Closed-Loop Recycling Takes Hold, and the High-End PMMA Market Enters an Era of Competition Among Industry Giants

When plastic recycling is no longer just a vision, but a viable business path, a whole new era of competition has begun.

For the high-end polymethyl methacrylate (PMMA) industry, this wave of change has moved from the shallows of technical validation into the deep waters of large-scale implementation. As chemical recycling technologies mature commercially, global chemical giants are increasingly saying goodbye to the “red ocean” battles of the commodity market and instead engaging in a higher-value “giant confrontation” centered on technological barriers, patent moats, and shares of the high-end market.

Unlocking the technical code of "single body circulation"

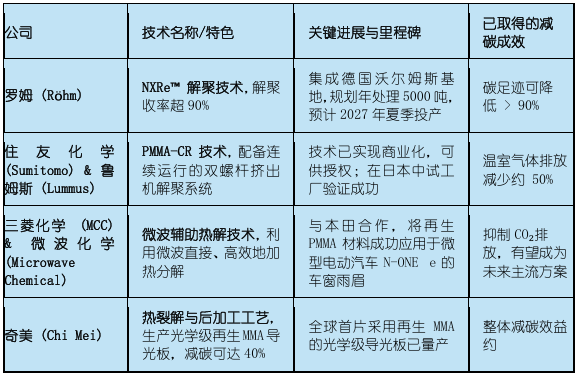

Overview of Mainstream Technology Pathways: At present, leading companies around the world have developed distinctive chemical recycling technology pathways, laying a solid foundation for commercial deployment. The main pathways are summarized as follows:

II. Clash of the Giants: A Business Contest Where Each Shows Their Strengths

1. Vertical Integration Path

This model aims to build a complete closed-loop value chain from recycling and processing to production, enabling control over the entire product lifecycle and cost optimization.

(1) Building cross-company alliances (with Röhm as a typical example): At the end of 2024, Röhm established the European PMMA Recycling Alliance and developed a clearly defined division of responsibilities:

The solvent-resistant PMMA tail light material jointly developed with Starry Universe Lighting (Source: Wanhua Chemical)

Wanhua Chemical: As a domestic industry leader, its subsidiary has planned to build a large-scale PMMA chemical recycling project, aiming to achieve a full industrial layout from raw materials to recycling and improve the circular economy system.

Advantages and Challenges: Vertical integration can build a strong value moat, effectively controlling costs and quality, and is suitable for high-end sectors such as automotive and electronics. However, this model requires substantial investment and heavily depends on a stable supply of high-quality scrap.

2. Technological Patentization and Licensing Pathways

Model advantages: This "light asset" model has lower investment risks and can quickly establish a presence globally.

Facing challenges: requiring companies to have highly disruptive and high-barrier technology patent moats.

3. High-Value Path of Special Materials

Image source: CHIMEI

III. The Chinese Market: A Leap from Scale Expansion to Value Restructuring

Four, dual drive of policies and markets.

Supply side: Reshaping the “new benchmark” for costs: Carbon footprint certification has become a “mandatory pass” for entering high-end markets such as the EU. The EU Packaging and Packaging Waste Regulation (PPWR) requires that packaging contain a minimum proportion of recycled materials by 2030; its draft End-of-Life Vehicles Regulation (ELVR) further proposes that, in the future, at least 20% of the plastics used in each vehicle must come from post-consumer recycled materials. Materials that fail to meet these standards may face high tariffs.

Demand side: High “green premium” from downstream brands: Demand upgrades from downstream brand owners are another major driver of change. Automakers such as Volkswagen and BMW, as well as consumer goods giants such as Coca-Cola and Unilever, have made the use of recycled materials and proof of their carbon footprint mandatory requirements for supply chain access.

V. Future Outlook: Where Are We Headed?

In summary, competition in the high-end PMMA industry has evolved from a simple contest of production capacity into a comprehensive race encompassing business models, core technologies, green concepts, and industrial ecosystems. The implementation of closed-loop recycling is not the industry's “ultimate answer,” but merely the opening of the door to a high-value, sustainable future.

This is a "qualifying round" entering the era of competition among giants. Ultimately, only those strategists who master core depolymerization technologies, have the capability to construct and efficiently operate closed-loop ecosystems, and can accurately meet downstream customers' demands for high-end, eco-friendly materials will succeed under the new rules of the game, leading the entire industry towards a more prosperous and sustainable future.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

【Overseas Highlights】Celanese Shuts Its Korean Engineering Plastics Plant! BASF to Divest Coatings Business; Six Japanese Corporations Tap Into Plastic Chemical Recycling

-

Global Chemical Giants Accelerate Production Capacity Restructuring, Dow and Celanese Optimize Global Industry Layout

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Gas Explosion Accident at Shanxi Tongzhou Group Liushenyu Coal Mine Results in 82 Deaths