Cost and demand both under pressure, polypropylene nationwide drawing price drops over 1500 yuan in one week, industry enters deep adjustment period

1. Market Overview: The national average price plunged 15.98%, with both spot and futures markets weakening simultaneously.

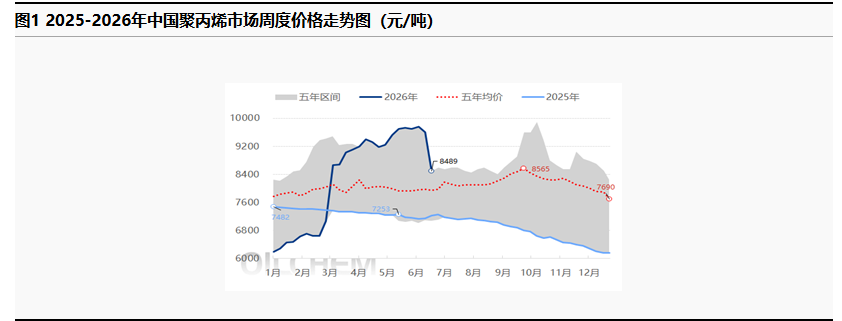

In mid-to-late June 2026, the domestic polypropylene market experienced a rare one-way sharp decline. According to data from Longzhong Information, as of June 25, the national average price of polypropylene raffia stood at CNY 8,021/ton, down sharply by CNY 1,525/ton from the previous week’s average, with a weekly decline of 15.98%. Spot prices across all product categories fell together.

National weighted average spot price: down 1,525 yuan/tonne week-on-week, a decline of 15.98%. The weighted statistical scope includes high- and low-priced cargoes across all regions nationwide, resulting in an overall decline significantly greater than short-term spot fluctuations in any single region.

Regional market divergence: single-day price adjustments in the East China and South China distribution markets were concentrated at 100–350 yuan/ton; after multiple consecutive rounds of cuts, cumulative declines for higher-priced grades exceeded 1,000 yuan; the downturn in the North China region was relatively milder, and regional price differentials continued to widen; petrochemical ex-factory single adjustment range: 100–350 yuan/ton.

Futures market: The PP2609 contract fell by more than 900 points over the week from June 19 to 25 (the futures figure refers to the decline in quoted futures points and differs in statistical scope from the national weighted average spot price, so there is no numerical conflict between the two). Bearish sentiment was released intensively, with both futures and spot markets weakening in tandem.

II. Two major bearish factors resonated, triggering this round of sharp PP decline

The geopolitical premium in the Middle East has rapidly dissipated, and the cost support for propylene has completely collapsed.

The terminal is deeply mired in the traditional off-season, with essential procurement nearly at a standstill.

Plastic woven bag industry: orders for agricultural supplies and food packaging have decreased significantly. Plastic woven bag factories are maintaining low-capacity production and have no plans to stock up in advance.

BOPP/CPP films: End-consumption orders have contracted, finished goods inventories have piled up at film producers, follow-up long-term orders are scarce, and raw material procurement volumes continue to shrink.

Nonwovens and hygiene materials: Rigid civilian demand remains stable with no new growth, while processors continue to draw down previous inventories, with very limited new raw material purchases.

Modified plastics, pipes, injection molding: Real estate and infrastructure have entered the traditional off-season, while end-market shipments of home appliances and daily necessities remain weak. Downstream factories are only making small purchases for rigid demand, with no bulk restocking activity.

III. Profitability across the entire industry chain has declined across the board, with mounting operating pressure at every stage.

Refining Production Sector: The decline in raw material propylene is slower than the price drop of polypropylene, resulting in a significant narrowing of processing profits for most oil-based refineries, with some coal-based enterprises facing temporary losses. Petrochemical companies are actively lowering prices to clear inventory and recover cash flow, showing a strong willingness to sell at low prices.

Intermediate trade segment: The early high-priced raw material inventory has depreciated sharply, speculative capital has exited the market in full, the spread between buying and selling prices continues to narrow, and there is no active replenishment demand in the market. Light positions and quick in-and-out trading have become the unified operating strategy among traders.

Downstream processing segment: the benefits of lower raw material costs cannot be passed on to downstream finished products. With fierce competition in the end-product market, finished product prices are unable to decline in step. Caught between upstream and downstream pressures, small and medium-sized processors are left with very thin profit margins, and some factories choose to reduce operating rates temporarily or halt production for short periods to avoid losses.

IV. Market Outlook: The short-term weak trend is unlikely to reverse, and a recovery rally will need to wait for the autumn restocking window.

International crude oil lacks strong upward momentum for now, the loose supply pattern of propylene continues, and polypropylene lacks rebound support from the cost side.

The traditional off-season cycle for plastics is expected to continue, and with the downstream peak stocking period in September–October still some time away, large-scale restocking is unlikely to materialize in the short term.

Source: Longzhong

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

Research progress on surface modification of white carbon black and its applications

-

Major Shake-Up! Latest China Auto Export Rankings Released

-

A Look at the Material Suppliers Behind SpaceX

-

Nike mind: Neuroscience and Foam Material Innovation Merge to Lead Low-Carbon Upgrading Technology in the Footwear Industry