Rising Competitive Anxiety: European Union Considers Strengthening Trade Measures Against China!

On June 3, Bloomberg reported that the European Union is preparing to warn businesses and the public that a trade conflict between China and the EU may erupt as Brussels considers new restrictive measures against China to rebalance their uneven economic and trade relationship.

Just last week, the European Commission held a closed-door meeting to discuss its next steps. After the meeting, the European Commission publicly stated that the current China-EU trade and investment relationship is “unsustainable” and that it would take “more resolute and coordinated measures” in the future.

According to informed sources, participants generally believed in private discussions that if the European Union introduces new restrictive measures, China is very likely to take retaliatory action, so European businesses and the public need to be prepared for an escalation in trade frictions.

Intensified competitive anxiety prompts the EU to seek to reduce dependence on China.

An important reason for the shift in the European Union’s attitude is the increasing competitive pressure it faces from China.

In recent years, there has been a growing consensus among political and business circles in the European Union that if it cannot quickly enhance industrial competitiveness, narrow the innovation gap with China and the United States, and build a more resilient supply chain system, Europe’s position in the global economic landscape and industrial chain will continue to decline.

Mario Draghi, who led the European Central Bank during the eurozone debt crisis, previously warned that if Europe cannot compete effectively with the United States and China, it will fall into a “slow decline” and even “lose its reason for existence.”

To this end, Draghi recommended that the EU increase investment by €700 billion to €800 billion annually for technological innovation, the energy transition, and supply chain security, in order to reduce reliance on external markets and key technologies.

However, the reality is that the EU remains highly dependent on Chinese supply chains.

Bloomberg Economics estimates that if China's supply of rare earths and permanent magnets is interrupted for a year, approximately $4.4 trillion of global GDP will be at risk, with Germany becoming one of the hardest-hit economies in Europe. For industries such as automotive, electric motors, and industrial equipment, any disruption in the supply of critical raw materials will directly impact production activities.

Previously, European car manufacturers warned that due to heightened supply chain risks, the EU might even have to consider temporarily lifting restrictions on China's Yangzhou Yangjie Electronic Technology Co., Ltd. to avoid production disruptions caused by parts shortages.

This also exposes a reality: although Europe continues to advance “de-risking,” its dependence on China in key areas such as critical raw materials, electronic components, and the new energy vehicle supply chain will remain difficult to shake off in the short term.

Chinese automakers are accelerating their entry into the European market.

Another major source of concern for Europe is the rapid improvement in the competitiveness of China's automotive industry.

As the global automotive industry shifts toward electrification, Chinese automakers are leveraging their electric vehicle technologies, supply chain advantages, and price competitiveness to continuously expand their influence in the European market. They have also moved beyond simple product exports and are gradually advancing toward local manufacturing and industrial chain deployment.

According to data from the European Automobile Manufacturers Association (ACEA), in April of this year, Chinese automakers achieved a record market share of 9.8% in Europe. Compared to the same period last year, sales of Chinese automakers in Europe more than doubled, with an increase of 114%, reaching 112,992 vehicles. The sales of pure electric vehicles grew by 111% year-on-year, reaching 38,281 units, with their share of total pure electric vehicle sales in Europe surpassing 15% for the first time in that month.

From January to April, several Chinese automakers further expanded their market share in Europe.

Among them,BYDThe share of new car registrations in the EU, UK, and European Free Trade Association markets has reached 2.2%. The company plans to achieve full localization of electric vehicle production in the European market by 2028 and is in discussions with European car manufacturers such as Stellantis regarding the acquisition of idle factories in Europe.

Chery AutomobileIt has continued to build influence through brands such as Chery, Omoda, Jaecoo, and Jetour, achieving a 2% market share in Europe from January to April. At present, Chery has established a joint venture with Spanish automaker EBRO to advance localized production at the former Nissan plant in Barcelona. In addition, reports indicate that Chery also plans to produce vehicles at Nissan’s Sunderland plant in the UK.

China FAW GroupRed Flag brandIt is also accelerating its expansion in Europe. According to foreign media reports, Hongqi is in talks with Stellantis about using its factory in Spain for local production, and plans to launch more than ten new energy vehicle models in Europe by 2028.

It has become the Chinese automotive group with the largest market share in Europe. Backed by brands including Volvo, Polestar, Lotus, LEVC, Lynk & Co, Zeekr, and Smart, the Geely group accounted for 2.5% of new car registrations in the European market in the first four months of this year. In March this year, Volvo Cars and Geely Auto reached a cooperation agreement under which Volvo would be responsible for the import and distribution of Lynk & Co electric vehicles in the European market.

According to Spanish media reports, Geely has also acquired a partial stake in a Ford factory located in Valencia, Spain.

SAIC Motor Corporation LimitedThen, leveraging the MG and Maxus brands, it became the second-largest Chinese automaker in Europe, with a market share reaching 2.4% from January to April this year. In June, the government of Spain’s Galicia autonomous community disclosed that SAIC plans to build its first vehicle assembly plant in the EU there, with an initial investment of about 200 million euros.

At the same time,Xpeng MotorsIt is discussing the acquisition of European plants with companies including Volkswagen; currently, Magna Steyr is assembling two models for Xpeng in Graz, Austria, to supply the European market.

Leap MotorTo further deepen cooperation with Stellantis, both parties plan to launch a joint production project in Spain, extending from sales cooperation to manufacturing collaboration. In the first four months of this year, Leap Motor's new car registration share in the European market reached 0.7%.

From exporting complete vehicles to building factories, acquiring production capacity, and establishing capital and manufacturing partnerships with local European automakers, Chinese car companies are participating in the European automotive industry chain in increasingly deeper ways. For Europe, this means that competition from China’s automotive industry is no longer limited to imported products, but is beginning to enter the local European market and manufacturing system directly.

This shift from trade exports to industrial penetration is becoming one of the important reasons for the EU to re-examine its economic and trade relations with China.

More importantly, this trend is not confined to the automotive industry, nor is it limited to Europe. Statistics from the OECD show that over the past two decades, Chinese companies have significantly increased their market share across major manufacturing sectors worldwide.

Trade imbalance and the intensifying dispute over “subsidies and overcapacity”

As Chinese companies expand their influence in Europe and global markets, discussions between China and Europe regarding trade balance and industrial competition continue to intensify.

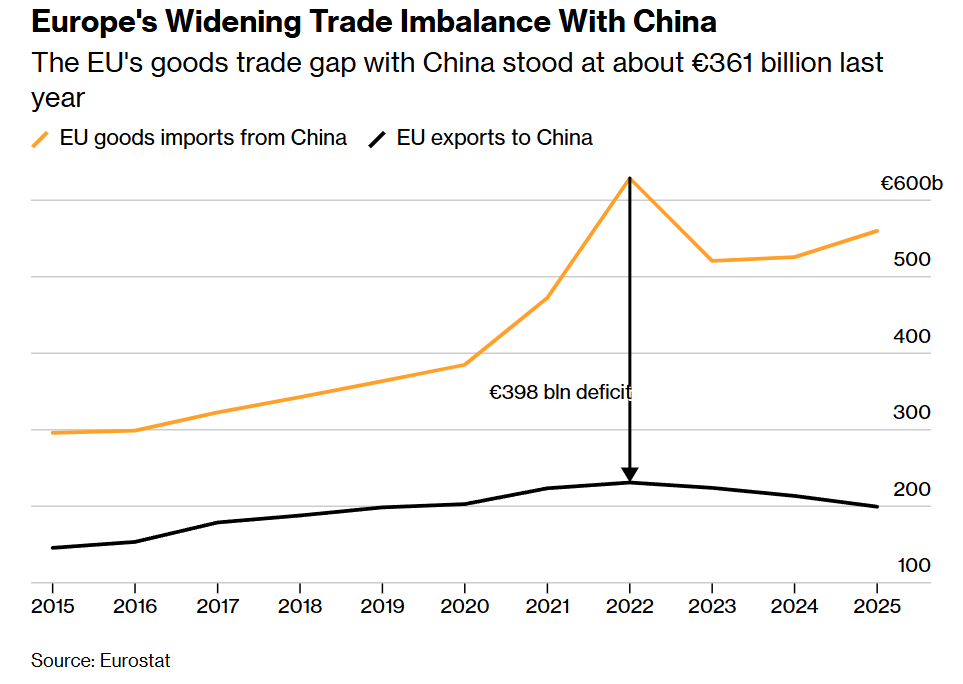

According to data from the Chinese Ministry of Foreign Affairs, the EU was China's second-largest export market last year. Meanwhile, EU data shows that the trade deficit with China is expected to be around 361 billion euros by 2025.

The chart shows the EU’s trade deficit with China: the orange line represents the value of EU imports from China, while the black line represents the value of EU exports to China; data source: Eurostat.

This trend has continued into 2026. Official Chinese data show that China’s exports to the European Union have increased by 19% year on year since the start of 2026, compared with an 8% increase for the whole of 2025.

An analysis conducted by the relevant institutions of 2026 customs data found that, with the massive influx of Chinese electric vehicles, the trade imbalance between the EU and China reached a record high in the first quarter of this year. This surge came as Chinese automakers faced weakening domestic demand and moved aggressively into Europe. Meanwhile, as the war in the Middle East pushed up gasoline prices at gas stations, European consumers turned to greener alternatives.

Against this backdrop, in the first four months of this year, China’s trade surplus with the 27 EU member states reached a cumulative US$113 billion, an increase of US$22 billion from US$91 billion in the same period of 2025. At this pace, the full-year surplus in 2026 will hit a new record high.

The EU believes that Chinese companies are rapidly expanding their market share in fields such as new energy vehicles, photovoltaics, steel, shipbuilding, and telecommunications equipment, which is closely related to government support and industrial policies. The European Commission is studying how to use existing trade tools to address the issues of "overcapacity" and "unfair competition" as defined by it.

In this regard, China has always held a different view. China believes that industrial support policies are common practices internationally and comply with World Trade Organization rules. Chinese Foreign Ministry spokesperson Mao Ning recently stated that whether it is "de-risking," "reducing dependence," or the so-called "trade imbalance," they are essentially different expressions of protectionism. She also warned that related measures will ultimately raise costs for European companies and weaken their long-term competitiveness.

From an industrial perspective, the core of the dispute between the two sides is not merely the trade figures themselves, but rather the competition for dominance in the global new energy vehicle sector, advanced manufacturing, and critical supply chains.

The EU may further strengthen its trade defense instruments.

Facing intensifying competitive pressure, the European Union is considering further strengthening its trade defense system.

In addition to the anti-subsidy investigations and tariff measures that have already been implemented, the European Commission is also evaluating new policy tools to address the so-called "overcapacity in Chinese manufacturing" issue and enhance protection for key industries.

EU Industry Commissioner Stéphane Séjourné recently said that European companies still do not attach enough importance to supply chain and geopolitical risks, and that in the future the EU will make greater use of tariffs, import quotas, and other measures to protect domestic industries.

It is reported that Brussels is also discussing whether to activate the EU’s toughest trade tool—the Anti-Coercion Instrument. Once activated, the EU could take measures including raising tariffs, imposing additional taxes and fees, and restricting investment.

In response, China’s Ministry of Commerce stated that if the European Union unilaterally introduces new trade tools and implements discriminatory restrictive measures, China will resolutely take countermeasures to safeguard its legitimate rights and interests.

However, even with rising external pressures, there are still significant differences within the European Union regarding how to respond to China.

Countries such as France have consistently advocated for tougher industrial protection policies, and French President Emmanuel Macron has called on the European Union to adopt measures to protect strategic industries, similar to those being used by the United States.

Spain tends to maintain an open cooperative relationship with China. Spanish Prime Minister Pedro Sánchez stated during a recent visit that the European continent needs to "open its doors to China so that Europe does not have to close itself off."

Germany, which is highly dependent on export markets, has long worried that an escalation of trade conflicts could hurt its own interests. German Economy Minister Katherina Reiche recently said that when unfair competition is detected, Europe needs to take action to protect its domestic industries, but Germany is also an export-oriented country, so it needs to strike a balance between protecting industry and maintaining open markets.

Nevertheless, growing signs suggest that Germany’s stance on strengthening trade defense tools is changing, and that it is willing to discuss new policy instruments to address the issue of overcapacity.

Later this month, EU leaders will hold a summit in Brussels to discuss whether to authorize the European Commission to draft new trade proposals.

Have China-EU economic and trade relations shifted from complementarity to competition?

Regarding the current escalating trade frictions between China and Europe, Sun Chenghao, a researcher at the Center for International Security and Strategy at Tsinghua University, believes that an important change is that China-Europe economic and trade relations are gradually shifting from the high degree of complementarity of the past toward more direct industrial competition.

Taking the automotive industry as an example, for a long period of time, the relationship between the Chinese and European automotive industries was more characterized by market cooperation and complementarity: China was one of the most important growth markets for European automakers, while Europe exported technology, brands, and high-end products to China.

However, with the rapid rise of China's smart electric vehicle industry, this relationship is changing.

Today, Chinese automakers are not only important participants in the European market, but are also becoming direct competitors to Europe’s domestic automotive industry; meanwhile, China’s importance in power batteries, key minerals, electric drive systems, and intelligent supply chains continues to increase.

For Europe, the current challenge is no longer merely how to cope with rising imports, but how to maintain technological innovation and industrial competitiveness amid a new wave of transformation in the automotive industry. For Chinese automakers, the European market remains one of the most strategically valuable regions in their global expansion. As more and more companies shift from “exporting to Europe” to “putting down roots in Europe,” the relationship between the Chinese and European automotive industries is also moving beyond the past model of market complementarity and gradually entering a new stage marked by both competition and cooperation.

From a broader perspective of economic and trade relations, as China continues to promote industrial upgrades and Europe accelerates its efforts to strengthen industrial protection and supply chain security, competitive factors between China and Europe are on the rise. Whether both sides can find a new balance between competition and cooperation in the future will be key to influencing the direction of China-Europe economic and trade relations.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped

-

Ethylene Industry Enters Production Boom Period! Multinational Giants and Domestic Leaders Compete in Trillion-Dollar Track

-

Target To Reduce Plastic By 30%! South Korea Enters Plastic Recycling Controversy, Involving National Interests

-

Amer Sports Releases 2025 Sustainability Report, Apparel And Footwear Recycled Material Proportion Reaches 19.3%