13.3 Billion Bet on TDI/HDI! Jiangsu Eastern Shenghong, with a Debt Ratio of 82%, to Challenge Covestro and Wanhua Chemistry?

On the evening of April 10, 2026, an announcement from Dongfang Shenghong stirred up the polyurethane and high-end new materials sector: the third-level wholly-owned subsidiary, Lianyungang Hongke New Materials, signed an agreement with the Xuwei New Area Management Committee, planning to investRMB 13.33 billionLaunch of the Shangma Aromatics Industry Chain Quality Improvement and Efficiency Enhancement Project in One Go150,000 tons/year TDI, 50,000 tons/year HDI, 300,000 tons/year PC...along with 10 other core facilities, targeting the long-held strongholds of Wanhua Chemical and Covestro in isocyanates and engineering plastics.

Image source: Eastern Fortune

One side isDebt-to-asset ratio: 82.3%With just turning a profit and a tight financial situation, one side is a countercyclical investment of tens of billions in heavy assets, directly entering an oligopolistic market; the other side is the full-chain cost advantage brought by the integration of refining and petrochemicals. Meanwhile, the external pressures of soaring oil prices and intensifying competition within the industry are mounting. Is Oriental Shenghong's "tightrope walking" expansion a strategic move to secure its future, or a financial risk under high leverage? What kind of restructuring will this bring to China's polyurethane and PC industry landscapes?

I. Immediately after turning red, 13.3 billion was invested in three high-barrier tracks

Oriental Fortune's investment of 1 billion yuan is not a simple expansion, but a.Vertical Integration + High-end BreakthroughThe concentrated implementation. The project takes Xuhui New District in Lianyungang as the carrier, focusing on the aromatic chain to extend downstream, forming a "basic chemicals - isocyanate - engineering plastics" loop, directly targeting the three most profitable and high-barrier sectors in the industry.

1. TDI: Directly Enter the Oligopoly Battlefield, Challenge Wanhua's Global Dominance

TDI is a core raw material for polyurethane soft foam, coatings, and elastomers. The global market is highly concentrated: Wanhua Chemical holds a significant share.1.47 million tons/yearTotal production capacity firmly holds the top position, with a market share exceeding 40%; Covestro and BASF follow closely, forming an oligopoly.

Figure: WanHua TDI Product Series (Source: WanHua)

Dongfang Shenghong Development Plan150,000 tons/year TDIThough its scale is not even a fraction of that of Wanhua, it is sufficient to rank it among the top tier domestic suppliers and the seventh largest supplier globally. Relying on a 16 million ton per year integrated refining and petrochemical facility, Shenghong can achieve the "crude oil - PX - benzene - TDI" production chain.Full-chain self-sufficiencyRaw material cost advantages and plant synergy are significant, making it a key force in breaking foreign companies’ pricing power.

2. HDI: Entering the Blue Ocean Market, Betting on High-End Coatings Domestic Substitution

HDI (aliphatic diisocyanate) is a key raw material for high-end light-resistant coatings, automotive OEM paints, and wind power adhesives, which was long dominated by foreign companies such as Covestro and Kangrui. After Wanhua acquired Kangrui, its production capacity rose to the world's first. Meanwhile, companies like Merry Materials and Yangnong Chemical have also entered the market, with China's pending HDI production capacity exceeding that.500,000 tons, shifting from an importing country to an export powerhouse.

50,000 tons/year HDIAlthough not operating at maximum capacity, it synergizes with TDI and PC to target growth markets such as new energy vehicles, high-end equipment, and photovoltaic encapsulation, pursuing a "differentiated + integrated support" strategy to avoid low-end price competition and capture opportunities in the domestic substitution window.

3. PC: Break through high-end dependency and address the shortfall in engineering plastics.

There is an overcapacity of low-end polycarbonate (PC) production in China, butHigh-end optical grade, automotive modified, and electronic grade polycarbonateStill highly dependent on imports. After the Wanhua Chemical Fujian project goes into production, the capacity will reach12 million tons per year, leading the high-end market. Shenghong300,000 tons/year PCWith an annual self-sufficiency of 240,000 tons of bisphenol A, it is expected to rank among the top five domestically, and to establish the "bisphenol A-PC-modification" chain, thereby increasing the proportion of high-value-added products.

From the perspective of layout logic, Shenghong is not blindly expanding production, but rather focusing on the "olefins + aromatics" dual industrial chains, filling the gaps in isocyanate and engineering plastics, and building an "oil refining - new materials - terminal application" ecosystem, providing domestic raw material support for new energy and high-end manufacturing.

II. Expansion at an 82% Debt-to-Asset Ratio: The Tug-of-War Between Cash Flow and Debt at the Brink

Behind the ambition of billions lies Dongfang Shenghong.High debt, weak profitability, just turned profitableof the real fundamentals, this expansion is more like “dancing on the edge of a knife.”

As of the third quarter of 2025, Dongfang ShenghongTotal assets of 212.8 billion yuan, total liabilities of 175.1 billion yuan, debt-to-asset ratio of 82.3%With current liabilities exceeding 100 billion yuan, short-term loans of 55.8 billion yuan, and limited room for further borrowing.

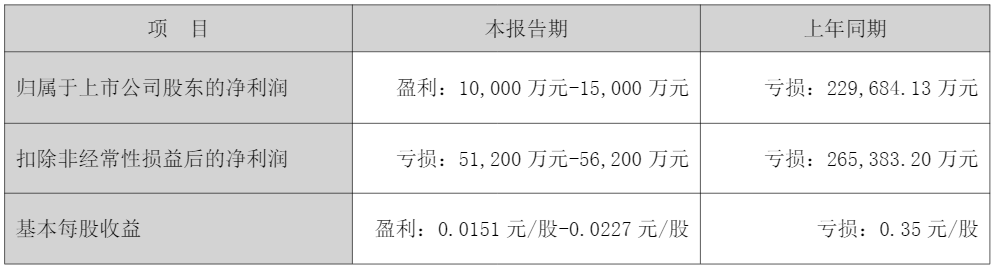

At the performance level, the company's estimated net profit attributable to the parent in 2025100 million to 150 million yuan, turning profitable year-over-year, but still reporting a loss in net profit excluding non-recurring gains and losses.RMB 512 million - RMB 562 millionThe core business has a weak profit foundation. The main way to turn losses into gains relies on the stable operation of refining and petrochemical projects and the benefits from declining crude oil prices, rather than a fundamental improvement in core competitiveness.

Figure: Eastern Silk 2025 Earnings Forecast (Figure source: Eastern Silk)

Figure: Eastern Silk 2025 Earnings Forecast (Figure source: Eastern Silk)

More troublingly, since early 2026, geopolitical conflicts in the Middle East have driven up oil prices, with Brent crude surging from $60 per barrel toAbove $95 per barrelMeanwhile, Shenghong’s cost advantage from its annual crude oil processing capacity of 16 million tons is rapidly eroding, further pressuring its profit outlook.

Short-term cash flow appears to be supported: Operating cash flow in Q3 20258.977 billion yuanSet a new historical high, but with the addition of a hundred billion new projects and a hundred billion ongoing engineering projects, the capital expenditure pressure has suddenly increased. More notably, the company explicitly stated in institutional investor visits that "Future capital expenditures will gradually decline, with no major new projects underway.”, abruptly reversing course in just two months and selling off consecutively within ten days13.33 billion + 3.455 billionTwo investments (Note: Shenghong Refining (Lianyungang), a wholly-owned subsidiary of Dongfang Shenghong, plans to invest approximately 3.455 billion yuan in the construction of a 2 million tons/year coking raw material pretreatment facility and related supporting facilities), totaling nearly 16.8 billion yuan, have sparked market concerns about the company's financial chain due to the strategic shift.

III. Why Shenghong Can Compete with Wanhua? Full-Chain Advantages and Late-Moving Opportunities

Even with full financial pressure, Dongfang Shenghong still has three cards to support its competition with Wanhua and Covestro in the TDI and HDI sectors.

1.Petrochemical Integration Platform: The Deepest Cost Moat

Shenghong owns16 million tons/year integrated refining and chemical complexwith self-sufficiency in key raw materials such as PX, benzene, propylene, and propylene oxide, and the capability to produce TDI, HDI, and PC.Self-supplied upstream raw materials, shared utility infrastructure, and minimized logistics costsCompared to companies that purchase pure benzene and toluene externally, Shenghong's cost advantage per ton can reach several hundred yuan, providing stronger risk resistance during a downturn in the cycle.

2. Global supply shift to the East: China's influence continues to grow

Europe's energy crisis has forced BASF and Covestro to phase out aging capacities, while Japan's Tosoh and others are gradually shutting down plants, leading to a reduction in global TDI and HDI supply.Accelerate eastward movementIn 2025, China’s TDI exports reached 556,500 tons, surging 51.83% year-on-year and filling the global supply gap. Shenghong’s entry into the market at this juncture coincides perfectly with the global supply restructuring window, enabling it to leverage China’s supply chain advantages to capture overseas market share.

3. Surge in High-End Demand: Domestic Substitution Opens New Growth Space

New energy vehicles, wind power, photovoltaics, and high-end equipment drive growth.Yellowing-resistant coatings, high-performance elastomers, engineering plasticsDemand is surging, with huge shortages in HDI, high-end PCs, and modified TDI products. Under the high-price monopoly of foreign capital, domestic high-quality production capacity has a strong impetus for substitution. Shenghong's entry into the high-end market aligns with the major trend of industrial upgrading.

However, the risks are also clear: TDI is already showing signs of overcapacity, and the HDI sector is seeing too many new entrants.Price wars, eroded profitsInevitable; at the technical level, the TDI phosgene process has extremely high safety and environmental protection requirements, and core catalysis and purification technologies for HDI still lag behind. Whether Shenghong can achieve stable production and compliance is the key challenge it faces.

IV. The Collective “Homogenization” Evolution of Large-Scale Petrochemical Complexes: What Will Be Competed in the Second Half?

The billion-yuan gamble of Eastern Fortune is not an isolated case.

Leading companies such as Wanhua, Rongsheng, Hengli, and Huarun Hengsheng are collectively moving from being leaders in a single segment to becoming all-round chemical giants with "refining + olefins + aromatics + new materials," following a highly similar path.

- Wanhua: MDI/TDI leader → expanding into PC, PMMA, POE, and lithium battery materials

- Rongsheng/Hengli: Petrochemical PTA → Expanding EVA, POE, and High-End Polyolefins

- Hualu Hengsheng: A leading coal chemical enterprise → expanding TDI, nylon, and biodegradable plastics

This “homogenized evolution” is inevitable for the industry: heavy and chemical industries must…Full industry chain vertical integrationonly then can a cost and supply moat be built; it is also a timely opportunity: domestic substitution and high-end upgrading open up a second growth curve.

But when all the giants "become like each other," the real test begins.is the key to victory.

For Eastern Shenghong, the RMB 13.3 billion investment is not the end, but a new starting point: Can the company leverage its refining and petrochemical advantages to gain a competitive edge in its products? Can it achieve breakthroughs in the TDI and HDI sectors?Can expansion and safety be balanced under high debt? This not only determines Shenghong’s future but also influences China’s global positioning in the polyurethane and polycarbonate industries.

V. Behind the High-Stakes Gamble: China National Chemical Corporation’s Breakthrough and Clarity

Dongfang ShenghongDebt ratio of over 82% + countercyclical investment of RMB 13.3 billion, seemingly radical, is in fact a collective choice made by China’s leading chemical enterprises: securing a foothold in high-end segments at the bottom of the cycle, leveraging integrated supply chain advantages to break foreign monopolies, and investing heavily in capital-intensive assets to secure long-term influence.

This game has no absolute losers or winners.

For the industry, Chinese enterprises' collective entry has accelerated the eastward shift of global pricing power for TDI, HDI, and PC, promoting the domestic substitution of high-end raw materials, which benefits downstream manufacturing in cost reduction and efficiency improvement.

For enterprises, high-leverage expansion is a double-edged sword: success propels them into the global top tier, while failure subjects them to dual pressures of cash flow strain and overcapacity.

Zhuan Su Shijie believes that the true value of Dongfang Shenghong lies in providing a sample for the industry:How can a large refining and chemical company transform towards high-end new materials? How can a highly indebted enterprise balance expansion with security? How can a cyclical enterprise navigate volatility and achieve value upgrading?

Over the next two to three years, the industry will enter a new phase as new TDI and HDI production capacities are concentratedly released.Capacity cleanup, technology competition, brand rivalrythe second half. Whoever transitions first from “scale leadership” to “value leadership,” and whoever identifies differentiation amid homogenization, will secure a dominant position in the next round of industry reshuffling.

Editor: Lily

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Middle East Tensions Escalate Again? U.S.-Iran Talks Collapse Before Starting, Crude Oil Volatility and Plastic Futures Retreat, Plastics Market Faces New Test

-

Saudi Core Petrochemical Zone Hit! Trump Issues "Final Deadline" Threat to Iran! Over 5 Million Tons of Production Capacity Halted in April

-

Magna Announces Sale Of Lighting And Roof Systems Business

-

Vimar Launches Linea Switch Range Using Envalior Recycled Material, Cutting Carbon Footprint by Over 80%

-

Mdi tariff slashed from 511% to 85%—can wanhua reenter u.s. market?