Cost and Supply-Demand Convergence Drive Polyester Bottle Flake Market Higher in April

I. Key Focus Areas This Month

① Iran stated it will allow commercial vessels to pass through the Strait of Hormuz during the ceasefire window, alleviating the previously persistent risk of shipping disruptions and positively impacting the flow of imported raw materials.

② This month, the supply and demand situation for polyester bottle chips has become tighter, with industry processing fees continuously rising to around 1,500 yuan/ton. The industry's profitability has significantly improved, representing a substantial increase from the previously low processing fee levels.

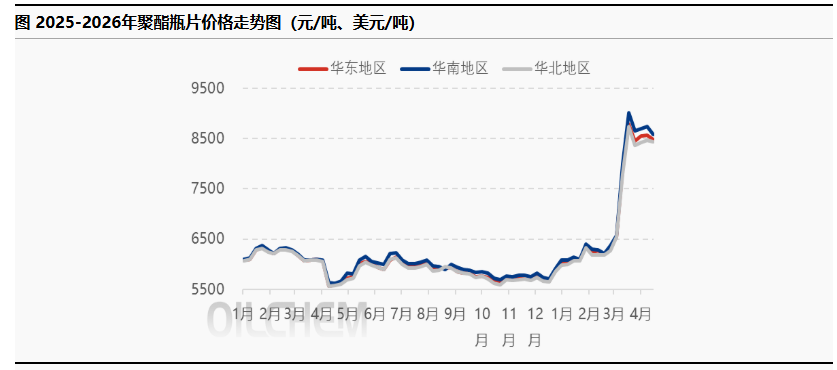

③ The monthly average price of polyester bottle chips in the East China region in April was 8609 yuan/ton, up 515 yuan/ton from the previous month, with a month-on-month increase of 6.38%, showing a steady upward trend.

II. Analysis of the Polyester Bottle Flakes Market This Month

The domestic polyester bottle resin market in April showed a "V"-shaped trend, with the monthly average price steadily rising. The overall average price for the month was 8,609 yuan/ton, an increase of 515 yuan/ton compared to the previous month, a rise of 6.38%. The mainstream price range remained between 8,300 and 8,900 yuan/ton. Looking at the performance of major domestic markets, the average price in the East China region in April was 8,609 yuan/ton, up 516 yuan/ton from 8,093 yuan/ton in March, an increase of 5.98%, and up 51.29% year-on-year compared to 5,690 yuan/ton in April 2025. The average price in the South China region in April was 8,719 yuan/ton, up 470 yuan/ton from 8,249 yuan/ton in March, an increase of 5.39%, and up 51.82% year-on-year. The average price in the North China region in April was 8,457 yuan/ton, up 432 yuan/ton from 8,025 yuan/ton in March, an increase of 5.10%, and up 48.94% year-on-year.

The upward trend in this month's market is mainly driven by cost support and the resonance of supply and demand. Geopolitically, the ongoing conflict between Iran and Israel has continued to escalate, causing disruptions in the passage through the Strait of Hormuz, leading to tight raw material supply. PX and PTA plants have undergone concentrated maintenance, further tightening the supply of raw materials and providing strong cost support for polyester bottle chip prices. On the supply side, constrained raw material availability and force majeure factors have limited industry supply increases, keeping overall supply stable. On the demand side, the traditional peak season has arrived, with downstream industries gradually recovering, maintaining a strong supply-demand structure. In summary, rising costs combined with the resonance of supply and demand have continuously improved the profit margin of the polyester bottle chip industry, resulting in a strong upward trend in the market in April.

III. Analysis of Upstream Situation

1) PTA: It is expected that the subsequent PTA market price will trend warmer. The negotiations between Iran and the US are expected to last for a considerable period, and the Strait of Hormuz continues to restrict shipping liquidity, prolonging the risk of crude oil supply. Domestic PTA supply is tightening due to extended US sanctions, reduced operating rates of refining and petrochemical enterprises, restrictions on upstream PX imports, and low industry profitability; at the same time, PTA processing fees are at a low level, with limited raw material supply, coupled with the polyester industry's inventory being relatively high and difficult to deplete. Overall, the geopolitical situation remains unstable, and the potential support from the cost side still exists. Currently, the supply of PX is tightening, and the PTA-PET industrial chain is showing a marginal destocking trend. Moving forward, it will be crucial to closely monitor the value transmission within the industry and the return of terminal demand.

Ethylene glycol: It is expected that the Chinese ethylene glycol market will maintain a high-range oscillation trend in May, with market focus concentrated on geopolitical issues and the performance of the downstream polyester industry. On the supply side, a few refining and petrochemical units are scheduled for maintenance in late May, while some units are expected to increase their operating rates. Coupled with the high operating rate expectation of coal-based units, the domestic ethylene glycol production is expected to gradually rise in May. In terms of imports, due to the navigational issues in the Strait of Hormuz, the import expectation is conservative, with the total import volume expected to be within 300,000 tons. The visible inventory at ports is expected to continue decreasing in May. On the demand side, downstream demand is sluggish, and market expectations for demand are relatively cautious. Moreover, if the navigational issues in the Strait of Hormuz ease, it will also have some impact on market sentiment. In summary, the ethylene glycol market in May will show a wide range of fluctuations, influenced by the combination of the inventory reduction support in the fundamentals, cautious demand, and geopolitical disturbances. The market transaction prices are expected to fluctuate within the range of 4,850 to 5,300 RMB/ton.

IV. Outlook for the Polyester Bottle Chip Market Next Month

Supply Forecast: In May, China's PET bottle flake industry has no clear plans for capacity changes. Attention should focus on the restart progress of previously shut-down units and new plant commissioning. The first phase of Hongze's 500,000-ton recycled polyester new materials project is scheduled to come online before June and will not affect the May supply landscape. The 1.5-million-ton-per-year PET packaging materials project by Fuhai (Shandong) Packaging Materials Co., Ltd. has been completed and is now contributing stable supply.

Demand Forecast: Polyester chip demand in May is expected to remain relatively strong, supported by a favorable export market outlook. On the domestic front, downstream soft drink industry operating rates are projected to stay around 80%–100%, soybean crushing plant operating rates may slightly rise to around 48%, and PET sheet industry operating rates are anticipated to range between 40% and 60%, collectively providing solid support to overall demand.

Price Outlook: The market for polyester chip is expected to see its center of gravity continue moving upward in May. Geopolitical tensions are anticipated to persist, with a potential blockade of the Strait of Hormuz exacerbating crude oil supply risks. On the raw material front, restricted PX imports and low industry profitability have tightened domestic supply, while multiple PTA units are scheduled for maintenance, providing strong cost support for polyester chip. Supply constraints stemming from raw material factors mean major producers currently have no clear plans for significant capacity increases. Downstream demand is in its peak season, with high operating rates in soft drink and sheet industries, further bolstered by robust overseas export demand. As a result, the polyester chip market is expected to trade in a high range in May, with prices potentially rising to RMB 8,900 per ton—up RMB 291 per ton or 3.27% month-over-month from April.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

First Time Surpassing $3 Billion! First Time Surpassing 100,000 Tons! Cathay Biotech’s 2025 Performance: Chemical Production Fully Phased Out, Biological Method Wins

-

$4 Billion! Medtronic Makes Another Acquisition

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range