Plastic Optical Fiber (POF) Industry Investment Opportunity Analysis and Market Size Forecast

I. Core Conclusion

1. The industry as a whole is in the early growth stage, transitioning from a “supporting material for consumer electronics” to a “core substrate for AI and automotive intelligence.” Plastic optical fiber (POF), also known as polymer optical fiber, is a flexible optical transmission medium with a core made of PMMA or perfluorinated polymers, offering key advantages such as controllable cost, excellent flexibility, immunity to electromagnetic interference, and ease of installation. According to QYResearch, the global plastic optical fiber (POF) market was valued at approximately USD 6.62 billion in 2025 and is expected to reach USD 11.93 billion by 2032, representing a CAGR of about 8.9%. However, this overall growth rate masks significant structural divergence within the market: traditional products represented by step-index POF (SI-POF) have entered the mid-growth stage in consumer electronics and home networking; high-performance products represented by graded-index POF (GI-POF) are in the early growth stage in fields such as automotive, industrial automation, and data centers; while frontier technologies such as multi-core GI-POF remain at a very early introduction stage for applications in AI data centers. In May 2026, a research team from Keio University in Japan successfully demonstrated ultra-high-speed transmission of 212.5 Gbps over 50 meters using GI-POF, with bandwidth exceeding that of quartz multimode optical fiber. This technological breakthrough fundamentally reshapes the positioning of plastic optical fiber in high-speed data communications.

2. The wave of automotive electrification and intelligentization is becoming the strongest growth engine for plastic optical fiber. Thanks to its excellent EMI immunity, bending tolerance, and high-speed data transmission capability, plastic optical fiber is accelerating the replacement of copper cables in in-vehicle infotainment systems, lighting control, sensor data transmission, and ADAS systems. As the penetration of electric vehicles and autonomous vehicles increases, in-vehicle networks are experiencing a sharp rise in demand for lightweight, interference-resistant, high-bandwidth communication links. The automotive electronics industry remains the main driver of POF—infotainment systems, lighting, multimedia networks, and sensors are increasingly relying on POF. Automotive standard systems represented by the MOST (Media Oriented Systems Transport) bus protocol have fully supported POF, further consolidating its position in in-vehicle networks.

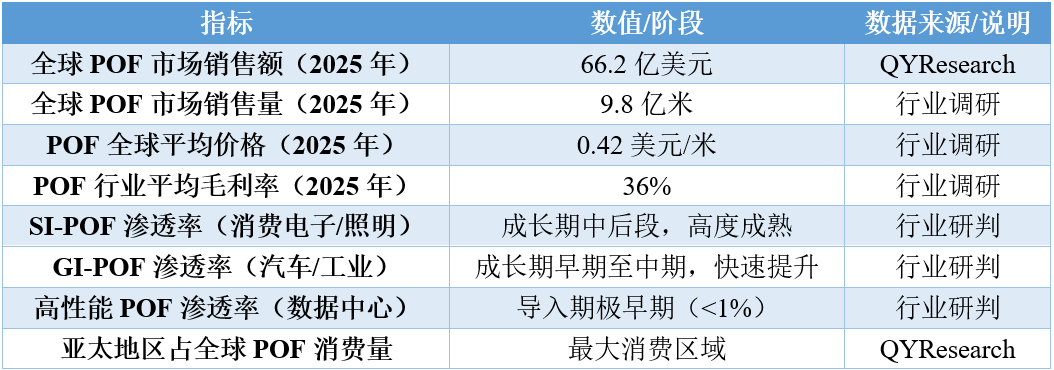

3. The AI data center and industrial automation are opening a second growth curve, with high-performance POF breaking through traditional application boundaries. High Performance Plastic Optical Fiber (POF) has surpassed its early positioning as a convenient alternative to glass fiber and copper cables, and is increasingly being assessed as an engineered interconnect platform that balances bandwidth, bend resistance, vibration resistance, and ease of installation. In May 2025, a team from Keio University developed multi-core GI-POF technology, achieving ultra-high-speed transmission of 106.25Gbps with a single core, providing high-density, low-latency, and high-capacity optical communication solutions for the next generation of AI data centers. In the field of industrial automation, POF is widely used in control systems and factory networks, ensuring reliable short-distance data transmission in harsh environments. According to industry research, the global POF market sales volume is expected to reach 980 million meters in 2025, with a global average price of $0.42 per meter and an average market gross margin of 36%.

4. The competitive landscape is characterized by “Japanese and European players dominating the high-end segment, while China is accelerating its catch-up,” with a window for domestic substitution now opening. Major participants in the global plastic optical fiber market include Japanese and European companies such as Asahi Kasei, Mitsubishi Chemical, Toray Group, AGC, LEONI, and FiberFin. Japanese companies hold significant technological advantages in GI-POF and high-performance perfluorinated POF. Chinese companies have achieved a certain scale in PMMA-based POF and the mid- to low-end market, but are still catching up in the fields of high-end GI-POF and perfluorinated POF. After 34 years of technical efforts, domestic companies such as Sun Telecom have broken the foreign monopoly in communication-grade plastic optical fiber. Tianxin Optical Fiber has independently developed and mass-produced 5 Mbps, 10 Mbps, and 50 Mbps plastic optical fiber transceivers and their core components, while R&D on its second-generation long-distance, high-bandwidth plastic optical fiber communication transceivers is also progressing steadily.

5. Three scenarios reveal that, under the base-case scenario, the global plastic optical fiber market is expected to exceed USD 10 billion by 2030. Under the optimistic scenario, accelerated POF penetration in AI data centers, coupled with stronger-than-expected automotive intelligence growth, could drive the global POF market beyond USD 13 billion by 2030. Under the base-case scenario, all end-use segments are expected to advance steadily at their current growth rates, with the overall industry CAGR reaching about 8%–9% and the market size totaling approximately USD 10–11 billion by 2030. Under the pessimistic scenario, if the AI investment cycle weakens or competition from copper cables and glass optical fiber intensifies, the market size would be around USD 8.0–8.5 billion.

2. Industry Status and Investment Cycle Opportunity Assessment

1. Industry Penetration Rate: Traditional applications are highly mature, while penetration in high-performance sectors is accelerating.

The analysis of the permeability of plastic optical fibers needs to distinguish between product generations (SI-POF and GI-POF) and application scenarios (consumer electronics, automotive, industrial, data centers) across two dimensions.

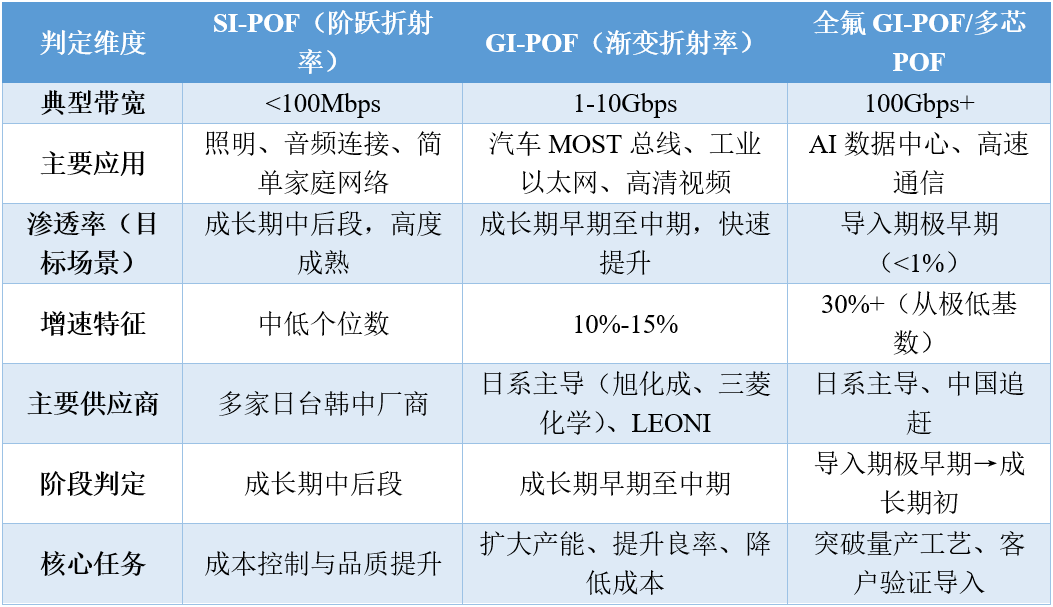

From the perspective of product generation penetration rates, step-index plastic optical fiber (SI-POF) is the most traditional POF product, with a larger core diameter (typically 0.5-1mm) and limited bandwidth (usually <100Mbps). It is mainly used for short-distance lighting, consumer electronic audio connections, and simple home networking. This category has entered the later stage of its growth phase, with a high penetration rate but slowing growth. Gradient-index plastic optical fiber (GI-POF) significantly improves bandwidth to Gbps levels by precisely controlling the refractive index distribution to reduce mode dispersion. The penetration rate of GI-POF is rapidly increasing in applications such as automotive MOST bus, industrial Ethernet, and high-definition video transmission, positioning it in the early to mid stage of its growth phase. Perfluorinated GI-POF further reduces material dispersion, with transmission performance approaching that of quartz multimode fibers, and is currently in the introduction phase in data centers and high-speed communication fields.

From the perspective of penetration in the automotive sector, in-vehicle networks represent the application scenario with the highest penetration rate and the most stable growth for plastic optical fiber (POF). POF has already achieved relatively high penetration in in-vehicle infotainment systems (MOST bus), with most mid- to high-end vehicles using POF as the transmission medium for automotive multimedia networks. With the growing adoption of electric vehicles and autonomous vehicles, the application of POF in sensor data transmission, ADAS, and lighting control is expanding rapidly. Automotive OEM demand for POF is shifting from an “optional configuration” to a “standard configuration.”

From the perspective of industrial automation penetration, POF is steadily gaining adoption in industrial control systems. Factory automation, robotics, and control systems require cables capable of ensuring reliable short-distance data transmission in harsh environments. With its resistance to electromagnetic interference and bending tolerance, POF is gradually replacing copper cables in areas such as motor drives, motion control, and fieldbus applications. However, the industrial sector has extremely high requirements for reliability and durability, and POF certification cycles are relatively long, resulting in a more measured pace of penetration growth.

From the perspective of data center penetration, this is currently the segment with the lowest penetration rate but the greatest growth potential. Traditionally, short-reach interconnects in data centers have been dominated by silica multimode optical fibers, and POF has failed to enter the market due to bandwidth limitations. However, technological breakthroughs in 2025–2026 are changing this landscape—multicore GI-POF has achieved 106.25 Gbps transmission per core, and in May 2026 it further reached 212.5 Gbps over a 50-meter distance. With AI data centers urgently requiring high-density, low-cost, and easy-to-deploy optical interconnect solutions, POF’s penetration rate in short-reach “server-to-switch” links is expected to rise rapidly from its current extremely low level.

From the perspective of domestic substitution penetration, the global high-end plastic optical fiber market is still dominated by Japanese and European companies. Japanese enterprises such as Asahi Kasei, Mitsubishi Chemical, Toray Group, and AGC hold significant technological advantages in GI-POF and perfluorinated POF. LEONI of Germany occupies a leading position in automotive POF wiring harnesses. Chinese companies have developed a certain scale in PMMA-based POF and the mid- to low-end market, with companies such as Jiangxi Dasheng, Sichuan Huiyuan, and Jiangsu TX capable of mass supply. Saintnex Optics has broken the foreign monopoly in communication-grade plastic optical fiber after 34 years of technological development. Tianxin Optical Fiber has independently developed and mass-produced 5 Mbps, 10 Mbps, and 50 Mbps plastic optical fiber transceivers and their core components. However, domestic companies still lag behind international leaders in high-end GI-POF and perfluorinated POF, and domestic substitution is at a critical stage of moving from “catching up” to “running in parallel.”

Table 1: Key Indicators of Penetration Rate in the Plastic Optical Fiber Industry

Data source: publicly available market information, Jiusi Research Institute

Phase determination conclusion: The overall plastic optical fiber industry is still in the early stage of growth, but with significant structural differentiation within the segment. SI-POF has entered the mid-to-late stage of growth in consumer electronics and lighting applications; GI-POF is in the early-to-mid stage of growth in automotive and industrial automation applications, with rapid penetration increase; high-performance perfluorinated GI-POF is in the very early introduction stage in AI data center applications. The industry's most core growth drivers have shifted from "steady demand in consumer electronics and home networking" to a three-engine model driven by "automotive electrification and intelligence + AI data centers + industrial automation."

2. Industry Growth Rate: Overall medium-to-high-speed growth, with particularly significant growth in the high-performance segment

The growth rate of the plastic optical fiber industry shows a characteristic of "overall CAGR of about 8%-9%, with higher growth in the high-performance sector."

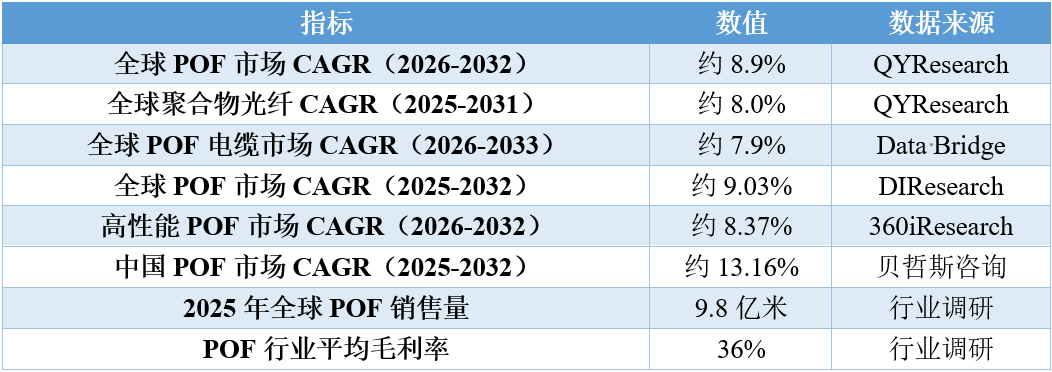

From an overall market size and growth perspective, different organizations provide slightly different growth forecasts due to variations in statistical scope. According to QYResearch, the global POF market was approximately USD 6.62 billion in 2025 and is expected to reach USD 11.93 billion by 2032, with a CAGR of about 8.9%. The polymer optical fiber market (including POF) was approximately USD 6.87 billion in 2024 and is projected to reach USD 11.65 billion by 2031, with a CAGR of about 8.0%. Data Bridge Market Research reports that the global POF market in 2025 was about USD 2.84 billion (a narrower definition, limited to cable products), and is expected to reach USD 4.96 billion by 2033, with a CAGR of 7.9%. DIResearch estimates that the global POF market will reach USD 7.278 billion in 2025 and USD 13.331 billion in 2032, with a CAGR of 9.03%. Forecasts from all institutions point to a medium-to-high growth range of 8% to 9%.

From the perspective of the growth rate of high-performance POF segments, the growth of high-performance plastic optical fibers (including GI-POF and perfluorinated POF) significantly exceeds the industry average. According to data from 360iResearch, the high-performance POF market is expected to reach approximately $1.98 billion by 2025 and $3.48 billion by 2032, with a CAGR of about 8.37%. The perfluorinated POF market is expected to be around $520 million in 2025 and reach $780 million by 2032, with a CAGR of approximately 5.3%. With the opening up of data centers and high-speed communication scenarios, the growth rate of high-performance POF is expected to further increase.

From the perspective of regional market growth, the Asia-Pacific region leads the global POF market, supported by the strong manufacturing ecosystems of China, Japan, and South Korea. China’s POF market is expected to reach RMB 13.906 billion in 2025 and grow at a CAGR of 13.16% to RMB 117.993 billion by 2032. This growth rate is significantly higher than the global average, reflecting China’s global position in automotive manufacturing, consumer electronics, and industrial automation, as well as the accelerated advancement of domestic substitution.

From the perspective of application-side growth, automotive electronics is the largest downstream application area for POF, with demand continuing to rise thanks to the trends of electrification and intelligentization. Industrial automation is another strong growth area—factories are adopting fiber-optic connections to build noise-sensitive communication networks. Although data center applications currently have a very small base, they are expected to become the fastest-growing segment with breakthroughs in GI-POF technology. In 2025, global POF market sales volume will reach 980 million meters, while the industry’s average gross margin will remain at a high level of 36%.

Table 2: Overview of Key Growth Indicators in the Plastic Optical Fiber Industry

Data source: Market public information, Jiusi Research.

3. Conclusion on Lifecycle Stage Determination: Product generational differentiation is significant, and high-performance POF is at a critical inflection point before explosive growth.

Considering multiple indicators such as penetration rate, growth rate, technological evolution, and downstream applications, the plastic optical fiber industry as a whole is in the early stage of growth, but internally it exhibits a highly significant characteristic of “product generational stratification.”

Table 3: Stage Determination Comparison Table for “Product Generational Stratification” in the Plastic Optical Fiber Industry

Data source: Public market information, Jius Research

Judgment conclusion: The plastic optical fiber industry is currently in a structural transition stage characterized by "maturation of traditional products + explosion of high-performance products." SI-POF has established a stable market structure; GI-POF is rapidly penetrating the market, benefiting from the electrification and intelligence of automobiles and industrial automation. Perfluorinated GI-POF and multi-core POF are at a critical point of transitioning from the introduction phase to the growth phase, catalyzed by demand from AI data centers. Technological breakthroughs in 2025-2026 (demonstrations of 106.25Gbps and 212.5Gbps transmission) will validate the feasibility of POF in short-distance interconnects in data centers. The core growth drivers of the industry have shifted from the "stable demand of consumer electronics and home networks" to a tri-engine drive of "automotive intelligence + AI data centers + industrial automation." High-performance POF is upgrading from a "supporting category" in electronic materials to a "strategic material" in AI infrastructure.

III. Market Size Forecast

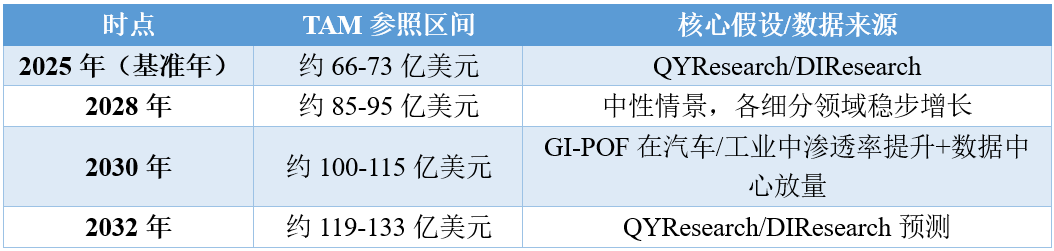

1. Estimation and Analysis of Total Addressable Market (TAM)

The TAM calculation for the plastic optical fiber market needs to be analyzed hierarchically from three levels: the global all-category market, the high-performance POF segmented market, and the regional market.

From the perspective of the global all-category market, different institutions provide varying market size forecasts due to differences in statistical scope. QYResearch data show that the global POF market will reach approximately USD 6.62 billion in 2025 and is expected to grow to USD 11.93 billion by 2032. The polymer optical fiber market (a slightly broader definition) was approximately USD 6.87 billion in 2024 and is projected to reach USD 11.65 billion by 2031. DIResearch data indicate that the global POF market will reach USD 7.278 billion in 2025 and USD 13.331 billion by 2032. Data Bridge Market Research, using a narrower definition limited to cable products, estimates the market at approximately USD 2.84 billion in 2025, rising to USD 4.96 billion by 2033. All institutions’ forecasts point to a long-term market opportunity on the order of tens of billions of U.S. dollars.

From the perspective of the high-performance POF sub-segment TAM, this is the segment with the greatest growth elasticity. According to 360iResearch, the high-performance POF market was approximately USD 1.98 billion in 2025 and is expected to reach USD 3.48 billion by 2032. The perfluorinated POF market was approximately USD 520 million in 2025 and is projected to reach USD 780 million by 2032. As AI data centers drive explosive demand for high-speed, short-reach optical interconnects, the TAM for high-performance POF is expected to expand further.

From the perspective of TAM in the Chinese market, China is one of the largest POF consumer markets in the world. According to Beijieshi Consulting, the market size of POF in China is expected to be approximately 13.906 billion RMB (around 1.9 billion USD) in 2025, and it is projected to reach 117.993 billion RMB (around 16 billion USD) by 2032, with a CAGR of approximately 13.16%. The growth rate of the Chinese market significantly exceeds the global average, mainly benefiting from its global leading position in automotive manufacturing, consumer electronics, and industrial automation, as well as the accelerated advancement of domestic substitution.

Table 4: Global TAM Outlook Reference for Plastic Optical Fiber

Data sources: Public market information, JiuSi Research

2. Three-Scenario Forecast Analysis

This forecast focuses on the global market size of the full range of plastic optical fiber products. The core differences among the three scenarios lie in the interplay between the pace of POF penetration in AI data centers, the pace of automotive electrification and intelligence, the investment cycle in industrial automation, and the progress of domestic substitution.

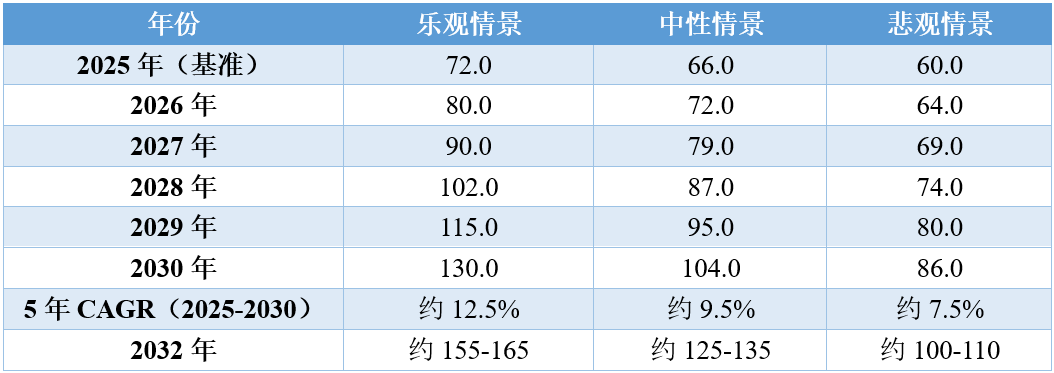

Table 5: Global Plastic Optical Fiber Full-Category Three-Scenario Forecast

Unit: USD 100 million

Data source: Jiusi Xingyan

Note: The comprehensive forecast covers all POF categories, including SI-POF, GI-POF, and perfluorinated POF. Differences in CAGR across scenarios mainly reflect variations in the pace of POF penetration in AI data centers, the electrification of the automotive sector, and the progress of domestic substitution.

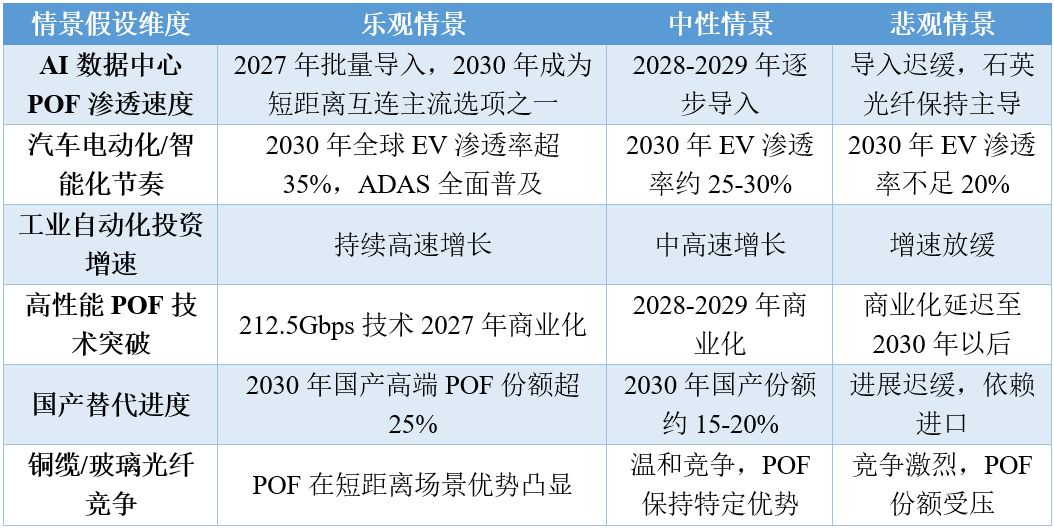

Table 6: Comparison of Core Assumptions Across Three Scenarios for Plastic Optical Fiber

Data source: Jiusi Xingyan

The optimistic scenario is based on multiple favorable assumptions: "AI data center POF penetration exceeding expectations + acceleration of automotive electrification and intelligentization + rapid commercialization of high-performance POF technology + comprehensive acceleration of domestic substitution." Keio University’s 212.5Gbps GI-POF technology is expected to achieve commercial mass production by 2027, with POF becoming one of the mainstream options in short-distance links between "servers and switches" in AI data centers. The global penetration rate of electric vehicles is projected to exceed 35% by 2030, with in-vehicle POF networks expanding from infotainment to full-stack ADAS and autonomous driving. Investment in Industry 4.0 and smart manufacturing continues to grow rapidly. Domestic high-performance GI-POF has been certified by leading customers and is being shipped in bulk, with domestic high-end POF accounting for over 25% of the market share by 2030. The global POF market size is expected to reach approximately $13 billion by 2030, with a 5-year CAGR of about 12.5%.

Neutral scenario (baseline reference scenario). AI data center POF adoption advances steadily along the technology maturity curve, with batch-scale introduction achieved in 2028–2029. Vehicle electrification and intelligentization progress as planned, and POF penetration in in-vehicle networks increases steadily. Industrial automation maintains medium-to-high-speed growth. Domestic substitution proceeds in an orderly manner, with the domestic share reaching approximately 15–20% by 2030. Prices of high-performance POF decline moderately as capacity is released, while profitability remains relatively high. By 2030, the global POF market size is expected to reach approximately USD 10.4 billion, with a five-year CAGR of about 9.5%. Under this scenario, GI-POF penetration in the automotive and industrial sectors surpasses the 2.5% growth inflection point around 2028, while high-performance POF penetration in data centers reaches a critical threshold around 2030.

Under the pessimistic scenario, the AI investment cycle experiences a phased pullback in 2027–2028, and the adoption of POF in data centers is significantly delayed. The increase in electric-vehicle penetration falls short of expectations, with traditional internal combustion engine vehicles still dominating, leading to a downward revision in the growth rate of demand for in-vehicle POF networks. Investment in industrial automation slows due to macroeconomic factors. Progress in domestic breakthroughs in high-performance POF technology and customer certification is sluggish. Copper cables maintain their share in short-distance applications thanks to their cost advantage, while silica optical fiber remains dominant in high-speed applications. By 2030, the global POF market size is approximately USD 8.6 billion, with a five-year CAGR of about 7.5%. Under the pessimistic scenario, the plastic optical fiber industry returns to a steady growth path centered on consumer electronics and home networking, while the structural growth potential driven by high-performance applications narrows significantly.

4. Future Outlook Analysis of Key Turning Points

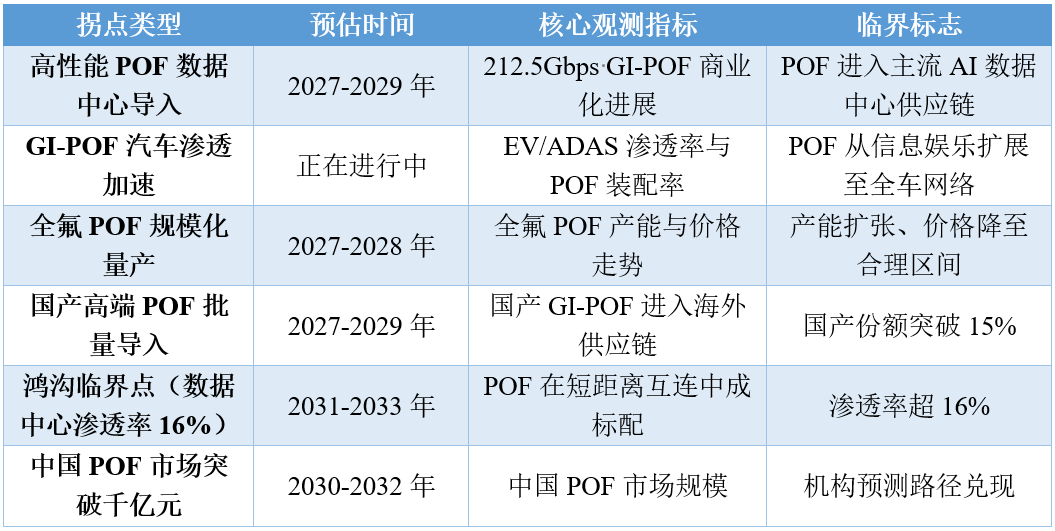

1. Turning Point Time Window Prediction

The plastic optical fiber industry is currently facing the convergence of several critical inflection points, among which the adoption of high-performance POF in data centers, the penetration rate inflection point of GI-POF in automobiles, and the domestic substitution inflection point are the most central.

High-performance POF data center import turning point - 2027-2029. In May 2025, a team from Keio University developed multi-core GI-POF technology, achieving ultra-high-speed transmission of 106.25 Gbps with a single core. In May 2026, the same team further demonstrated 212.5 Gbps transmission over a distance of 50 meters, surpassing quartz multimode fiber in bandwidth. These technological breakthroughs have cleared the bandwidth barriers for POF to enter AI data centers. In the COREnext project, demonstrations led by Infineon have explored the feasibility of POF supporting high-speed data transmission in future communication systems. It is expected that from 2027 to 2029, high-performance POF will officially enter the short-distance interconnect market of AI data centers, becoming a strong complement to quartz fibers and copper cables.

GI-POF automotive penetration growth inflection point - has partially crossed and is accelerating. The penetration rate of POF in the vehicle MOST bus has reached a high level, and mid-to-high-end models have widely adopted it. With the proliferation of electric vehicles and autonomous driving cars, the application of POF in sensor data transmission, ADAS, and lighting control is rapidly expanding. The collaboration between automotive OEMs and POF suppliers is shifting from "infotainment" to "full vehicle networking." This acceleration of the inflection point will directly drive a multiple increase in GI-POF demand.

Inflection point for large-scale mass production of perfluorinated POF: 2027–2028. Perfluorinated GI-POF has lower material dispersion and a wider transmission window than PMMA-based POF, making it a key material for achieving data rates above 100Gbps. Currently, perfluorinated POF production capacity is mainly concentrated among Japanese companies, with limited capacity and relatively high prices. As demand for perfluorinated POF is released in data centers and high-speed communication scenarios, it is expected to reach an inflection point for large-scale mass production in 2027–2028. Capacity expansion and cost reductions will drive an accelerated increase in penetration.

The inflection point for the mass adoption of domestically produced high-end POF is expected to come in 2027–2029. After 34 years of technological development, Saintnov Optoelectronics has broken foreign monopolies in the field of communication-grade plastic optical fiber. Tianxin Fiber has independently developed and mass-produced 5 Mbps, 10 Mbps, and 50 Mbps plastic optical transceivers and their core components, and R&D on second-generation long-distance, high-bandwidth products is also steadily progressing. However, domestic high-end GI-POF and perfluorinated POF still need to pass stringent certification processes before entering the supply chains of global top-tier customers, and mass adoption is expected to be achieved in 2027–2029.

Chasm Tipping Point — High-performance POF penetration in short-reach data center interconnects exceeds 16%: expected in 2031–2033. This inflection point will mark POF’s shift from an “optional solution” to a “standard configuration” in short-reach optical interconnects for AI data centers. By then, POF will capture a significant share of short-reach links such as server-to-switch and switch-to-switch connections, and the industry will enter an accelerated growth phase.

The key observation window in the near term is the second half of 2026 through 2027. Four variables will jointly determine the precise timing for the plastic optical fiber industry to move from “structural growth” to “broad-based scale-up”: the industrialization partners and commercialization timeline for Keio University’s 212.5 Gbps GI-POF technology; next-generation POF in-vehicle network plans among major global automotive OEMs; certification progress of domestically produced high-end POF among leading customers; and capacity expansion plans for perfluorinated POF.

Table 7: Predicted Key Inflection Point Times for Plastic Optical Fibers

Source: Jiusi Research Institute

2. Future Prospects Assessment

The future prospects of the plastic optical fiber industry can be summed up as follows: it is a strategic leap from being a “supporting role in consumer electronics” to becoming a “leading player in AI and automotive intelligence” — the industry’s value logic is shifting from “a low-cost substitute for copper cables” to “a strategic materials competition in high-performance optical interconnects.”

Driven by the dual forces of the AI computing era and automotive intelligence, plastic optical fiber is undergoing a fundamental shift in positioning—from a “low-cost alternative for short distances” to a “high-performance optical interconnection platform.” High-performance plastic optical fiber has long surpassed its early role and is increasingly being regarded as an engineered interconnect platform, capable of balancing bandwidth, bend tolerance, vibration resistance, and ease of installation.

From the perspective of technological evolution, plastic optical fibers (POF) are accelerating along a clear path of generational upgrades. SI-POF (<100Mbps) → PMMA-based GI-POF (1-10Gbps) → Perfluorinated GI-POF (10-100Gbps) → Multi-core GI-POF (100Gbps+), with each generation striving for the ultimate in bandwidth and transmission distance. The technological breakthroughs expected in 2025-2026—106.25Gbps single-core and 212.5Gbps transmission over 50 meters—will enable POF to surpass quartz multimode fibers for the first time in bandwidth performance. This fundamentally changes the market positioning and competitive landscape of POF.

From the perspective of application scenarios, the growth of plastic optical fiber is shifting from “single-point breakthroughs” to “broad-based expansion.” In the automotive sector, electrification and intelligence are turning in-vehicle networks from “a feature found only in a few luxury cars” into “a standard configuration in all new vehicles.” In the industrial sector, factory automation and Industry 4.0 are driving sustained demand for anti-interference, highly reliable short-distance communications. In the data center sector, the urgent need of AI computing clusters for high-density, low-cost optical interconnects is opening up an entirely new market space for POF. These three major application scenarios are jointly driving rapid growth in POF demand from different directions.

From a competitive landscape perspective, the global plastic optical fiber market is undergoing a shift from “Japan-Europe dominance” to “multipolar competition.” Japanese companies have deep technical expertise and strong patent barriers in GI-POF and perfluorinated POF. However, Chinese companies are rapidly catching up—Sentong Optoelectronics broke the monopoly after 34 years of technological development, and Tianxin Fiber has built a complete product portfolio spanning from transceivers to core components. Domestic substitution is not just about price competition, but a comprehensive catch-up in technological capability and supply chain completeness. As China further consolidates its global leadership in new energy vehicles, consumer electronics, and industrial automation, the market space for domestic POF companies will continue to expand.

From the perspective of standardization progress, in April 2025, the kick-off meeting for the revision of the national standard *Technical Specification for Plastic Optical Fiber Power Information Transmission Systems – Part 1: Technical Requirements* was held in Beijing, hosted by the Energy Research Institute of China Electric Power Research Institute. The improvement of the standard system will remove obstacles to the application of POF in new scenarios such as power information transmission. At the same time, relevant standards for Gigabit Ethernet over Plastic Optical Fiber (GEPOF) are also being advanced. The acceleration of standardization will lower the adoption threshold for downstream customers and promote POF from a “niche solution” to a “mainstream choice.”

As of mid-2026, SI-POF continues to grow steadily in the consumer electronics and lighting sectors, providing a stable foundation for the industry. GI-POF is rapidly penetrating the automotive and industrial automation markets, opening up medium-term growth opportunities. Meanwhile, under the stimulus of AI data center demand, perfluorinated GI-POF and multi-core POF are on the verge of a breakout, transitioning from the introduction stage to the growth stage. If 2024–2025 was the “year of validation” for high-performance POF technological breakthroughs, then 2026 is the “year when the inflection point is established,” marking the shift from “technology validation” to “commercial adoption.” Driven by technological breakthroughs, capacity expansion, and customer onboarding, Chinese companies are accelerating the buildout of comprehensive industrial capabilities spanning from materials to systems and from low-end to high-end products.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Research progress on surface modification of white carbon black and its applications

-

List Released! Mexico Announces 50% Tariff On 1,371 China Product Categories

-

A Look at the Material Suppliers Behind SpaceX

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

Major Shake-Up! Latest China Auto Export Rankings Released