Breaking news! formosa petrochemical olefins division lifts force majeure! asia olefins supply and demand dynamics face another reversal

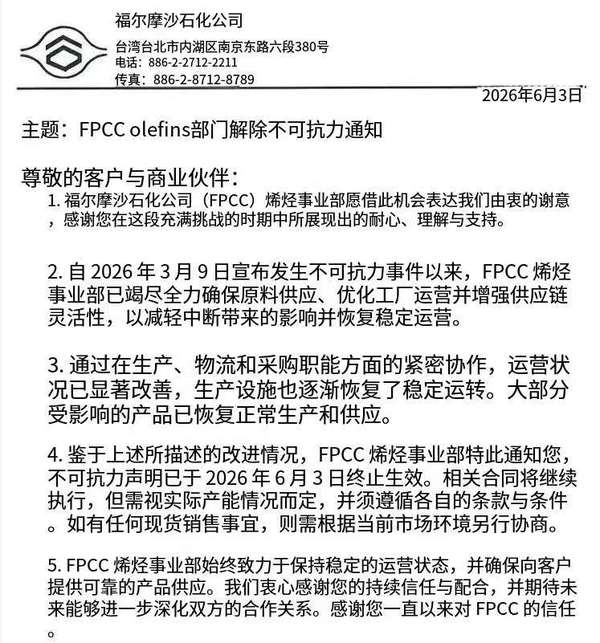

According to the latest news from Zhuansu Vision, Formosa Petrochemical’s Olefins Business Division has issued a notice lifting the force majeure and has resumed production.

As one of the core suppliers of olefins and plastic raw materials in Asia, Formosa Plastics' full resumption of operations will directly alter the supply pattern of ethylene, propylene, and downstream plastic raw materials in East Asia, significantly impacting the spot and futures markets of the entire PP, PE, and styrene industry chain.

1. Event Review

Formosa Petrochemical’s Mailiao olefins cracking unit officially declared force majeure on March 9, 2026. The trigger was the disruption of shipping through the Strait of Hormuz caused by geopolitical conflict in the Middle East, which interrupted arrivals of Middle Eastern naphtha (about two-thirds of Formosa’s naphtha imports depend on the Middle East). For details, see the previous report by Plastics Vision: “Can't Hold On! Middle East Crisis Cuts Off the Chemical Industry’s “Lifeline,” with Giants Including Wanhua, Formosa Plastics, and Dow Announcing Force Majeure in Quick Succession“Golden March and Silver April” Hit by the Strongest Force Majeure in History! 14 Plastics and Chemical Giants Issue Announcements, Global Plastics and Chemical Production Capacity Restricted, April Price Hike Wave Continues to Escalate。

Constrained capacity:Ethylene: 2.93 million tons/year; propylene: 2.43 million tons/year. The entire olefin cracking complex is operating at minimum load, with operating rates dropping to the 32%–50% range during peak periods.

Ripple effects:Formosa Plastics’ downstream PE, PP, PVC and styrene supply simultaneously triggered force majeure, while Asian olefins and plastics spot prices surged temporarily, tightening domestic supplies of imported materials.

II. Current Status of Production Recovery

With the Middle East shipping routes resuming navigation and naphtha cargoes arriving one after another, Formosa Petrochemical has officially lifted the force majeure clause on olefins, and the cracker units have begun phased production ramp-up, with full-capacity restart now in place.

Progress:In mid-to-late May, the load will be gradually ramped up, and by early June the entire olefins unit will resume full-capacity operation, with ethylene and propylene sales shipments returning to normal long-term contract fulfillment and spot market deliveries.

Supporting synchronization: Translate the above content into English and output only the translation result directly, without any explanation.The synchronous lifting of production restrictions on aromatic hydrocarbons (benzene, toluene, PX) and styrene units has alleviated the raw material shortage issue for Formosa Plastics' fibers.

III. Impact of Industrial Chain Prices

1. Ethylene/PE (LDPE/HDPE/LLDPE)

The increase in ethylene production in Asia has led to downward pressure on spot prices; Formosa Plastics' exports of PE have increased, and the influx of imported PE into the domestic market has suppressed the upward potential of domestic PE prices, causing high spot prices to gradually ease.

2. Propylene/PP

Incremental propylene supply in Asia, coupled with the concentrated restart of multiple domestic PDH units, has shifted propylene fundamentals from tight to loose. PP import supply has rebounded, weakening the upward momentum in spot prices, while the basis has gradually narrowed.

3. Styrene, EPS

Formosa Plastics' SM (Styrene) production capacity of 1.32 million tons/year is fully released, leading to a rapid narrowing of the supply gap for styrene in Asia. As a result, the cost of styrene and EPS has decreased, putting downward pressure on prices.

IV. Market Outlook

Negative main theme:Formosa Plastics, South Korea’s YNCC, and Singapore crackers have resumed production in a concentrated manner, shifting the Asian olefins market from “tight supply” into a cycle of ample supply, while the cost side (naphtha) has also declined, lowering costs across the entire value chain.

Supporting variables:Downstream rigid demand for plastics remains stable, and some domestic refining and chemical units are undergoing routine maintenance, limiting the room for a sharp price decline. Overall, the market is fluctuating with a weak bias.

Trade Changes:The arrival volume of imported Formosa feedstock in South China and East China has increased, and traders’ willingness to replenish imported supplies has improved, putting pressure on the price comparison of domestic materials.

Source: Formosa Plastics Group, ZHUAN PLASTICS VIEW, S&P Global Platts, OPIS, Zhuochuang Information, Longzhong Information, Jinlianchuan, Securities Star, Donghai Futures, and other publicly available information online.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped

-

Ethylene Industry Enters Production Boom Period! Multinational Giants and Domestic Leaders Compete in Trillion-Dollar Track

-

Breaking news! formosa petrochemical olefins division lifts force majeure! asia olefins supply and demand dynamics face another reversal

-

Target To Reduce Plastic By 30%! South Korea Enters Plastic Recycling Controversy, Involving National Interests