Domestic Sulfur Market Officially Enters the “10,000-Yuan Era”! Titanium Dioxide Forced to Follow Suit, Price Increase Letters Issued in Rapid Succession

As of June 15, the domestic sulfur market has officially entered the "ten-thousand yuan era." According to the latest industry data, the mainstream price of solid sulfur in Shandong has soared to 11,084 yuan/ton. At the beginning of June, the mainstream price of solid sulfur in Shandong was less than 8,000 yuan/ton, and in just over a week, the increase has exceeded 2,000 yuan!

Source: Business Society

Looking back to early 2026, the average domestic sulfur price was only around RMB 3,850 per ton; in just half a year, it has risen by more than 160%. And since the low point in the second half of 2024, the price has surged by nearly 600% in just one and a half years—this yellow granular material, once regarded as an “industrial byproduct,” is now experiencing its most dramatic rally in nearly a decade.

In early June, the sulfur market was changing almost by the day. Quotations for granular sulfur at Zhenjiang Port and Dafeng Port surged from RMB 7,450–7,500 per tonne on June 1 to RMB 8,400–8,500 per tonne on June 3, a two-day increase of nearly RMB 1,000, with the largest single-day rise reaching RMB 750 per tonne. By the morning of June 9, spot transaction prices in Shandong and many parts of East China had fully broken through the RMB 10,000-per-tonne mark.

Overseas sulfur prices have also risen in tandem. Abu Dhabi National Oil Company (ADNOC) has raised its official sulfur selling price for the Indian market in June to $860/ton (FOB Ruwais), an increase of $100/ton from May, setting a new all-time high.

The core reason for this round of sharp price increases is not a surge in demand, but simultaneous pressure on the supply side across three chains.

Overseas imports were disrupted: Following shipping disruptions in the Strait of Hormuz, China’s imports from the Middle East were almost completely cut off. From January to April 2026, arrivals of sulfur from the Middle East plunged 75% year-on-year.

Social inventories are nearly depleted: according to the latest monitoring, as of early June, total sulfur inventories at major domestic ports (such as Nanjing Port, Fangchenggang Port, and Zhenjiang Port) have approached the 900,000-ton red line.

Domestic source-directed supply assurance: major domestic refineries have launched a special “supply assurance” mechanism, prioritizing supplies to fertilizer producers, further intensifying the spot shortage of industrial sulfur.

Sulfur is a key raw material for the production of sulfuric acid, and the sulfate-process production of 1 ton of titanium dioxide requires 3.6 tons of sulfuric acid. Driven by the continued surge in sulfur prices, sulfuric acid prices have risen sharply, and this factor alone has caused a steep increase in titanium dioxide production costs. Under pressure from rising costs, titanium dioxide producers have begun to implement frequent price increases.

On June 5th, Longbai Group, a global leader, announced its fifth price increase since March of this year: an increase of 1,000 yuan/ton domestically and 150 USD/ton internationally. On the same day, Tianeng Chemical also announced an increase of 1,000 yuan/ton for domestic customers and 150 USD/ton for international customers, effective immediately. Shandong Xianghai Titanium Industry and Shandong Jinhai Titanium Industry, both under Lubek Chemical, also issued a notice to raise prices by 1,000 yuan/ton domestically and 150 USD/ton internationally.

On June 6, two more companies officially issued letters: Shandong Daon Titanium Industry announced that starting today, the domestic price of Daon brand titanium dioxide will increase by 1,000 yuan per ton, and the international price will increase by 150 dollars per ton; Qianjiang Fangyuan Titanium also announced that starting June 6, the domestic price of rutile titanium dioxide will rise by 1,000 yuan per ton, and the export price will rise by 150 dollars per ton.

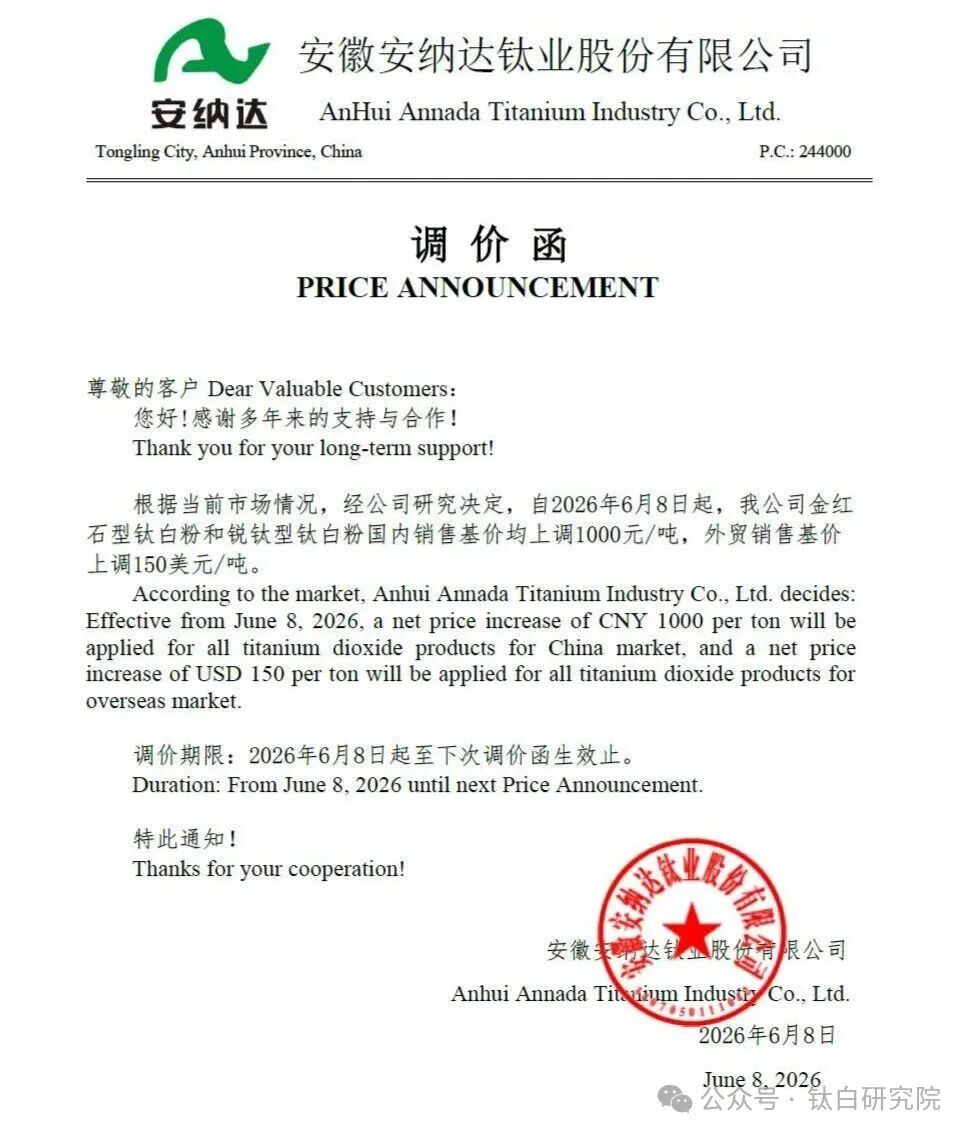

On June 8, Kunshan Kylin Technology announced another price increase: its TiOEX series titanium dioxide prices will rise by 1,000 yuan/ton in China and by 150 USD/ton internationally — the company’s second price hike this year. On the same day, Panzhihua Haifengxin Chemical Co., Ltd., Jiangsu Zhengtai Chemical Co., Ltd., and Anhui Annada Titanium Industry Co., Ltd. also successively issued price adjustment notices, each raising the domestic price of their titanium dioxide series by 1,000 yuan/ton. Among them, Zhengtai and Annada also increased their international prices by 150 USD/ton, while Haifengxin’s notice did not mention any international price increase.

On June 8, Inner Mongolia Guocheng Titanium Industry Co., Ltd. and Nanjing Titanium White Chemical Co., Ltd. also issued a notice: Guocheng Titanium Industry will increase the price of all models of titanium dioxide by 1,000 yuan/ton domestically and by 150 USD/ton internationally starting from this day; Nanjing Titanium White will increase the price of all models of rutile titanium dioxide by 1,000 yuan/ton domestically and by 150 USD/ton internationally starting from this day. Thus, the number of domestic companies issuing price increase notices on June 8 has exceeded six.

International giants are also making moves. On June 1, Chemours raised its Asia-Pacific prices by $250/ton, marking the third consecutive increase this year and bringing the cumulative rise to more than $650/ton; Germany’s Kronos also announced that, effective July 1, it will raise prices by another $325/ton for Asia, the Middle East, and Africa.

According to incomplete statistics, more than 20 titanium dioxide price increase notices have appeared in the market within just a few days.

However, a price increase notice does not necessarily translate into the actual transaction price. The latest data on June 8 showed that the benchmark price of titanium dioxide was only RMB 16,720 per ton, down 2.79% from RMB 17,200 per ton at the beginning of the month. This indicates that against the backdrop of weak end-user demand in sectors such as real estate, the actual pass-through effect of companies’ frequent price hike announcements has been greatly diminished.

Approximately 60% of titanium dioxide is used in coatings. As leading titanium dioxide producers have cumulatively announced price increases of more than RMB 4,500 per ton within six months, the coatings industry has become the main recipient of price pass-through. According to industry estimates, titanium dioxide accounts for as much as 20%–30% of raw material costs in coatings. Industry insiders report that frequent titanium dioxide price increase notices are expected to raise their costs by RMB 800–1,000 per ton.

Facing mounting pressure, many companies have already taken the lead in responding. Affected by the continued rise in upstream raw material prices, leading coating companies such as Nippon Paint, SKSHU, and Carpoly implemented intensive price increases starting in March 2026, with mainstream products seeing hikes generally ranging from 5% to 15%. Among them, SKSHU introduced multiple rounds of price adjustment plans in March and April, with the cumulative increase exceeding 10%.

Industry insiders warn that the sector must not misjudge the situation, as relying solely on price increases will make it difficult to fully offset the rise in raw material costs. Looking ahead, the autumn fertilizer stocking season in August and September will be the real decisive moment, when competition for sulfur resources between phosphate fertilizers and titanium dioxide will become intense. If end-market demand still fails to improve, the industry may face a genuine round of survival-driven reshuffling, with small and medium-sized enterprises lacking long-term raw material agreements and alternative process solutions being the first to come under pressure.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

A Look at the Material Suppliers Behind SpaceX

-

Nike mind: Neuroscience and Foam Material Innovation Merge to Lead Low-Carbon Upgrading Technology in the Footwear Industry

-

Research progress on surface modification of white carbon black and its applications

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped