Q1 2026 customer transaction value released: Who Is Still Engaged in Price Wars?

Since the beginning of this year, the “price war” in the auto market has gradually subsided, and there has been increasing reflection within the industry on low-price competition. Recently, a senior executive of an automaker said in a media interview that companies cannot rely on price wars for the long term; once the low-price limit is broken, the industry will face huge hidden risks in its operations. What the automotive industry truly needs to compete on is technology, service, quality, brand, and corporate social responsibility.

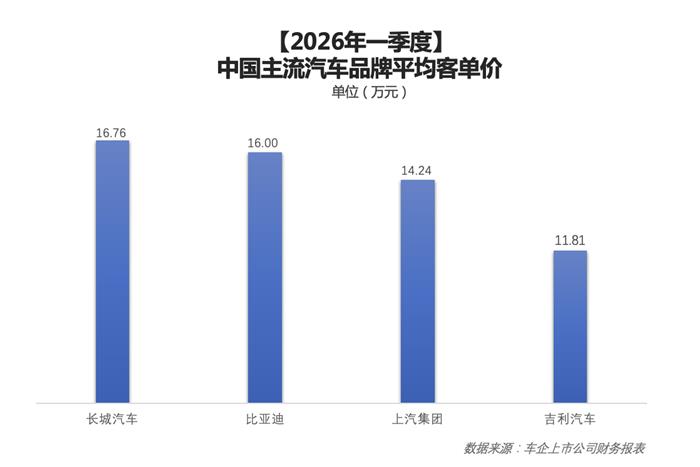

This judgment aligns with the current changes in competition within the Chinese auto market. In the first quarter of 2026, the average transaction price of mainstream automotive brands in China was as follows: Great Wall Motors at 167,600 yuan, BYD at 160,000 yuan, SAIC Group at 142,400 yuan, and Geely Auto at 118,100 yuan, all higher than the levels in 2025. However, the data on average transaction prices in the first quarter intuitively reflects the differences in pricing strategies across the industry and clearly answers the core question of "who is adhering to pricing."

In recent years, price wars were once the most direct means of competition in the automotive market. In the short term, price cuts can stimulate demand and boost sales, but as the industry enters a stage dominated by new energy vehicles, consumers’ criteria for evaluating cars are also changing. Whether the driving range is dependable, charging and refueling are convenient, driver-assistance systems are reliable, and after-sales service is comprehensive is increasingly influencing more and more users’ car-buying decisions.

More realistic pressures are also emerging. Since April, the retail penetration rate of new energy passenger vehicles in China has exceeded the 60% threshold. As NEVs move from an incremental market into the mainstream, the room for winning over users through price cuts is narrowing. Meanwhile, the auto industry’s overall profit margin was only 3.2% in the first quarter, and many automakers have adjusted prices and tightened terminal discounts. Continuing the price war is becoming increasingly unrealistic.

Compared with sales volume, the average transaction price better reflects an automaker’s product positioning and market recognition. Being able to maintain a stable average selling price per vehicle while expanding scale indicates that a company has a solid foundation in both product strength and brand power, and is therefore better positioned to continue investing in technology, quality, and service.

Judging from first-quarter data, the rise in average vehicle prices among different automakers is supported by different factors. Great Wall Motor’s average transaction price reached RMB 167,600, which is related to its continued efforts in recent years to promote product layouts in off-road vehicles and high-end new energy vehicles. BYD’s average transaction price in the first quarter was about RMB 160,000. While maintaining a high level of scale, technologies such as its second-generation Blade Battery, flash-charging technology, and “God’s Eye” driver-assistance system have been rolled out at a faster pace, further enhancing the user experience in terms of range, energy replenishment, and intelligent driving safety. SAIC Motor’s average transaction price in the first quarter was about RMB 142,400, with its own brands, new energy vehicles, and overseas markets working together as the three driving forces behind its price performance. Data show that in the first quarter of this year, SAIC Motor sold a cumulative 325,000 vehicles in overseas markets, up 48.3% year on year.

From this perspective, the average transaction price is no longer merely a figure in financial terms; it has also become a measure for assessing an automaker’s operating quality and market recognition. After the price war subsides, competition among automakers has not weakened; rather, the logic of competition has changed. If companies blindly rely on technological imitation, product benchmarking, and low-price tactics to chase sales, they are in effect overdrawing their long-term capabilities. Only by truly strengthening product value and turning technology, quality, and user experience into genuine customer recognition can automakers secure their place at the table and navigate through this period of shallow waters.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

Research progress on surface modification of white carbon black and its applications

-

Major Shake-Up! Latest China Auto Export Rankings Released

-

A Look at the Material Suppliers Behind SpaceX

-

Nike mind: Neuroscience and Foam Material Innovation Merge to Lead Low-Carbon Upgrading Technology in the Footwear Industry