[PVC Weekly Review] Policy Support Weakens, Market Continues Downward Trend

I. This Week’s Market Focus

This week, the core focus of the PVC market centered on three key indicators: supply, inventory, and pre-sales, overall showing a pattern of supply-demand imbalance and inventory accumulation, as detailed below. First, on the supply side, PVC plant capacity utilization fell by 2.46% week-on-week, while output declined by 3.43% over the same period, mainly due to maintenance shutdowns at multiple enterprises, which led to a drop in operating rates. Second, on the inventory side, PVC social inventory reached 1.2992 million tons this week, up 0.23% week-on-week and sharply higher by 102.51% year-on-year. Inventory pressure continues to build and has become a major factor weighing on the market. Third, on the pre-sales side, pre-sales volume of PVC producers increased by 4.50% week-on-week and by 2.71% year-on-year. Producers have attempted to ease inventory pressure through pre-sales, but this has failed to alter the market’s overall weak trend. China’s PVC industry is characterized by a production structure dominated by the calcium carbide process, supplemented by the ethylene process. At present, China’s total PVC production capacity is close to 30 million tons, of which the calcium carbide route accounts for about 72% and the ethylene route about 28%. The cost fluctuation logic of these two process routes differs significantly, which also directly affects the strength of cost support for PVC this week.

II. Market Trends This Week

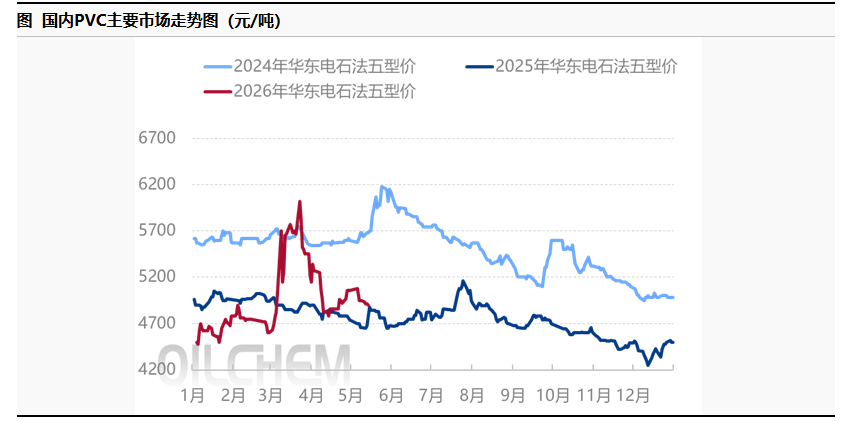

During the current period (May 8–14, 2026), the domestic PVC market generally showed weak performance. Although positive signals were released on the policy front, their support was limited. Futures prices fell back after rising, while market prices continued their downward trend. In terms of price changes across regions, the price of SG-5 PVC in North China rose from RMB 4,940/ton on May 7 to RMB 4,970/ton on May 14, up RMB 30/ton, or 0.61% month-on-month. In East China, SG-5 PVC fell from RMB 4,950/ton to RMB 4,900/ton, down RMB 50/ton, or 1.01% month-on-month. In South China, SG-5 PVC declined from RMB 5,050/ton to RMB 5,010/ton, down RMB 40/ton, or 0.79% month-on-month. The key consumption regions of East China and South China both saw noticeable declines, leading the overall market trend.

From the supply side, the number of enterprises undergoing maintenance increased this week, and the operating load of PVC units continued to decline, with both capacity utilization and output falling month-on-month. In theory, this could ease supply pressure, but the actual effect has been limited. On the demand side, performance remains sluggish, with downstream enterprises showing weak purchasing willingness and market trading activity remaining thin. Coupled with the approaching traditional off-season, demand is unlikely to provide effective support, leading to continued accumulation of social inventories and further exacerbating the loose market supply-demand pattern.

Although there have been positive policy announcements, their support for the market is limited and has not reversed the prominent supply-demand imbalance. The market shows a trend of decline after an initial rise, and PVC prices continue to decrease. As of this week, the cash prices for calcium carbide method PVC in East China range from 4,830 to 5,000 yuan/ton, while ethylene method PVC prices are mainly negotiated on a practical basis, fluctuating with the market. As the calcium carbide method is the mainstream production process for PVC, its price changes directly influence the overall market trend. Currently, the supply-demand imbalance is significant, and market expectations are not optimistic, showing a weak consolidation and a tendency for transactions to seek lower prices.

3. Market Outlook Prediction

Based on a comprehensive assessment of various factors, it is expected that the domestic PVC spot market will continue to operate weakly next week, with both supply and demand maintaining a dual weakness pattern. There is insufficient policy support and weak cost support, while intense competition within the industry continues. It is anticipated that the benchmark price for SG-5 in East China will operate in the range of 4800-5000 yuan/ton. The key areas of focus for the next period and next week will be three core directions and specific influencing factors.

For the next period, key attention should be paid to three aspects: 1. The trend of Asian contract prices in June and the implementation of domestic maintenance plans in May, as the extent to which maintenance is carried out will directly affect the subsequent supply landscape. 2. The impact of geopolitical conflicts on crude oil prices and changes in ocean freight rates, as fluctuations in crude oil prices will be transmitted to the cost side of ethylene-based PVC, thereby affecting market prices. 3. The resumption of operations in downstream industries and China’s PVC export order intake, as the pace of resumption and export orders will directly affect the strength of demand-side support.

Second, key factors to watch next week: 1. On the supply side, the operating rates of PVC units at Inner Mongolia Yili, Baotou Haipingmian, Xinjiang Tianye Tianchen and other enterprises are set to increase next week. Inner Mongolia Yili has an annual PVC production capacity of 500,000 tonnes, Baotou Haipingmian has 400,000 tonnes/year of PVC capacity, and Xinjiang Tianye Tianchen has 450,000 tonnes/year. The ramp-up in operations at these three producers will lead to a slight increase in market supply, further intensifying the pressure from ample supply [4][5]. 2. On the demand side, operating rates in downstream industries will continue to rise, and some product exporters are operating well. In terms of external demand, PVC demand in India has improved. Affected by the Indian government’s temporary exemption of PVC import duties until the end of June, India is expected to continue active procurement in the later period, which may provide a modest boost to China’s PVC export demand. 3. On the cost side, for ethylene, domestic PVC-related derivatives are maintaining low operating rates, reducing demand for externally purchased seaborne cargoes. Coupled with the gradual recovery of cracker operating rates in South Korea, ethylene prices in US dollar terms are expected to have further downside potential, further weakening cost support for ethylene-based PVC. For calcium carbide, instability in current market supply and demand has intensified; some calcium carbide units under maintenance have resumed operation, while downstream maintenance has been implemented successively. The calcium carbide market is expected to see intensified supply-demand bargaining next week, with prices likely to continue rising, which may provide some cost support for carbide-based PVC, but is unlikely to change the overall weak pattern.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Daily Review: Cost and Supply Support Push Polyester Bottle Film Market Higher

-

Polyester bottle flake market continues to decline

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

Phased Rally Ends, Polypropylene Returns to Fundamental Consolidation