High Oil Prices Break Cost Line: Independent Refinery Operating Rate Falls Below 54%

Since the second quarter of 2026, international crude oil prices have continued to trade above the $100-per-barrel level, exerting a significant shock on the feedstock cost side of domestic independent refineries. As earlier low-priced stockpiled feedstocks are gradually depleted, the procurement cost of imported crude oil has fully converged with international benchmarks, the discount advantage has narrowed markedly, and the economic benefits of substitute feedstocks have also weakened accordingly. As a result, independent refinery refining margins fell into deep negative territory from mid to late April. Ongoing margin deterioration, combined with seasonal maintenance, has driven the operating rate of Shandong independent refineries onto a downward trajectory.

The Dilemma of Costs: The Low Price Advantage is Gradually Losing Its Edge

In the era of low oil prices, cost advantages are the core survival logic of independent refineries. At the same time, their raw material composition consists of imported crude oil, imported straight-run fuel oil, and diluted asphalt, aiming to diversify risks and reduce overall costs.

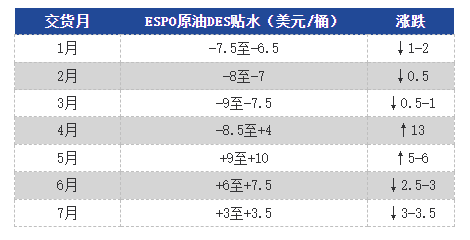

1. The discounted dividend narrowed sharply. Before the conflict, independent refineries could purchase Russian crude at a discount of USD 9/bbl; after the conflict, Russian crude gradually shifted from a USD 9/bbl discount to a premium of USD 9–10/bbl. This was mainly reflected in a significant rebound in premiums for ESPO crude arriving after mid-April, with May cargo prices rising to a peak. However, as downstream buyers’ purchasing interest continued to weaken, transaction prices for ESPO crude cargoes in June and July kept falling, and it was heard that mainstream transactions for July DES cargoes were around a premium of USD 3/bbl.

Source: JLC

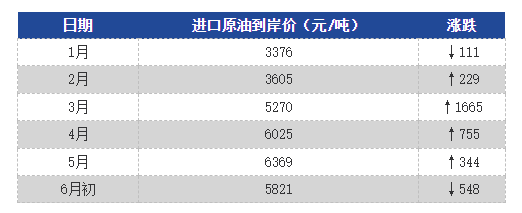

2. The cost fully "aligns with the benchmark price." According to JLC, the mainstream imported crude oil landing cost for independent refineries has surged from 50-55 USD/barrel during the low oil price period (when oil prices were 60 USD/barrel) to 105-110 USD/barrel during the high oil price period, with the overall raw material costs increasing by 2000-2800 RMB/ton compared to before the conflict.

Data source: Jin Lian Chuang

3. The cost-performance advantage of alternative feedstocks has disappeared. Straight-run fuel oil was once an important supplementary feedstock for independent refineries, but this year, due to relatively ample crude oil quotas and a sharp rise in the benchmark price of Singapore high-sulfur 380 CST fuel oil, independent refineries’ purchasing interest has cooled significantly.

According to the latest data released by the General Administration of Customs, China’s fuel oil imports in April 2026 were 976,600 metric tons, down 59.78% month-on-month and 46.56% year-on-year. Of this, fuel oil imports for the refining and petrochemical feedstock sector in April were only 421,500 metric tons, down 73.74% month-on-month and 67.62% year-on-year.

The Ulcer of Profit: The Ongoing Deepening of Theoretical Losses

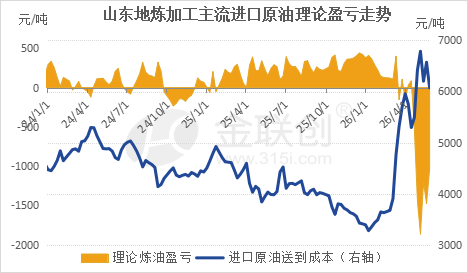

Data source: JLC

According to JLC’s profit model, since mid-to-late April, as earlier inventories of low-priced feedstock were depleted, the pass-through of high post-war oil costs caused refining profits at independent refineries to plunge into negative territory, with losses continuing to deepen. In the week of April 22, theoretical refining margins at independent refineries fell below zero for the first time to -521 yuan/tonne, and then plunged to -1,440 yuan/tonne the following week.

Overall, throughout May, high crude oil prices caused the refining profit margins of local independent refineries to collapse across the board. According to data monitored by JLC, the average theoretical refining profit of independent refineries in May stood at -1,397 yuan/ton, down 996 yuan/ton month-on-month and 1,640 yuan/ton year-on-year, hitting the lowest level in recent years.

Operating rate: Mid-term low-level fluctuations, long-term downward shift in focus.

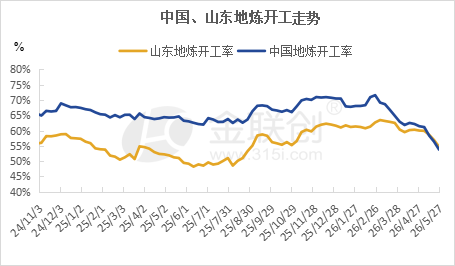

Data source: Jinlianchuang

Dragged down by high costs, many refineries in the province have successively cut runs, with some entering maintenance shutdowns. The reduction in operating rates driven by profit losses, resonating with the traditional spring turnaround season, is a rational choice for independent refineries after profit collapse, as they control operating loads to delay the transmission of high-cost pressures to the production side.

According to Jinlianchuang’s operating rate monitoring data, after declining for several consecutive weeks, the operating rate of Shandong independent refineries fell to 53.56% as of June 3, down by a cumulative 9.1% from the end of February. However, it has not yet dropped below the low level of 49.15% recorded during the maintenance peak in the same period last year.

JLC predicts that the geopolitical risk premium remains high, the situation in the Strait of Hormuz is still unclear, and combined with the complete depletion of low-priced raw material reserves leading to overall high costs, as well as expectations of increased maintenance in the future, it is estimated that the operating rate of Shandong independent refineries may maintain a low fluctuation in the range of 48%-53% in the short term. In the medium to long term, considering factors such as intensified competition from new energy alternatives, oversupply of refined oil, and accelerated industry consolidation, the operating rate of Shandong independent refineries also faces structural downward pressure.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Breaking news! formosa petrochemical olefins division lifts force majeure! asia olefins supply and demand dynamics face another reversal

-

Borouge Achieves Stellar $1.1 Billion Net Profit in 2025 Driven by Operational Excellence and Record Sales

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped

-

Gas Explosion Accident at Shanxi Tongzhou Group Liushenyu Coal Mine Results in 82 Deaths