishing stocks in small quantities as needed, with no large-scale inventory build-up.

Supply-demand fundamentals: Supply constraints persist, while demand shows signs of weakening.

On the supply side, OPEC+ continues its deep production cut policy, with total output in April at 33.19 million barrels per day, a month-on-month decrease of 1.74 million barrels per day. Saudi Arabia's crude oil production has dropped to its lowest level in nearly 30 years. The global voluntary production cut capacity exceeds 10 million barrels per day. Navigation through the Strait of Hormuz has slightly resumed, easing market fears of disruptions in crude oil transportation and directly eliminating a large amount of risk premium. U.S. shale oil production continues to recover, with the latest weekly output stable at 13.7 million barrels per day, slightly offsetting the OPEC+ production cut gap.

On the demand side, the downturn in manufacturing activity in Europe and the United States has weakened industrial crude oil consumption; the operating rate of domestic independent refineries has continued to decline to 52.5%, and demand for petrochemical feedstocks has contracted. Although the summer gasoline consumption peak is approaching, near-term weak demand expectations are limiting the upside in oil prices, and the IEA has lowered its forecast for global crude oil demand growth in 2026.

Market Trend Analysis: Short-term Weakness Seeking a Bottom, Mid-to-Long Term Base Remains Stable

Short-term trend: The US-Iran talks have released signals of easing tensions, coupled with a concentration of profit-taking by bulls, leading oil prices into a rapid correction phase. The short-term key support for WTI is $83/barrel, with resistance at $91/barrel; for Brent, support is at $86/barrel, with resistance at $95/barrel; the domestic SC main support is at 568 yuan/barrel, with limited rebound potential in the short term, likely maintaining low-level oscillation and consolidation.

Medium- to long-term outlook: OPEC+’s continued production cuts, combined with ongoing global crude oil inventory drawdowns, have led to a cumulative reduction of 246 million barrels in global visible inventories in March–April. Low inventory levels will provide strong downside support. With the summer travel peak approaching, gasoline demand is expected to rebound. This round of declines is a pullback driven by geopolitical sentiment, and the medium- to long-term upward logic has not been fundamentally undermined.

Core Reference Data Most Concerned by Investors (Updated on May 31)

EIA U.S. crude oil inventories (core monitoring indicator): For the week of May 15, inventories fell by 7.863 million barrels, marking six consecutive weeks of draws. U.S. commercial crude oil stocks have reached a five-year low for this time of year, which is the strongest support for the medium- to long-term bottom of oil prices.

2. Refined oil price adjustment outlook for this round: The pricing adjustment window will open at 24:00 on June 4. Based on current estimates, prices are expected to be cut by 510 yuan/ton, equivalent to a decrease of 0.39 yuan per liter for 92-octane gasoline, marking the second sharp decline this year.

3. U.S. Dollar Index: The latest quote is 100.26. The U.S. dollar has strengthened slightly, continuously weighing on commodity valuations and limiting the upside potential for crude oil.

4. OPEC+ total production in April: 33.19 million barrels per day, down 1.74 million barrels per day month-on-month; voluntary production cuts remain at high levels, locking in a future supply shortfall.

U.S. shale oil weekly production: 13.7 million barrels per day, reaching a new high for the year, temporarily easing the global supply tightness.

Freight and Discounts: Middle East routes under pressure, West Africa and Brazil freight rates surge, discounts for inferior oil widen.

This week, the global crude oil seaborne transport market has shown an extreme divergence, with the Middle East cooling while the Atlantic is heating up.

Freight rates for VLCC routes from the Middle East to Asia remained at a high level of $3.8 million per vessel at the beginning of the week, before dropping to $3.2 million by the weekend, a decline of 16%. Suezmax tanker rates from the Middle East to Europe fell from $2.8 million to $2.4 million. The main reason for the decline in freight rates is that Asian refineries, faced with feedstock shortages and shrinking margins, were forced to cut orders—China's crude oil imports from Saudi Arabia in June are expected to be only 600,000 barrels per day, about half of April's volume. However, this “decline” is only relative to the previous extreme highs; $3.2 million is still about four times higher than the normal pre-war level. The discount of Middle Eastern Dubai crude to Brent widened significantly from -$2.0 to -$5.5 per barrel, which is the most direct reflection of Middle Eastern crude being stranded at the straits—there is a value gap of more than $5 per barrel between inside and outside the Persian Gulf.

VLCC freight rates from West Africa to Asia have surged against the trend, with the Angola-to-Ningbo, China route rising from USD 1.8 million to USD 2.2 million, up 22%. Freight rates from Nigeria to Sikka, India have climbed in tandem. The discount of West African Angolan crude to Brent has widened from +USD 1.0 to +USD 3.2, and the discount of Nigerian Bonny Light has widened from +USD 1.5 to +USD 3.8. Asian buyers are shifting procurement toward the Atlantic Basin at any cost, a clear signal of a structural reshaping of global crude oil trade flows.

VLCC freight from Brazil to Asia rose from $2.00 million to $2.35 million, an increase of 17.5%. Brazilian Tupi crude's premium to Brent rose from +$1.8 to +$3.5. Brazil's national oil company has announced it will increase export allocations to Asia in June. Among South American sour crudes, Venezuela's Merey crude's discount to Brent widened from -$8.0 to -$11.0, and Ecuador's Napo crude's discount widened from -$3.0 to -$5.5.

The main reason for the widening discount of low-quality crude oil is that refinery margins have been squeezed by high oil prices, prompting refineries to prioritize the purchase of high-grade crude to increase yields. In addition, as refineries around the world enter maintenance season, demand for high-sulfur heavy crude has dropped to rock bottom. However, this widening discount is beginning to attract some independent refineries to buy at low prices. If the discount further widens to -$15, it will trigger a rebound in bargain-hunting demand.

The simultaneous appearance of a $-5.5 Middle East discount and a $+3.8 West Africa premium is the best illustration of a "logistics breakdown" in the global crude oil market. Next week, pay attention to whether West African freight rates will exceed $2.5 million, and whether a Venezuelan discount expanding to -$15 will trigger bargain-hunting by Asian refineries.

In the short term, the crude oil market remains weak and seeks a bottom due to the triple negative impact of easing geopolitical tensions, a stronger US dollar, and profit-taking by long positions; there is insufficient momentum for a rebound. In the medium to long term, however, with deep production cuts by OPEC+, persistently low global crude inventories, and the peak summer gasoline consumption season, the downside for oil prices is limited and there is strong support at the bottom. From a trading perspective, it is advised to mainly stay on the sidelines in the short term and wait for signs of price stabilization. Industrial clients may consider locking in raw material procurement costs in batches during price pullbacks.

The commander of the Iranian Revolutionary Guard Corps declared "We have blocked it," setting control over the Strait as a red line. The probability of "limited progress but delayed signing" has risen to 45%, becoming the primary baseline scenario. Quantitative models show the fair value of Brent crude to be around $100 per barrel, higher than the market price. Early June is a critical window for determining the direction of summer oil prices—if an agreement is reached, Brent is expected to fall back to $85 to $92, with Middle Eastern premiums narrowing significantly first; if the deal breaks down combined with military tensions, Brent could break through $110 and rise to $120 to $130.

Focus on three key signals next week: whether the EIA inventory on June 4th continues to deteriorate, whether the number of vessels passing through the strait drops below 20, and whether Gulf mediation produces a new proposal. The storm is not over yet; the crossroads of agreement and war are now clearly ahead.

The article is compiled from publicly available information on the internet, including sources such as Zhuan Su Vision, Securities Times, Earth Collector, Miao Dong Today's Crude Oil, and MT4 Gold Trading.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Eastman France PET Depolymerization Plant: Project "Alive," But Construction Paused

-

Mitsubishi Chemical Plans To Split Petrochemical Business By 2028

-

Bola Carbon Black Announces Global Restructuring of Specialty Carbon Black and Multi-Walled Carbon Nanotube Business

-

900,000-Ton-Per-Year Ethylene Plant Shut Down! ExxonMobil Reshapes Asia-Pacific Petrochemical Landscape