U.S.-Iran Tensions: Why Polypropylene Is Harder Than Polyethylene

Amid U.S. airstrikes on targets inside Iran and soaring shipping insurance rates in the Strait of Hormuz, polypropylene (PP) prices have surpassed those of polyethylene (PE), despite PE having higher import volumes. While this may seem counterintuitive at first glance, it actually reveals the starkly different vulnerabilities of the two supply chains in the face of geopolitical risks.

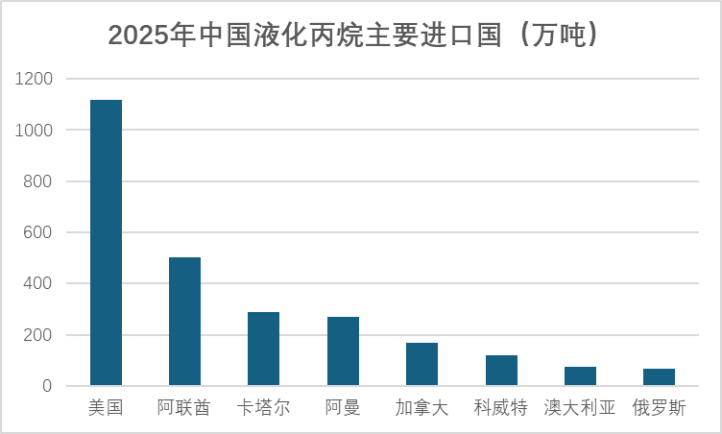

The key is not in the finished product, but in the raw materials. Although China imports over 12 million tons of PE annually, its main sources - the UAE, Saudi Arabia, and the US - are currently not directly impacted, and the Middle East has ample PE production capacity, making it highly substitutable. In contrast, nearly 40% of PP relies on the PDH (propane dehydrogenation) process, and propane is highly concentrated in Middle Eastern supply, with Qatar, the UAE, and Iran together accounting for over 70% of China's imports. With the intensification of US-Iran tensions, although Iran is not a major propane exporter, as a country along the Strait of Hormuz, any escalation in the situation will increase regional shipping risks and insurance costs; more critically, Qatar recently suspended part of its natural gas production due to a malfunction at its North Field, leading to a tightening of global LPG (liquefied petroleum gas) supply, with propane prices soaring nearly 30% in two weeks, and the price for delivery to Northeast Asia exceeding $620 per ton.

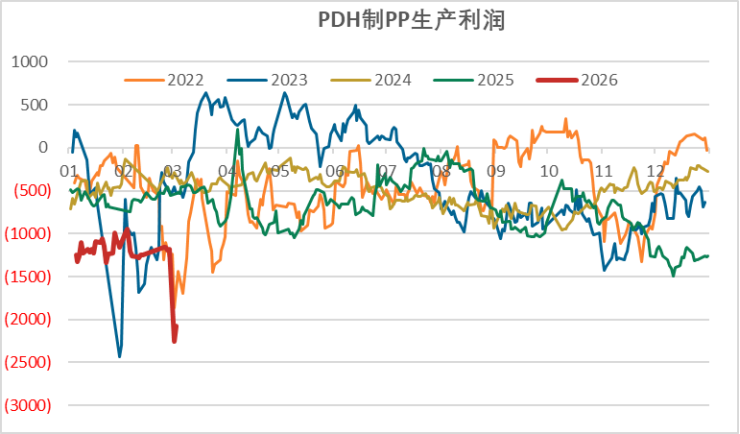

This directly impacts PDH plants: on one hand, the surge in raw material costs has driven theoretical profits below -2,000 yuan/ton; on the other hand, delays in long-term contract deliveries and difficulties in spot procurement have forced many companies to reduce their operating loads. According to Longzhong data, the PDH operating rate has plummeted from 82% to 68%, with no prospects of recovery in sight.

In contrast, PE feedstock sources are diversified—naphtha cracking tracks oil prices (currently stable), coal-based routes face no supply disruption risks, and import disruptions are offset by supplies from Southeast Asia and the Americas. Therefore, while PP faces dual pressures of "feedstock supply disruption + cost collapse," PE supply remains secure, giving PP stronger support due to expected production cuts.

The US-Iran conflict remains unresolved, and the Strait of Hormuz is still the global energy bottleneck. As long as the propylene supply chain in the Middle East faces pressure, PDH units will struggle to operate at full capacity, and the strong position of PP over PE is likely to continue. This price divergence ignited by the regional powder keg once again proves: in the chemical market, whoever's lifeline is in others' hands will be the most afraid of a single gunshot.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Middle East Tension Spikes Global Energy Pattern, Crude Oil and Plastic Industries Face Multiple Challenges

-

Middle East Tensions Escalate Sharply: How Polyolefins Respond Amid Soaring Risk Premium

-

Middle East Polymer Export Hub Hit in Sudden Attack, Global Supply Chain Sounds Alarm

-

[Forward-Looking Analysis] Impact of Escalating U.S.-Iran Tensions on Domestic Chemical Market

-

Futures Surge Violently, Polyolefin Spot Prices Rise Sharply in Tandem