Polypropylene: Short-term bottom support exists, but medium to long-term pressure remains

In March, insufficient cost support and weak supply and demand continued to pressure the market, leading to a weak performance in the domestic PP market. However, as multiple facilities entered maintenance in the second half of the month, the pressure on the supply side was being alleviated, coupled with seasonal rigid demand support, strengthening short-term market support. In the long term, however, the pressure from new capacity additions and expectations of seasonal weakening in demand weighed on the market, leaving market operation pressure unabated.

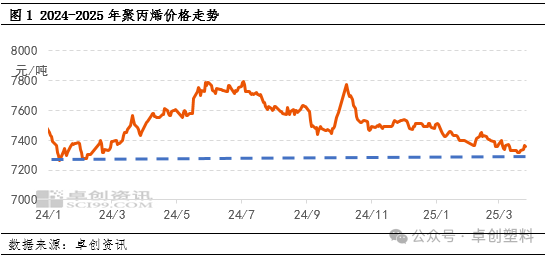

March: Insufficient cost support combined with weak supply and demand leads to a downward shift in the price center.

In the first half of March, the international crude oil market showed weakness, weakening cost support. At the same time, some facilities that had been under maintenance gradually resumed production, increasing market supply pressure and dampening market sentiment, leading to a continuous softening of PP prices. In the second half of the month, in order to meet monthly sales targets, traders adopted aggressive price-cutting strategies, keeping the market under pressure. Additionally, weak overseas demand coupled with expectations of rising shipping costs weakened the trading atmosphere in the export market, further undermining market confidence. However, as several domestic facilities entered maintenance, production volumes decreased significantly month-on-month, with operating rates for major categories such as homopolymer injection molding, and low melt fiber reaching relatively low levels, easing market supply pressure. Moreover, as prices reached the lowest levels of the year, downside support began to strengthen, leading to a slightly warming price trend by the end of the month.

Market Outlook: Short-term may be relatively strong with fluctuations, long-term operating pressure still exists.

For the short-term outlook, analysts believe that the PP market will have strong bottom support and may remain in a relatively oscillating situation. On one hand, the market is gradually entering the spring maintenance season, and as maintenance work progresses steadily, it will help alleviate supply pressure in the market. On the other hand, the current operating load of downstream industries is at a relatively high level for the first half of the year, and seasonal rigid demand will continue to provide support for the market.

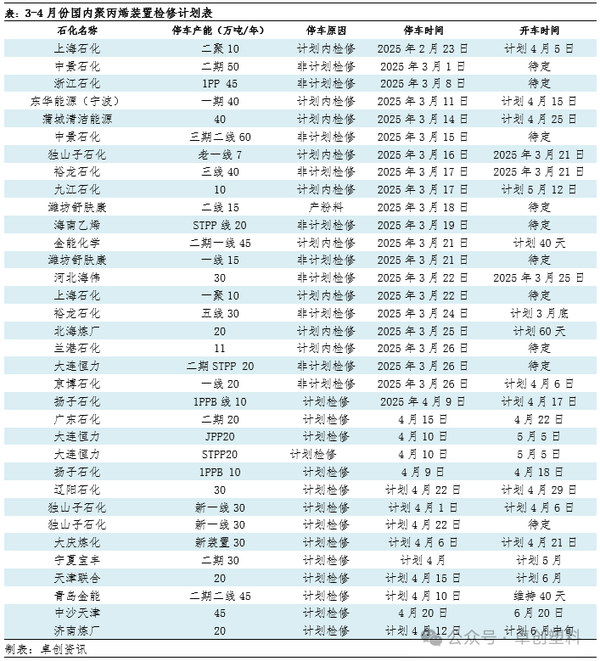

Supply: Continuous Increase in Maintenance Facilities to Help Alleviate Supply Pressure

Since mid-March, the number of polypropylene plant maintenance shutdowns has significantly increased, leading to a continuous reduction in market supply. According to data statistics, due to the rise in maintenance shutdowns, domestic polypropylene production last week decreased by 6.44% compared to the previous week, and it is expected that production will continue to decline this week. Looking at April, the maintenance situation in the polypropylene market has not eased. In addition to the existing maintenance shutdowns, multiple plants such as Yangzi Petrochemical, Sinopec SABIC Tianjin, and the second phase of Jinneng Chemical will also join the maintenance lineup. Therefore, it is anticipated that the production loss caused by maintenance in April will continue to increase, potentially further alleviating market supply pressure.

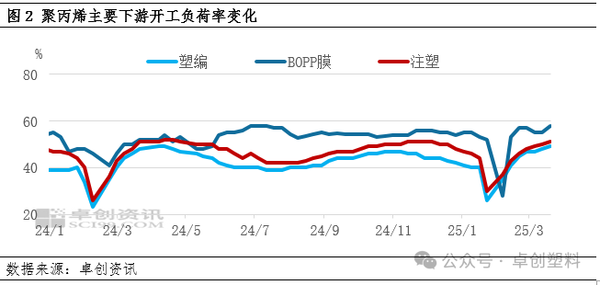

Requirement: Downstream long-term orders are weak, but currently in a seasonally strong demand period.

Since the Spring Festival, the trend in new orders for major downstream sectors of polypropylene (PP) has been relatively weak, especially long-term orders have not performed well. Coupled with poor profit conditions for downstream businesses and the gradual arrival of pre-hedged resources before the festival, there is insufficient motivation for enterprises to replenish stocks. However, as operating rates gradually rise to relatively high levels, demand for polypropylene has entered a seasonally favorable period in the first half of the year. It is expected that by late April to mid-May, seasonal basic demand will continue to provide support. Additionally, polypropylene prices have fallen back to the low point in early February last year, and the relatively low absolute price will also provide some bottom-level support for the market.

Overall, the short-term supply and demand contradiction for polypropylene is unlikely to significantly widen, and given that prices are not excessively high, there is support at the lower end. It is expected that the market may remain in a moderately strong oscillation in the near term.

From a medium-term perspective, the polypropylene market will still face pressure from supply and demand. On one hand, there are multiple new capacity addition plans in the second quarter, such as Inner Mongolia Baofeng (500,000 tons/year), ExxonMobil PP facility (955,000 tons/year), and Zhenhai Refining and Chemical PP facility (500,000 tons/year). The addition of these new capacities is expected to increase year-over-year production, intensifying supply pressure. On the other hand, considering seasonal factors, demand from some downstream industries may weaken after April, and it is necessary to closely monitor the new order conditions of downstream enterprises. Additionally, based on the seasonal performance of polypropylene exports, exports are expected to decline in April-June, especially in May and June. Moreover, weak overseas demand and the instability of freight costs will also reduce the support for the export market.

Overall, in the short term, the fundamental pressure in the polypropylene market is not significant, and the price still has certain bottom support. However, from a long-term perspective, fundamental pressure still exists. If planned new capacity is released as scheduled, the supply pressure will increase; coupled with the possible seasonal weakening of downstream demand and limited export support, these factors will jointly exert pressure on the market. Therefore, in the long run, the polypropylene market will still face pressure.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift