Surge Of 47%, 1.84 Million Tons Of Production Halted, Monthly Exports Hit New High! PP At Highs Suddenly Hits “Emergency Brake,” Is A Turning Point Coming?

Since the beginning of 2026, geopolitical conflicts in the Middle East have triggered a surge in plastics and chemical prices, driving the chemical market to rebound against the trend after halting its decline. Recently, data from the National Bureau of Statistics showed that from January to April, the total profits of the chemical raw materials and chemical products manufacturing industry reached 191 billion yuan, up 73.4% year on year, leading all major industrial sectors.

In this round of profit frenzy in the chemical industry, polypropylene (PP) has stood out as a core benchmark. Boosted by multiple favorable factors—including geopolitical conflicts, concentrated plant maintenance shutdowns, and explosive export growth—PP prices have nearly doubled in the past two months. But just as bullish sentiment was running high, both futures and spot markets weakened in tandem on May 29, abruptly slamming the brakes on the high-level rally.

01 Surged 47.4% in two months, supply shortages and rising prices have become the norm

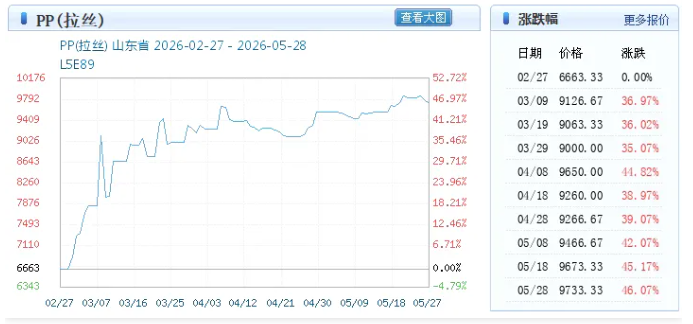

Since the second quarter, the domestic PP market has been on a one-way upward trend. According to data from Plas.com and Tonghuashun, raffia-grade PP in Shandong rose from its year-to-date low of RMB 6,690/ton on February 25 to a peak of RMB 9,856.67/ton in late May.An accumulated increase of 3166.67 yuan/ton, with a growth rate of 47.4%.。

(Image source: Business Society)

This round of price increases is characterized by a stepwise upward trend.

· Early MarchBreak through 7,800 yuan/ton, with a stage increase of over 16%.

· Mid-Marchsurged to 8,900 yuan/tonne, with the cumulative gain widening to 33.7%;

· April–MayAfter consolidating at high levels, it surged again in late May, maintaining strength throughout the second quarter.

The core characteristics of the market in the second quarter were tight supply leading to rising prices, a tight spot market, and companies holding firm on prices.

02 Sudden Market Shift! Pullback Signal Officially Emerges

The strong rally that lasted for more than two months cooled noticeably on May 29.

According to Longzhong Information data, today (May 29) PP futures fluctuated and moved lower, and the spot market also weakened in tandem. The mainstream quotation for raffia-grade PP in East China is 9,500–9,800 yuan/ton, and in the Hangzhou market 9,500–9,700 yuan/ton. Traders are proactively offering concessions to move cargo, and trading activity is subdued.

Weekly data shows that PP spot prices fell by 100 yuan/ton this week, a decrease of 1.02%, with the latest price at 9723.33 yuan/ton, significantly down from the recent peak, indicating a high-pressure market situation.

03 Supply support remains in place, and the tight balance has not broken down.

The core positive driver of this round of price increases — supply contraction — has not fundamentally reversed.

According to statistics from Plas and JLC, the PP industry saw a large-scale wave of maintenance in May.The maintenance capacity for the month exceeds 1.84 million tons.。

(Image source: Pulasi)

The maintenance cycles for the main units of companies such as Sinopec-SK Petrochemical and Shenhua Ningxia Coal exceed one month, with restart dates for some still to be determined. The impact of the supply contraction will continue into June and July.

The cost support remains strong. According to Longzhong data, the current weekly average cost of PDH-produced polypropylene is 10,650.22 yuan/ton, and the weekly average cost of oil-produced polypropylene is 9,511.23 yuan/ton, indicating that there is limited room for further significant declines.

However, marginal changes have emerged: the parking devices that were previously shut down are gradually restarting, the loss due to maintenance has decreased month-on-month, and the most critical phase of supply shortages is passing.

04 Requirements Drag Behind, Off-Season Effects Become More Pronounced

The core factor currently weighing on the market is weak downstream demand during the off-season.

The downstream industries such as woven plastics, film, and injection molding have entered the traditional off-season for consumption. End-user operating rates remain sluggish, with only rigid-demand replenishment being maintained, and large-scale chasing of price increases has basically disappeared. According to data from JLC,BOPP operating rate was only 59.85%, while CPP operating rate fell to 47.23%.。

Market feedback generally indicates that downstream buyers are clearly resistant to high-priced raw materials, and actual transactions are largely concluded through concessions from traders.

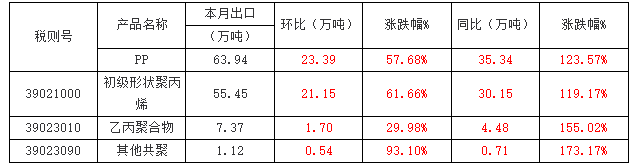

05 Explosive Growth in Exports Becomes the Biggest Highlight

Against a backdrop of weak domestic demand, exports have become the only demand booster for the PP market.

(April PP export statistics; source: Jinlianchuang, General Administration of Customs)

According to customs statistics:

· January–AprilDomestic cumulative PP exports reached 1.5794 million tons, a year-on-year surge of 55.1%;

· April (single month)Exports reached 639,400 tons, up 57.68% month-on-month and soaring 123.57% year-on-year.Set a new record for highest single-month exports.。

The explosive release of overseas orders has effectively absorbed domestic supply, offsetting the negative impact of the off-season in domestic demand.

06 Outlook: The unilateral uptrend has ended, with high-level consolidation likely to dominate.

The PP market is currently characterized by a mix of bullish and bearish forces, and the one-sided uptrend has already come to an end.

Supporting factorsThe million-ton-scale maintenance capacity has not yet fully resumed, and the tight supply-demand balance has not fundamentally reversed; cost support remains solid; the strong export momentum continues.

Suppressing FactorsThe downstream off-season continues, with strong resistance to high prices; plants are gradually restarting, leading to marginally looser supply; oil prices are falling, and cost premiums are gradually being eliminated.

Overall, it is difficult for PP to sustain a unilateral sharp rise in the short term, and it is more likely to remain within a range.Weak high-level consolidationSupported by low inventory levels, the probability of a significant decline is low, but due to the absence of demand in the off-season, the upside potential is limited. High-end specialty materials, benefiting from resilient demand, will perform better than general-purpose raffia grades.

Focus going forward on tracking: the progress of plant maintenance and restart, crude oil and propane prices, and the initiation of end-user restocking demand.

After surging 47% in two months and then losing momentum after meeting resistance at high levels, the logic behind this round of PP price increases has clearly shifted. A rally driven solely by supply contraction, without support from demand, has long exhausted its sustainability. Whether PP can break through again will hinge on whether off-season demand can recover and whether the strong export momentum can continue. The market may face a directional choice in June.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Eastman France PET Depolymerization Plant: Project "Alive," But Construction Paused

-

Mitsubishi Chemical Plans To Split Petrochemical Business By 2028

-

Bola Carbon Black Announces Global Restructuring of Specialty Carbon Black and Multi-Walled Carbon Nanotube Business

-

900,000-Ton-Per-Year Ethylene Plant Shut Down! ExxonMobil Reshapes Asia-Pacific Petrochemical Landscape