From "Platform" to "Symbiosis", the Relationship Between Full-Load and Less-Than-Truckload Needs a Real Reform

Suppliers are increasingly staging frequent appearances to endorse new vehicles.

Last night, Bosch China officially posted on Weibo, stating, "Bosch's passive safety systems, offering millimeter-level precision protection and clear driving visibility, empower the Hua Jing S," to support and promote the global debut of the "large six-seater" model Hua Jing S that evening. This is not an isolated case. Earlier this year, ahead of the Zeekr 8X launch, suppliers such as Bosch, Faurecia Hella, Michelin, Brembo, and Valeo collectively voiced their support. Similarly, when Changan Automobile unveiled its first locally produced model in Thailand, the NEVO Q05, Autoliv announced it had fully empowered the vehicle with a "global plus localized" safety solution. Once hidden behind the scenes, automotive component suppliers are now stepping into the spotlight of new vehicle launches with unprecedented visibility.

Source: Screenshot from Weibo

From braking systems and chassis to intelligent lighting and safety systems—names once mentioned primarily in industry forums or supplier directories are now directly joining consumer-facing brand co-promotion campaigns. A large number of supply-chain “hidden champions” are collectively stepping into the spotlight. This shift reflects not only a change in corporate brand communication strategies but, more profoundly, a fundamental transformation in the automotive industry’s underlying logic.

From behind-the-scenes support to front-and-center presence, the role of suppliers has changed.

In the era of fuel vehicles, automakers firmly occupied the absolute core of the industry, while parts suppliers were long in a subordinate position, forming a one-way model of "automakers defining demand, and suppliers passively meeting it." At that time, even global giants like Bosch and Continental rarely made brand appearances at the consumer end.

This "invisible" status is both a deliberate choice and an unavoidable reality for supply chain companies. The nature of B2B business means they do not need to face end consumers directly, and long-term stable supporting relationships have made them accustomed to hiding behind the glow of brands.

But the technological revolution of electrification and intelligence has completely broken this rigid pattern.

Taking the Zeekr 8X as an example, core components such as Bosch IPB 2.0 braking systems, Michelin Pilot Sport 5E tires, and Brembo high-performance braking technology are no longer just cold terms on a vehicle specification sheet—they directly define the new car's product strengths and serve as key differentiators in building competitive advantages. When metrics like 100 km/h braking distance, turning radius, and moose test results become hot topics among consumers, the suppliers behind these technologies naturally gain visibility.

More importantly, today's consumers pay extremely high attention to core components. They will actively compare which brand's air suspension, which brand's LiDAR, and which brand's silicon carbide power control. The endorsement from suppliers not only adds to the technical credibility of the new car but also leverages the high traffic of the whole vehicle to boost their own influence, creating a win-win situation.

Faurecia said in an interview with Gasgoo that the joint promotion between original equipment manufacturers (OEMs) and supply chain companies not only has value in market promotion, but also reflects a profound change in the industry's supply and demand relationship. The two sides are moving from traditional buyer-seller supply-demand relationships toward deeper joint development and ecosystem integration. This in-depth partnership spans the entire process of their collaboration, and the joint promotion during new vehicle launch events is a natural manifestation of this deep cooperation.

Image source: Shutterstock

The underlying logic of this change lies in the fact that the technical architecture of smart electric vehicles is quite different from that of traditional fuel vehicles. In the era of electrification, if a vehicle manufacturer wants to create differentiation, it often must deeply bind with core suppliers from the early stages of R&D, co-defining the technical solutions. When the supplier's technology is deeply integrated into the vehicle's DNA, it becomes a natural progression for them to step forward and speak together.

The upgrading of consumer awareness in the market has further fueled the breaking of supply chain boundaries. Today's high-end intelligent electric vehicle buyers are often tech enthusiasts who are well-versed in 8155 chips, Orin-X computing power, 800V high-voltage platforms, and silicon carbide power control. The brand influence of suppliers, in turn, also affects purchasing decisions. Supply chain companies have keenly recognized this shift and have begun to deliberately build their own brands, moving from the industry to the general public.

A New Ecosystem of Cooperation and Competition, the Relationship Between OEMs and Suppliers is Being Restructured

The supply chain’s collective launch of a new station platform appears, on the surface, to be a marketing collaboration, but in reality, it reflects a profound restructuring of the cooperative relationship between automakers and their suppliers.

In the traditional model, the relationship between automakers and suppliers can be described as "chain-like": information is passed down from top to bottom, with demands flowing from the automaker to Tier 1, then to Tier 2 and Tier 3, and the collaboration in technology research and development is not very strong. However, in the era of smart electric vehicles, the technological innovation of a car requires the collaborative efforts of the entire industrial chain, and any single weak link can become the shortest plank in the barrel. As a result, the relationship between the two sides is gradually shifting from "upstream and downstream" to "traveling companions," and from a "buyer-seller relationship" to a strategic partnership characterized by "shared benefits and shared risks."

Valeo revealed that OEMs are indeed adopting a more open attitude toward joint promotional activities with their supply chain partners, and many OEMs proactively invite their supply chain partners to participate in such initiatives. This shift reflects the evolving industrial partnerships and value logic amid the automotive industry’s electrification and intelligentization transformation. Technological innovations by core component suppliers have become a critical enabler for OEMs to build differentiated advantages in their vehicle offerings. The supplier–OEM relationship—traditionally linear and hierarchical—is evolving into a networked structure, progressing from conventional procurement-based cooperation toward deeper, co-creation-oriented collaboration—a trend increasingly evident across the industry.

The core of this collaborative creation is the popularization of the "joint development" model. In the past, the process for a car manufacturer to launch a new vehicle was: first defining product specifications, then bidding to suppliers, choosing those who met the standards and offered the lowest price. Once suppliers received the requirements, they developed according to the set specifications, with little say in the process. Today, many new vehicles involve key suppliers from the early stages of R&D, collaborating to customize technical solutions based on the vehicle's positioning, target user group, and brand personality. The technical capabilities, R&D schedules, and production capacity planning of suppliers are deeply integrated with the car manufacturer's product matrix.

Valeo stated that on one hand, it hopes to intuitively convey the mass production results of Valeo's innovative technologies to the entire industry and end markets, showcasing its technological strength and scenario value; on the other hand, it also hopes to use this as a link to explore and build a healthy industry ecosystem of technology co-creation and value sharing with the OEMs.

Image source: SheTu.com

In the new co-opetition ecosystem, the relationship between “competition” and “cooperation” has become more nuanced. On the one hand, both parties engage in deep collaboration in technological R&D to jointly enhance product competitiveness; on the other hand, subtle competition persists over value distribution and technological authority.

Automakers are unwilling to be "strangled" by any single supplier, so they maintain control by building a diversified supply chain system. For example, they simultaneously introduce two or three battery suppliers and two intelligent driving solution providers, creating an internal competition mechanism. This approach not only ensures supply security but also gives them an advantage in price negotiations. Among the supply chain companies, there is an intense technological competition; whoever mass-produces the next-generation technology first can secure large orders from top customers, thereby defining industry standards. Millimeter-wave radar, 4D imaging radar, wire-controlled chassis, 800V electric drive... everyEverysegment is crowded with competitors.

What's more noteworthy is that some leading automakers are beginning to venture into areas that used to belong to suppliers. Developing their own chips, operating systems, intelligent driving algorithms, and even batteries—things that were once unimaginable—are now becoming a reality. The logic for automakers to extend upstream is clear: core technologies should not be controlled by others, and differentiation should not rely on external sources. However, this also brings new pressures to supply chain companies: what if the customer becomes a competitor?

This complex relationship of cooperation and competition is a true reflection of the current original equipment manufacturer (OEM) ecosystem. Cooperation and competition are no longer either-or choices, but two forces that coexist and maintain a dynamic balance. Suppliers who can find their position and establish irreplaceability in this complex environment will have the opportunity to prevail in the next stage of competition.

There is still a long way to go from "platform" to "symbiosis".

Automotive suppliers collectively “appearing on stage” for a new vehicle launch is undoubtedly a clear sign of warming relations between OEMs and their suppliers. However, sharing the spotlight at a single launch event is far from genuine coexistence. Beneath the surface fanfare, longstanding issues in traditional OEM-supplier relationships remain unresolved, and new tensions are even beginning to emerge. The true transformation—from mere “stage appearances” to strategic collaboration—has only just begun.

In recent years, the relationship between and suppliers has indeed seen positive changes. More manufacturers have opened their R&D systems to core suppliers during the product definition phase, making joint development and early involvement the norm. In key technology areas such as autonomous driving and air suspension, suppliers are no longer just "following drawings" executors, but partners deeply involved in defining technical roadmaps.

Dong Yang, Chairman of the China Automotive Power Battery Industry Innovation Alliance, Co-Chairman of the China Automotive Chip Industry Innovation Strategy Alliance, and Vice Chairman of the China Electric Vehicle 100 Forum, recently pointed out that the automotive industry is currently experiencing major technological breakthroughs across multiple domains. A single vehicle manufacturer cannot possibly control and lead the development of so many technological fields. New technologies require collaborative refinement and integration between the technological side and the market-demand side to deliver mature applications and user experiences. Therefore, deep collaboration is essential. More importantly, new technologies are still undergoing continuous development, iteration, and upgrading; the relationship between supply and demand is no longer a simple buyer-seller transaction but requires long-term cooperation. This signifies that the relationship between OEMs and Tier 1 suppliers is inevitably shifting—from a “one-off transaction” to a “long-term partnership”—as a requirement of our times.

However, the other side of the coin is that the structural contradictions in the traditional whole-part relationship have not disappeared due to a few joint press conferences. The most typical and the most headache-inducing for supply chain companies is the issue of payment terms. In China's automotive industry, it is a long-standing unwritten rule for suppliers to have their payments withheld by vehicle manufacturers. Payment terms of 6 months, 9 months, or even longer, are standard at some vehicle manufacturers. The widespread use of acceptance bills further discounts the payments that suppliers receive.

To address this issue, the China Automobile Industry Association (CAAM) officially released the “Initiative on Standardizing Payment Terms for Suppliers of Automobile OEMs” in September 2025, stipulating clearly that payment terms for OEMs shall commence from the date of suppliers’ delivery and successful acceptance, with a maximum duration of 60 calendar days. According to a CAAM survey report released in February this year, the average payment term among 17 key automakers has decreased to 54 days.

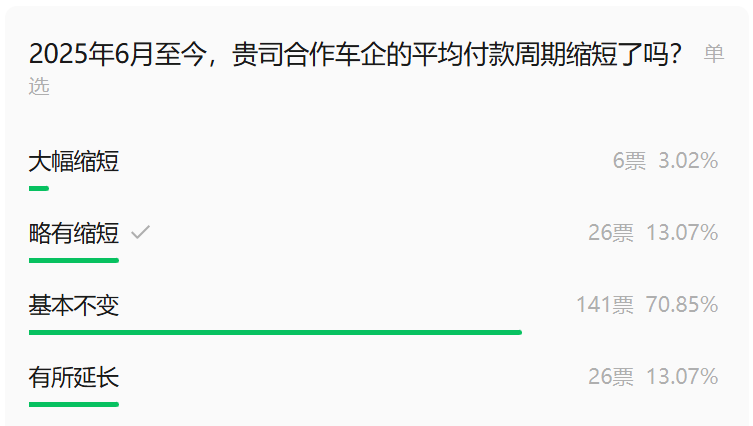

However, a significant gap remains between policy initiatives and industry reality. A survey conducted by Gasgoo shows that among approximately 200 respondents (note: this was an open poll, so multiple participants from the same company cannot be ruled out), only about 3% reported that their company's payment terms had "significantly shortened," while around 13% indicated "slight shortening." In stark contrast, as high as 70.85% of respondents stated that payment terms had "remained largely unchanged," and another 13% reported that terms had "somewhat lengthened." This suggests that, despite actions taken by some leading automakers, many suppliers have not experienced substantial relief from payment-term pressures in their actual operations. There remains a long way to go in translating "initiatives" into tangible outcomes, particularly regarding payment terms—a core issue in OEM-supplier relationships.

The root cause of the payment term issue lies in the power imbalance within the whole-to-fragment relationship. Major manufacturers hold the power to allocate orders, and suppliers, in order to retain their clients, often dare not "push back" on payment term issues. This structural dilemma cannot be solved by a single initiative. What is needed is a deepened industry consensus, optimized competition rules, and a mindset shift among manufacturers to truly regard suppliers as partners rather than tools.

Dong Yang particularly warned the industry to be cautious about the tendency of "full-stack self-research" and the neglect of partners. He pointed out that Tesla is not inherently inclined to full-stack self-research, but rather because traditional system suppliers could not meet its needs for technological advancement and the frequency of technological iteration. Tesla has always been seeking new system suppliers that can meet its requirements, and CATL is an important partner of it in the field of power batteries.

He emphasized that the "winner-takes-all" mindset from the internet industry is harmful to the automotive sector. Automobiles are long-cycle products; new technologies, structures, and features cannot maintain long-term monopolies. Moreover, vehicles have extremely high safety requirements, making them fundamentally different from certain internet products that can be iterated while in use. Therefore, automakers should maintain close, long-term collaboration with key partners rather than attempting to control everything themselves.

Restructuring the relationship between OEMs and suppliers cannot be achieved through just a few joint press conferences. Issues such as payment terms, technological rights, and price transmission mechanisms are tough challenges that require systemic solutions. Encouragingly, the industry has already recognized these problems. Some leading automakers have begun proactively optimizing their payment term management by shortening payment cycles, and others have established long-term strategic cooperation frameworks with key suppliers, committing to sustained collaboration across multiple vehicle platforms.

Platforms are beneficial and represent a starting point—but certainly not the end goal. In the second half of the “whole-vehicle–component” relationship, the real competition lies in who can demonstrate sincerity and offer practical solutions to genuine issues such as payment terms, technological rights, and profit distribution. Automakers willing to treat suppliers as true partners—not mere tools—will build the most robust supply chain moat in the next phase of competition.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Breakthrough! 13.6-million-ton new giant emerges as world’s fourth-largest polyolefin producer, reshaping industry landscape

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Saudi Core Petrochemical Zone Hit! Trump Issues "Final Deadline" Threat to Iran! Over 5 Million Tons of Production Capacity Halted in April

-

Vimar Launches Linea Switch Range Using Envalior Recycled Material, Cutting Carbon Footprint by Over 80%

-

Domestic PBE Breakthrough, Polyolefin Modification Industry to Break the Impasse