Two major consumable categories, large-scale centralized procurement to commence

A new round of centralized procurement is about to begin, and the orthopaedic trauma and anti-adhesion materials sectors are once again at a turning point for reshaping.

01

Orthopedic trauma faces a new round of centralized procurement.

The pricing system is becoming stable.

Recently, the Tianjin Municipal Medicine Procurement Center issued the “Notice on Carrying Out Centralized Maintenance of Product Information for Anti-Adhesion Materials and Orthopedic Trauma Medical Consumables” (hereinafter referred to as the “Notice”).

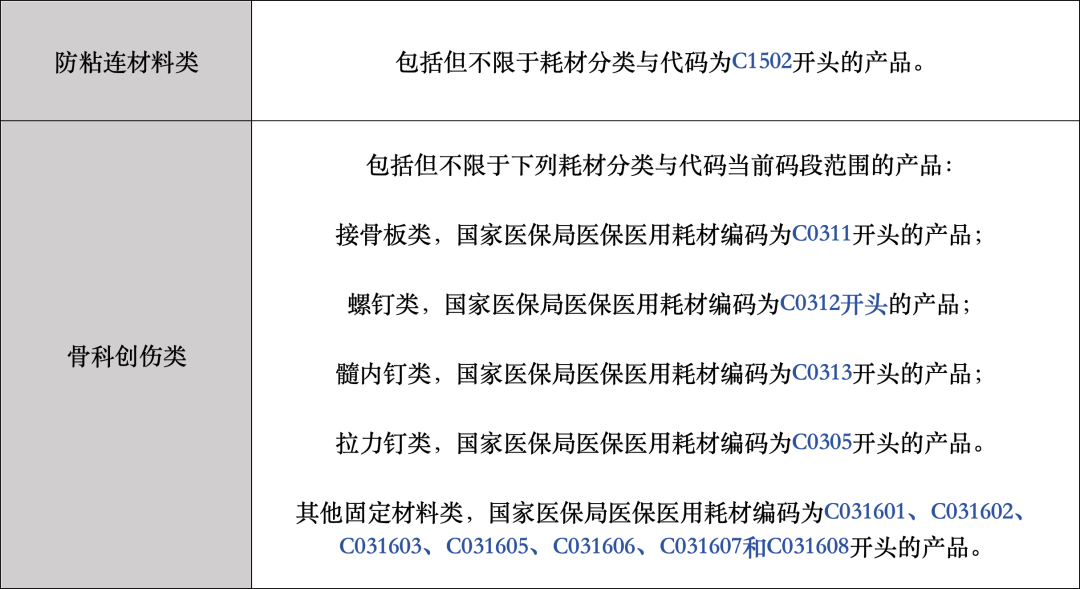

According to the Notice, the centralized maintenance period will run from May 26 to 17:00 on June 8, and the product scope includes two major categories: anti-adhesion materials and orthopedic trauma products, as follows:

Among them, orthopedic trauma consumables fall within the scope of continued procurement.

In 2023, the "3+N" alliance of the Beijing-Tianjin-Hebei region, along with alliances from twelve provinces including Henan, launched a large-scale centralized bulk procurement of orthopedic trauma consumables covering 28 provinces across the country. The procurement volume in the first year exceeded 1.41 million items, with an average price reduction of 80.7%.

As one of the most thoroughly centralized-procurement categories in China, orthopedic consumables have already undergone multiple rounds of reform, including national centralized procurement and interprovincial alliance procurement. As a result, the pricing premium in these products has been largely squeezed out. As previously pointed out by Open Source Securities, as the trend of orthopedic centralized procurement gradually eases at the margin, the likelihood of further significant price cuts is low.

Although the procurement documents have not yet been disclosed, amid the anti-involution trend in volume-based procurement, prices in several recent rounds of new and centralized procurement for major categories have remained relatively stable, with some cases even seeing price increases. Take orthopedic trauma products as an example: in the 2024 Shanghai orthopedic trauma procurement, the maximum winning bid price set was higher than that in the procurement organized by the 28-province alliance.

As pressures such as price cuts and inventory digestion have gradually been alleviated, the orthopedic industry has shown a clear recovery trend. Judging from the latest financial reports, the performance of leading domestic orthopedic companies has generally improved. In 2025, Chunli Medical, Sanyou Medical, Weigao Orthopedic, and Dabo Medical all achieved double growth in revenue, and in the first quarter of 2026, they all maintained stable and progressive development.

For the orthopedic sector, large-scale centralized procurement is no longer the “Sword of Damocles” hanging overhead. With the pricing cycle now largely stabilized, the focus of competition is shifting more toward new battlegrounds such as technological iteration and overseas expansion.

02

首度入局联盟集采

The anti-adhesion materials sector is facing new variables.

Unlike orthopedics, which has undergone multiple rounds of large-scale volume-based procurement, anti-adhesion materials have previously only been included in small-scale procurements in provinces such as Henan, Yunnan, and Jiangxi. This marks the first time these products have entered the scope of large-scale alliance procurement, signaling the beginning of a major price restructuring for this category.

Anti-adhesion materials are a class of medical materials used to prevent abnormal postoperative adhesions between tissues. They primarily work through physical isolation or biological modulation mechanisms to prevent the formation of fibrous adhesions during wound healing, thereby reducing the risk of postoperative complications.

Although not widely known, anti-adhesion materials have seen steadily growing indispensable demand in departments such as general surgery and obstetrics and gynecology, and have now become a standard niche market with strong appeal. According to statistics and forecasts by Biaodian Medicine, the market size of surgical anti-adhesion products in China reached approximately RMB 2.755 billion in 2024 and is expected to increase to RMB 2.998 billion by 2029, with a compound annual growth rate of about 1.71% from 2024 to 2029.

In the 2021 public alliance centralized procurement in Henan, the anti-adhesion materials purchased included anti-adhesion gel, anti-adhesion liquid, and anti-adhesion film, with an average price reduction of 72.21% and a maximum reduction of 76.11%.

According to the latest notice, the scope of products covered under the volume-based linkage procurement for anti-adhesion medical consumables shall be subject to the official procurement documents, which means that the specific procured products have not yet been specified.

Industry insiders have indicated that, based on past experience, the categories included in this round of centralized procurement for anti-adhesion materials will likely still focus on liquids, gels, and films, though the possibility of adding new categories such as semi-solid gels cannot be ruled out.

On pricing, as anti-adhesion materials have already undergone price cuts through centralized procurement—particularly with the Henan public hospital alliance’s volume-based procurement having already entered the renewal stage—previous winning bid prices are expected to serve as an important reference for this round of centralized procurement in the Beijing-Tianjin-Hebei region.

According to the logic of exchanging price for volume, as the scale of centralized procurement expands, the of price reduction usually increases accordingly. However, under the current "anti-involution" new situation of centralized procurement, the final selection rules still need to be confirmed after the official procurement documents are released.

Industry insiders noted that, judging from the centralized procurement of hemostatic materials in the Beijing-Tianjin-Hebei region, companies producing anti-adhesion materials are also expected to adopt relatively cautious bidding strategies, but may adjust their bids only at the decimal-point level on the basis of the original winning prices in order to improve their chances of being selected at a higher ranking.

Based on product characteristics, the domestic market for anti-adhesion materials is relatively fragmented. Large-scale centralized procurement is likely to accelerate industry consolidation. Smaller companies with weak bargaining power may face being phased out, while domestic enterprises with a wide range of products, large scale, and achievements in high-end segments—such as Hybio, Yantai Wanli, and Hangzhou Xiehe Medical—are likely to capture a greater market share.

The orthopedics market has emerged from the shadow of price cuts, while the anti-adhesion sector faces its first major alliance test. Centralized procurement has entered the second half, and competition has shifted from price battles to technological breakthroughs; the real contest has just begun.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Eastman France PET Depolymerization Plant: Project "Alive," But Construction Paused

-

Mitsubishi Chemical Plans To Split Petrochemical Business By 2028

-

Bola Carbon Black Announces Global Restructuring of Specialty Carbon Black and Multi-Walled Carbon Nanotube Business

-

900,000-Ton-Per-Year Ethylene Plant Shut Down! ExxonMobil Reshapes Asia-Pacific Petrochemical Landscape