Urgent Warning! New Round of Surge in Plastic Chemicals Imminent! Houthi Forces Block Red Sea, April Price Hike Notifications En Route!

Introduction: As missiles launched by Yemen’s Houthi armed group head toward Israel, global chemical markets grow increasingly nervous—this is not merely another escalation in geopolitical tensions, but rather an “energy stranglehold” stretching from the Persian Gulf to the Red Sea, tightening its grip on every link in the industrial chain, from crude oil to plastics.

On March 28 local time, Yemen's Houthi armed group formally declared war on Israel, launching ballistic missiles for the first time against targets in southern Israel, and stated that "operations will continue until Israel's aggression ceases." On the same day, the Israel Defense Forces carried out a new large-scale airstrike on Tehran, Iran's capital, claiming they had nearly destroyed approximately 90% of Iran's critical military-industrial facilities.

The war, far away in the Middle East, is spreading at an astonishing speed to China's factory raw material warehouses, European chemical production facilities, and the price tags of plastic products around the globe.

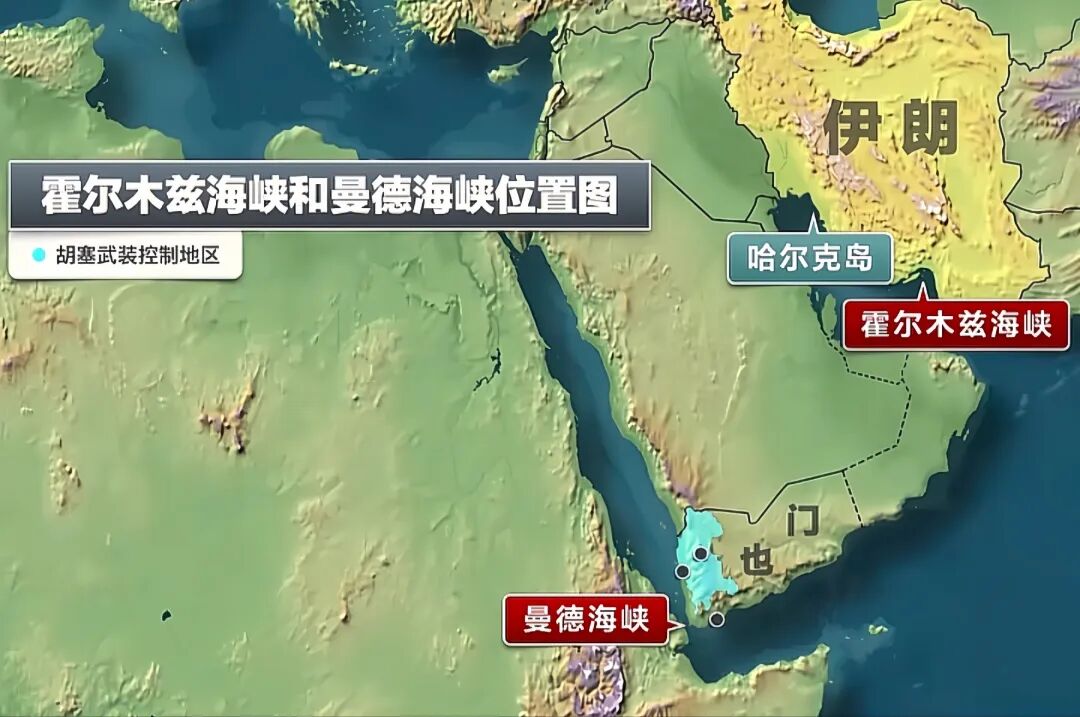

I. Dual Throats: The “Deadly Linkage” of the Strait of Hormuz and the Bab el-Mandeb Strait

The most dangerous consequence of the Houthis' involvement in the war is not the missiles themselves, but their ability to strangle global energy lifelines.

The Strait of Mandeb, a narrow waterway connecting the Red Sea to the Indian Ocean, is only 29 kilometers wide at its narrowest point, and carries daily traffic.Over 4.2 million barrelsIts oil transportation volume accounts for more than 5% of global seaborne oil trade and serves as the sole route for Persian Gulf crude oil bound for Europe and North America via the Suez Canal. Approximately 12% of global trade transportation—and a nearly equivalent proportion of seaborne oil trade—must pass through this waterway.

At this moment, this passage is forming a lethal linkage with the Strait of Hormuz, which has already been “de facto closed.” Since the U.S. and Israel launched military strikes against Iran on February 28, the Strait of Hormuz—the waterway handling approximately30% oil transportationThe crucial throat passage has been effectively closed for a full month.

This means that the sea crude oil export routes of core oil-producing countries such as Saudi Arabia, Iraq, Kuwait, and the UAE are facing a "double chokehold" from both the east and the west. According to calculations, if both routes were to be paralyzed simultaneously, the world would see a daily loss ofMore than 24 million barrelsThe disruption of oil transportation, which accounts for nearly a quarter of global oil trade.

II. From Crude Oil to Plastic: The “Domino Effect” Along the Industrial Chain

For the chemical industry, the impact of this crisis goes far beyond oil prices alone. The Middle East serves as the world's "breadbasket" for chemical feedstocks, accounting for more than 30% of global chemical production capacity. When feedstock supplies are cut off, the entire supply chain begins to collapse step by step.

The first domino falling: Methanol and olefins.SABIC has officially announced that its Ar-Razi plant located in Jubail will5 million tons per yearMethanol production capacity has been hit by force majeure, leading to a complete shutdown. According to the latest report from Morgan Stanley, similar force majeure declarations have spread to 10 countries globally, with over 31 declarations issued, covering core chemicals such as ethylene, propylene, and polyethylene.

The second domino: A wave of shutdowns at Asian chemical plants.Japan's February ethylene production plummeted 23% from the previous month, hitting a record low of 334,200 tons, with naphtha cracker operating rates dropping to 75.7%, the lowest level since June last year. South Korea's largest petrochemical company, LG Chem, has decided to shut down its No. 2 plant (with an annual capacity of 800,000 tons) at its core Yeosu site due to a prolonged disruption in naphtha supply. In Morbi, Gujarat, India, a well-known tile production area, nearly 450 out of 670 tile factories have suspended operations.

The Third Domino: Price Shock to European Industrial Chains.European PX (paraxylene) contract prices are expected to rise sharply, with Chinese PX price ranges already increased by USD 328/ton. Poland's Orlen has reduced PTA operating rates due to a force majeure event at its PET plant.

III. In-Depth Forecast of Plastic Market Trends: Projection of Price Movements for the Next Three Months

The current Middle East situation has escalated from “conflict risk” to a substantive supply disruption, placing the plastics market at the starting point of a new upward price cycle. Below is a commodity-by-commodity forecast for major plastic types.

(1) Polypropylene (PP): Cost-driven price increase, with upside potential of 10%–15%

PP is highly sensitive to crude oil prices; for every $10 increase per barrel of crude oil, PP production costs rise by approximately RMB 800–1,000 per ton. If Brent crude oil reaches $130 per barrel, as forecast by Citigroup, the theoretical cost of PP would rise to the range of RMB 9,500–10,000 per ton.

Supply SideThe Middle East accounts for approximately 25% of global PP capacity, and several PP production units in Saudi Arabia have announced reduced operating rates due to feedstock shortages. Domestically, PP social inventory in March has dropped to 85% of the level seen during the same period last year, and port arrivals of imported PP cargoes have decreased by more than 20% month-over-month. With the Red Sea route disrupted, shipping transit time for PP from the Middle East to Asia will extend from 20 days to 40–50 days (requiring a detour around the Cape of Good Hope), leading to a sharp decline in import arrivals in April and May.

Demand sideApril is the traditional peak season for demand of conventional film and packaging film, with strong willingness of downstream industries to purchase on a regular basis. However, it is necessary to be alert to the negative feedback of high prices on demand. If PP price rapidly exceeds 9,500 yuan/ton, some low-margin processing enterprises may choose to reduce production and wait.

Price PredictionPP prices are expected to fluctuate and rise slightly within the range of 8,800-9,200 yuan/ton in early April. By late April to May, prices may break through 9,500 yuan/ton, representing an increase of approximately 10%-15% compared to the end of March. It is recommended that downstream companies take the opportunity to stock up appropriately during early April, locking in part of their raw material costs.

(II) Polyethylene (PE): High import dependency; price increase may exceed that of polypropylene (PP).

PE (including LLDPE, LDPE, and HDPE) is one of the general-purpose plastics with the highest import dependency in China, with an import dependency rate of approximately 35% in 2024, of which over 50% comes from the Middle East region (Saudi Arabia, UAE, Iran).

supply shockThe Red Sea-Suez route is the main channel for Middle Eastern PE to be exported to Europe and Asia. After the Houthis blockaded the Strait of Bab el Mandeb, exports of Middle Eastern PE will face the problem of "being unable to leave." Currently, some traders have reported that several PE producers in Saudi Arabia have suspended quotes for April shipments, waiting for the situation to clarify. According to data from L&F Information, as of March 28, the PE port inventory in the East China region has decreased by 12% from the beginning of the month, and the arrival forecast has continued to decline for three consecutive weeks.

Structural differences:

LLDPE(Linear low-density polyethylene, mainly used for films): Supported by agricultural film demand, it has the highest price elasticity, with an expected increase of 12%-18%.

LDPE(High-pressure polyethylene, mainly used for heavy packaging film, cable material): Supply is relatively tight, with possible price increases leading, expected to be 15%-20%.

HDPE(High-density polyethylene, mainly used for pipes and hollow containers): Driven by infrastructure demand, the increase is relatively moderate, with an expected rise of 8%-12%.

Price PredictionThe target price for the LLDPE main contract in April is expected to be in the range of 9,500-9,800 yuan/ton, and LDPE is expected to break through the 11,000 yuan/ton mark. It is recommended that packaging film and agricultural film enterprises complete at least one month's worth of raw material stockpiling by early April.

(3) Polyvinyl chloride (PVC): Coal chemical advantages become prominent, with a relatively independent trend.

PVC is a type of plastic relatively less affected by crude oil prices, as approximately 80% of China’s PVC production capacity employs the calcium carbide process (a coal-chemical route) rather than oil-based feedstocks. In this round of the Middle East crisis, PVC may serve as a “safe-haven” commodity.

Cost sideAlthough the rise in crude oil prices will pass on some pressure via the ethylene method PVC (about 20% of capacity), under the background of stable coal prices, the cost advantage of the calcium carbide method PVC will become more prominent. Currently, the complete cost of calcium carbide method PVC in the northwest region is about 5,600-5,800 yuan/ton, far below the cost line of over 7,000 yuan/ton for the ethylene method.

Supply and Demand SideDomestic PVC social inventory is at a historically high level for the same period (approximately 550,000 metric tons), indicating relatively ample supply. On the demand side, the slowdown in real estate completions has dampened demand for pipes and profiles, but export demand—particularly to India and Southeast Asia—has remained strong. PVC export bookings in March rose 25% month-over-month, driven by front-loaded exports ahead of India's anti-dumping policy window.

Price ForecastPVC prices will show a fluctuating pattern with cost support at the bottom and demand pressure at the top, with an expected range of 6,200-6,800 yuan/ton in April-May, representing an increase of about 5%-8% from the end of March. Compared to PP and PE, the rise in PVC is relatively moderate, but it has a good safety margin. It is recommended that pipe and profile enterprises purchase in batches at low points.

(IV) Engineering Plastics (e.g., ABS, PC): Passive Price Increases Under Dual Pressure

Engineering plastics such as ABS (Acrylonitrile-Butadiene-Styrene copolymer) and PC (Polycarbonate) are facing a dual squeeze of "rising raw material costs + weak terminal demand."

Raw Material EndThe three main raw materials for ABS—styrene monomer (SM), butadiene (BD), and acrylonitrile (AN)—are all affected by rising crude oil prices. Among them, styrene has the highest correlation with crude oil, with its price increasing by over 12% in March. The primary raw material for PC, bisphenol A (BPA), is also facing cost-driven pressure.

Demand SideDemand recovery in end-use sectors such as home appliances, automotive, and electronics has fallen short of expectations, limiting their willingness to accept higher-priced engineering plastics. This could make it difficult for engineering plastic price increases to fully offset rising costs, thereby squeezing producers' profit margins.

Price PredictionABS is expected to rise by 8%-10%, with the main price range moving up to 12,500-13,500 yuan/ton; PC is expected to rise by 6%-8%, with the main price range moving up to 15,500-17,000 yuan/ton. It is suggested that downstream product enterprises follow the principle of "procuring as needed and shortening the inventory cycle" to avoid stocking up in large quantities at high prices.

(5) Short-term Risks and Mid-term Turning Points

Upward risk:

If the Strait of Hormuz is subjected to a military strike, oil prices could instantly surge above $150 per barrel, causing plastic prices to jump accordingly.

Major chemical plants in the Middle East have been forced to suspend operations due to raw material shortages or safety concerns, leading to an expansion of the supply gap.

Downside risk:

If the U.S. and Iran reach a temporary ceasefire agreement through a third party, market risk-off sentiment could ease, potentially leading to a 5%-8% correction in plastic prices.

Domestic demand recovery has fallen short of expectations, and downstream enterprises are unable to bear the high prices of raw materials, resulting in a situation of “high prices but no market.”

Mid-term inflection point signal:

The current plastic price rally is expected to last until mid-to-late June. Pay close attention to the following turning-point signals:

Has the Strait of Hormuz resumed navigation?

Has Saudi Arabia and Iran initiated formal talks?

Whether the domestic social inventory has risen for three consecutive weeks

Has downstream operating rates fallen below the 60% breakeven point?

IV. From Panic to Calm: Traders’ Rollercoaster of Emotions

Shao Shiping, Vice Chairwoman of Zhejiang Mingri Holding Group, described the shift in market sentiment during this price movement in three stages: "When the conflict first emerged, everyone feared a 'black swan' event, and the entire team was on high alert, focused on risk mitigation. Within just a few days, upstream suppliers issued force majeure notices, prompting everyone to calmly assess their positions and systematically review order risks. Now, as the market enters a state of high volatility and low liquidity, we've actually become more composed—neither rushing to buy nor hastily offloading inventory."

This shift in mindset reflects profound changes in the chemical trading industry. Chen Tao, General Manager of Guomao Chemical, who has 25 years of experience in the field, keenly observed that this crisis is fundamentally different from previous ones—during the Russia-Ukraine conflict in 2022, market anxiety was largely driven by fear of supply shortages and anticipatory panic; this time, however, it isPhysical supply chain is cut offThe obstruction of the Strait of Hormuz directly cuts off the core logistics channel for global energy and chemical industries.

"In today's market, everyone is both fearful and eager to profit, causing trading cycles to shorten significantly—no one dares to sign long-term contracts; everyone is doing short-term and spot deals," said Hao Xiaoyu, Director of Chemical Research at Zhongji Group.

V. The Perils and Opportunities for Domestic Enterprises: The Unexpected Dividend of Coal Chemical Industry

In this storm, Chinese energy and chemical companies are facing unprecedented challenges and opportunities.

10 million barrelsThe crude oil production has been shut down, and restoring this supply will take weeks or even months. China's import of methanol from the Middle East accounts for about 30%-35% of the domestic trade volume, and port inventories remain at low levels for this period.

PVC EnterpriseThe cost advantage of the calcium carbide route is becoming increasingly prominent, and integrated enterprises such as Xinjiang Tianye and Zhongtai Chemical are expected to see their gross profit per ton widen to RMB 800–1,000.

Coal-to-olefins enterpriseThe cost advantage of coal-based routes, such as Baofeng Energy and Donghua Energy, over oil-based routes will expand from 500 yuan/ton to over 1500 yuan/ton.

Modified Plastic EnterpriseLeading enterprises with formulation adjustment capabilities, such as Kingfa Science & Technology and Polytech, can alleviate raw material pressure through alternative solutions, thereby potentially increasing their market share.

Meanwhile, domestic leaders with integrated upstream and downstream operations are expected to accelerate their market share growth against the backdrop of capacity clearance in Japan and South Korea and cash flow pressures on smaller peers.

VI. Operational Recommendations for Plastic Products Enterprises

Based on the current situation and price forecasts, the following operational recommendations are proposed for plastic product enterprises of different types.

Picking strategy

Packaging film and agricultural film enterprises (mainly PE/PP)It is recommended to complete the two-month raw material stockpiling by April 10, to lock in the costs.

PVC-based pipe and profile manufacturersAdopt a "small volume, high frequency" procurement strategy, and actively stock up when the price is below 6200 yuan/ton.

Home appliance and automotive parts companies (mainly ABS/PC)It is recommended to sign a quarterly price-lock contract with upstream suppliers to mitigate short-term price fluctuations.

2. Product structure adjustment

Moderately increase the addition ratio of recycled material (under the premise of ensuring quality)

Develop alternative raw material solutions, such as using PVC to replace part of ABS in non-critical components.

Establish a price linkage mechanism with downstream customers and shorten the validity period of quotations

3. Risk hedging

Using futures tools for hedging, focusing on the main contracts of LLDPE, PP, and PVC

Focus on the impact of RMB exchange rate fluctuations on the cost of imported raw materials.

And with the Houthi forces officially entering the war and the threat of a blockade on the Bab-el-Mandeb Strait, the fuse for a new round of price hikes has been lit.

Citigroup analysts warned that if energy infrastructure were subjected to widespread attacks, and the Strait of Hormuz remained closed for an extended period, the average price of Brent crude oil could reach $X per barrel in the second and third quarters.$130Previously, Iran’s claim of “oil priced at $200 per barrel” was not mere fantasy. Once oil prices breach this threshold, cost pass-through to plastic raw materials will be inevitable. Calculations indicate that for every $10/barrel increase in crude oil prices, the per-ton production cost of polypropylene (PP) and polyethylene (PE) will rise by approximately $90 and $100, respectively—equivalent to RMB 650–720.

For plastic product companies, this is undoubtedly a harsh spring. From mineral water bottles to car bumpers, from packaging films to electronic product casings, every plastic product is the result of the complex confrontation between the Middle East war and the global supply chain.

A new round of price hikes is imminent.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Global Supply Chain Under Pressure! Wacker Increases Prices for Polymers and Silicones

-

SABIC Declares Force Majeure on Styrene Monomer and Methanol Production; Middle East Chemical Operations Halted

-

Middle East Triggers Widespread Force Majeure In Global Chemical Industry