[PA66 Weekly Review] Weak Demand Dominates, Market Remains in a Weak Stalemate

Market Focus for This Week

This week, the key focus points in the PA66 market centered on three dimensions: costs, supply and demand, and market sentiment, presenting a mixed pattern of bullish and bearish factors. First, on the cost side, raw material prices fluctuated downward, gradually weakening cost support for the PA66 market and becoming the main bearish factor weighing on the market. Second, on the supply-demand and sentiment side, downstream enterprises generally maintained a procurement pace based on immediate needs, with low purchasing enthusiasm. At the same time, polymer producers, affected by cost pressures, continued to show a strong intention to hold prices firm, resulting in evident bargaining between the two sides. Third, on the supply side, spot market supply saw a slight adjustment. During the current period, PA66 output was 19,100 tons, and the industry capacity utilization rate reached 65%, slightly lower than last week. The modest contraction in supply failed to provide effective support to the market.

2. This Week’s Market Trend

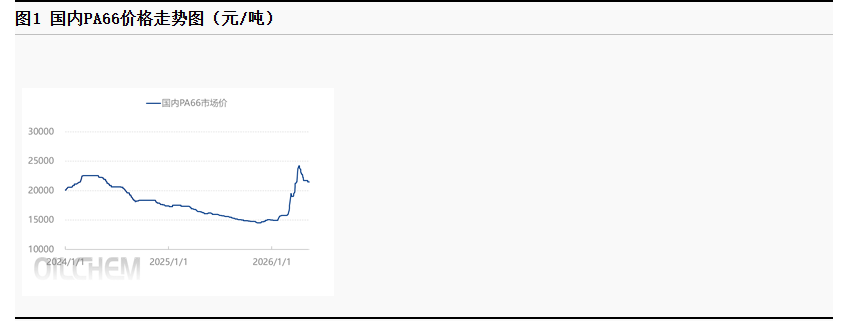

During this period (May 8–14, 2026), the domestic PA66 market generally showed a weak and fluctuating trend, with this being particularly evident in the East China market, the core trading region. This week, the average weekly spot price for small orders of PA66 in East China was RMB 21,500/tonne, down 1.15% from the previous week, indicating a slight downward shift in the market price center.

From the cost side, prices of PA66’s key raw materials, hexamethylenediamine and adipic acid, both fluctuated downward during the week. Cost support continued to weaken, directly undermining polymer producers’ confidence in holding firm on prices and becoming one of the key factors driving market prices to fluctuate lower. On the supply side, although the industry’s capacity utilization rate declined slightly from last week and spot supply saw minor adjustments, this failed to change the loose supply-demand pattern in the market.

Demand-side performance remained weak, while downstream and end markets were cautious about following up on high raw material prices, generally maintaining a need-based procurement pace. Willingness to make large-volume purchases was subdued, and market trading activity was thin. Although polymerization enterprises, under cost pressure, still intended to hold prices firm, the lack of effective demand-side support made it difficult to reverse the weak market trend. Overall industry confidence remained low, ultimately leading PA66 market prices to fluctuate weakly this week.

III. Market Outlook

Considering multiple factors comprehensively, it is expected that the domestic PA66 market will remain in a stalemated and volatile pattern in the short term. The tug-of-war between supply and demand will continue to be the core factor dominating the market trend. Overall, the market is likely to stay in a weak and deadlocked მდგომარეობ, making any obvious recovery difficult. Close attention should be paid to three key core factors:

First, on the supply side, the overall operating rate of polymerization enterprises is currently maintained at around 65%, and some manufacturers still have production cut plans going forward. There are expectations of a contraction in market supply. If the production cuts are implemented, they may slightly ease the pressure from ample supply, but it will be difficult to change the overall weak market pattern in the short term.

Second, on the demand side, downstream and end-user willingness to follow high raw material prices remains relatively weak. Overall, procurement will still mainly be driven by rigid demand replenishment, while attitudes toward bulk purchases remain cautious. It is difficult for the demand side to provide effective incremental support and it will continue to be the main factor weighing on the market.

Third, on the cost side, there are expectations of a reduction in adipic diamine supply at the raw material end. Shanghai Jieda’s adipic diamine unit was shut down on May 10, and Tianchen Qixiang plans to carry out maintenance on its ADN and adipic diamine units in June–July. As an important domestic enterprise in the nylon 66 new materials industry, Tianchen Qixiang’s maintenance shutdown will further reduce adipic diamine supply in the market. Although Yuncheng Xuyang has gradually begun sample promotion and downstream trial applications for its adipic diamine product, and its 50,000 tpa unit entered the trial production stage in April and achieved full-line integration, it is still in the early stage of market promotion and therefore provides only limited supplementation to overall supply. As a result, overall adipic diamine supply is still expected to decline, which will provide a certain degree of cost support to the PA66 market.

Overall, the short-term PA66 market is characterized by intertwined bullish and bearish factors. Persistently weak demand continues to weigh on the market, while raw material plant maintenance and price support from polymerization producers provide some support. Amid the tug-of-war between these forces, the market is expected to remain weak and rangebound.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Daily Review: Cost and Supply Support Push Polyester Bottle Film Market Higher

-

Polyester bottle flake market continues to decline

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

Phased Rally Ends, Polypropylene Returns to Fundamental Consolidation