Trump has always taken the harshest sanctions measures against Iran. Since he took office, he has reinstated the "maximum pressure" policy on Iran, aiming to reduce Iran's oil exports to zero. Since the implementation of this policy, the U.S. Department of the Treasury's Office of Foreign Assets Control (OFAC) has imposed three rounds of sanctions on Iran, involving 23 Iranian oil tankers. In addition, the United States has also increased the intensity of sanctions on Russian oil exports, sanctioning a total of 155 oil tankers related to Russia.

As U.S. sanctions have intensified, tanker market freight rates have surged in recent months. However, the UK-based veteran shipping brokerage Gibson Shipbrokers recently questioned the notion that "sanctions will continue to drive up tanker freight rates": although the market's hope for large-scale sanctions after Trump took office seems to have been dashed, as only 23 Iran-related tankers have been involved in a total of three rounds of sanctions so far.

Therefore, the company believes that freight rates have returned to realistic levels, as the surge in freight rates in January did not increase with any further sanctions from the US, UK, and EU.

Maritime transport network shows strong adaptability

Gibson believes that, based on recent market performance, despite increased sanctions from the US, UK, and EU, the global crude oil transportation landscape still demonstrates rapid adaptability. Major importing countries such as India and China have already adjusted their procurement strategies, sought alternative supply sources, and continued to maintain crude oil imports amid price fluctuations.

The energy data service provider Vortexa also stated that recent changes in trading activities indicate that China and India have quickly responded to the widespread sanctions imposed on tankers carrying Russian crude oil.

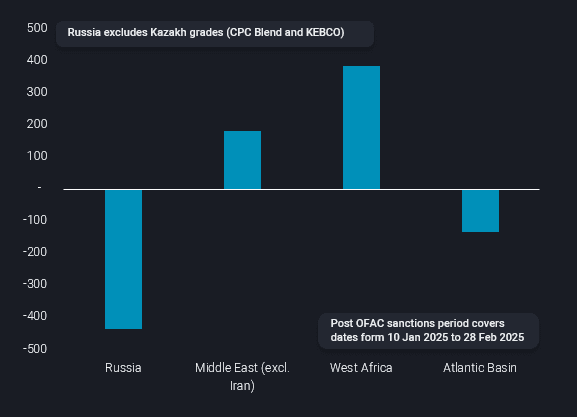

Vortexa believes: Since January 10, even taking into account seasonal slowdowns, Russia's crude oil exports to India and China (combined) have still slowed down. However, at the same time, exports from West Africa and the Middle East have picked up, and there are no signs of increased exports to India/China from other Atlantic Basin oil-producing countries.

Specifically, comparing the export volume of Russian-origin crude oil after the January 10 sanctions with the average export volume in 2024 shows a decrease of about 450 kbd. In contrast, exports from the Middle East (excluding Iran) increased by 200 kbd, but the most significant change was in West Africa, which saw a sharp increase in recent weeks, approximately double that of the Middle East.

OFAC sanctions on crude oil exports to China and India compared to the 2024 average, by origin (kbd)

From the perspective of India and China, the two major crude oil importers, although their imports from sanctioned countries have decreased, the import volumes of these two countries are becoming more diversified.

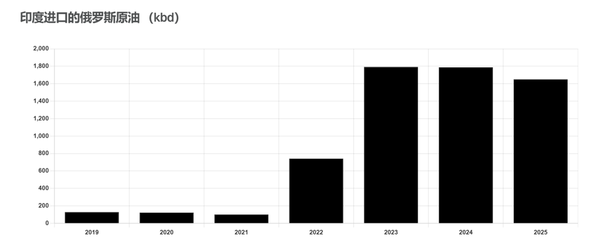

According to Gibson data, India, as one of the main importers of Russian crude oil, imported 200,000 barrels/day less in January compared to the 2024 average, and 300,000 barrels/day less in February. However, these reduced imports were supplemented by crude oil from West Africa and Latin America. Additionally, due to the price of Russian crude oil falling below the G7 cap of $65 per barrel, India's imports of Russian crude oil rebounded in March.

Votexa indicated that previously India was not a major buyer of Angolan crude oil in the West African region, but imports from there to India increased month-over-month in February, with imports from the Republic of Congo and Cameroon also increasing month-over-month.

Gibson stated that China's crude oil imports appear to have been more significantly affected, as the import volumes from Iran, Venezuela, and Russia in January and February were 800 and 900 kbd lower than the average for 2024. However, Gibson believes that these figures should be viewed with caution, as there was a noticeable decrease in crude oil imports from all sources into China in January, and the details of all crude oil imported in February have not yet been specified.

Vortexa indicates that the increase in China's crude oil imports from West Africa is primarily driven by an increase in exports from Angola to China. Post-sanction export volumes (January 10 to February 28) have exceeded the 700kbd threshold, thereby limiting exports to Atlantic Basin buyers (Spain, the Netherlands, Italy, and Brazil).

Gibson also stated that since March, China has been increasing its purchases from Iran, Venezuela, and Russia.

Whether it is China's tendency to import on a larger scale from long-term partners (Saudi Arabia and Iraq) or India's imports from multiple smaller suppliers (UAE, Kuwait, Oman, and Qatar), it undoubtedly indicates that the market may have found certain coping mechanisms.

Tanker freight rates rebounded and then fell back, with too much market uncertainty

Tanker freight rates are directly linked to fluctuations in crude oil export volumes. Gibson noted that tanker freight rates did indeed climb in January, with the Baltic Dirty Tanker Index surging from 799 on January 9 to 917 just 11 days later. On March 17, the index stood at 941, up 18 points from Friday.

In the fourth quarter, VLCCs, which did not see a typical seasonal improvement, also saw a significant increase in January. Data provided by the Baltic Exchange to Sinode Marine shows that the freight rate for Very Large Crude Carriers (VLCCs) soared from $23,000 per day at the beginning of the year to $57,000 per day, an increase of nearly 150%. It then fluctuated slightly, but the freight rate is currently still hovering around $40,000 per day.

Gibson stated that this rebound and the subsequent moderation in freight rates occurred under the sanctions of the United States, the United Kingdom, and the European Union. "This raises a question: Have oil flows returned to normal, or is the continued pressure from the U.S. on Iranian and Russian seaborne oil still having a long-term impact?" Although the sanctions had a temporary effect on shipping volumes, as trade flows found outlets, shipping volumes seemed to have returned to normal again.

The International Energy Agency (IEA) also issued a warning that new US tariffs could weaken global oil demand in 2025, further increasing uncertainty for the shipping industry. It is projected that global oil supply will exceed demand by 600,000 barrels per day, which may lead to a decrease in crude oil transportation and put downward pressure on freight rates. Furthermore, high-profile tariffs imposed by the US on China, Canada, and Mexico might trigger a macroeconomic slowdown, reduce industrial activity, and thereby limit the demand for oil transportation.

On the other hand, OPEC+ plans to gradually phase out voluntary production cuts, which may increase crude oil shipments, but the implementation by member countries remains uncertain. Meanwhile, an increase in production from the Tengiz oil field in Kazakhstan has boosted global oil supply, and a downgrade in production forecasts for Venezuela due to Chevron losing relevant permits could lead to a supply tightening and impact shipping routes in the South American region.

Overall, although the tanker market is adapting to the sanction environment and showing a certain degree of resilience, the future still depends on changes in policies of various countries, the market's reaction to new sanctions, and how sanctioned countries adjust their export strategies. Global oil transportation may have returned to a certain degree of normalcy, but this "new normal" remains full of uncertainties.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.