Polyester tariffs surge over 90%! eu-china trade war escalates

Since the beginning of 2026, trade frictions between China and the EU have intensified markedly. Within just a few months, the EU has launched a series of trade remedy investigations against China, placing the textile and apparel industry at the center of this storm.

Nylon filament exports are the first to be hit.

On March 27, 2026, the European Commission announced a preliminary anti-dumping ruling concerning polyamide yarns originating from China. It provisionally determined that the anti-dumping duty rate for Fujian Yongrong Jinjiang Co., Ltd., Fujian Jingfeng Technology Co., Ltd., Fujian Xinchuan Nylon Industry Co., Ltd., and Fujian Jinyuan High Performance Materials Co., Ltd. is 57.7%. The provisional anti-dumping duty rate for Fujian Hengshen Chemical Fiber Technology Co., Ltd., Fuzhou Liyuan Nylon Industry Co., Ltd., Fujian Liheng Nylon Industry Co., Ltd., Xinhui Dehua Nylon Chips Co., Ltd., and Nanchong Meihua Nylon Co., Ltd. is 90.1%. The provisional anti-dumping duty rate for other cooperating companies (see original text for details) is 67.1%, and for other Chinese companies, the provisional anti-dumping duty is 90.1%. The investigation period for dumping is from July 1, 2024, to June 30, 2025, and the investigation period for injury is from January 1, 2022, to the end of the dumping investigation period. (Data sourced from the European Commission website)

Polyester nonwoven fabric exports suffer a setback

On May 13, 2026, the European Commission announced a provisional anti-dumping determination on PET spunbond nonwoven fabrics originating in China. The Commission preliminarily determined that the provisional anti-dumping duty rate for Hubei Youbu Nonwoven Fabric Co., Ltd. is 45.6%; for Changde Tiendingfeng Nonwoven Co., Ltd. and Tiendingfeng Nonwoven Co., Ltd., 50.0%; for other cooperating companies, 49.4%; and for other Chinese companies, 50.0%. The dumping investigation period in this case was from July 1, 2024 to June 30, 2025, and the injury investigation period was from January 1, 2022 to the end of the dumping investigation period. (Source: European Commission website)

From nylon filament yarn to polyester nonwoven fabrics, the European Union has erected high tariff barriers on the grounds of anti-dumping, with duties on some products exceeding 90%, in an apparent attempt to precisely target key links in China’s textile industry chain. This series of measures has subjected China’s textile and apparel industry to its most severe test in international markets in recent years. At the same time, exports of polyester filament yarn and related textile and apparel products have also been significantly impacted, with problems such as order losses and rising costs becoming increasingly prominent, leaving the industry as a whole under considerable pressure.

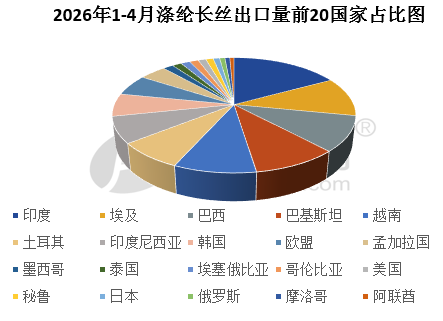

Data source: China Customs

From January to April 2026, the EU accounted for 5.51% of China’s polyester filament exports, ranking ninth among export destinations. Although this share may appear modest, the EU, as one of the world’s major textile consumption markets, still has a significant impact on China’s polyester filament exports through fluctuations in its demand.

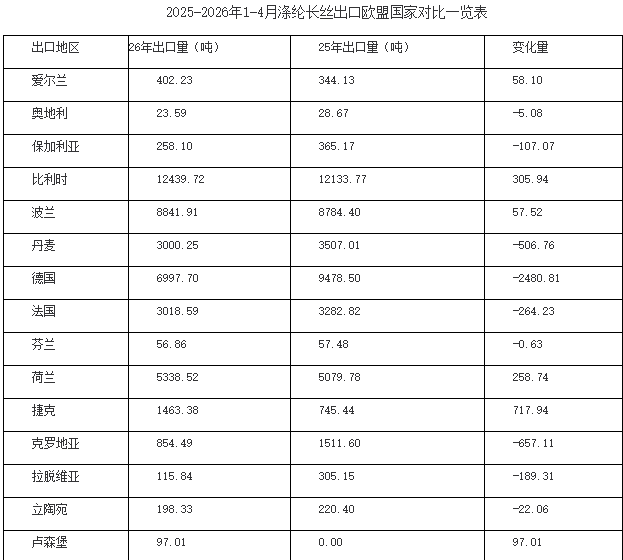

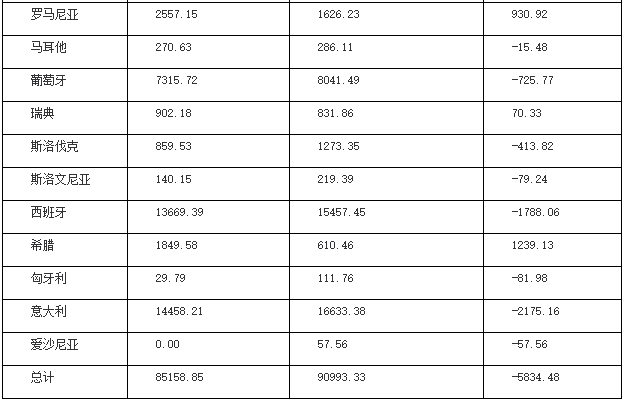

Data source: China Customs

In 2025 and from January to April 2026, China’s exports of polyester filament yarn to the EU showed a downward trend in both volume and price. From January to April 2025, China exported a total of 90,993.33 tons of polyester filament yarn to the EU, with a total export value of USD 121.7001 million and an average price of USD 1,377.46 per ton, down slightly by 1.84% from the same period of the previous year. In terms of distribution among member states, Italy was the largest export market, with export volume reaching 16,633.38 tons, accounting for 18.28%; Spain followed, with exports of 15,457.45 tons, accounting for 16.99%; Belgium ranked third, with exports of 12,133.77 tons, accounting for 13.33%.

Entering 2026, the export scale further contracted. From January to April, the cumulative exports to the European Union reached 85,158.85 tons, a year-on-year decrease of 6.41%; the total export value was 11,842.25 million USD; the average price slightly rebounded to 1,390.61 USD/ton, but still decreased by 6.41% year-on-year. The member state pattern saw slight adjustments: Italy remained in the top position with an export volume of 14,458.21 tons, with its share dropping to 16.98%; Spain exported 13,669.39 tons, with a share of 16.05%; Belgium exported 12,439.72 tons, with its share increasing to 14.61%. Overall, the ranking of the top three destination countries remained stable, but both Italy and Spain experienced declines in export volume and share, while Belgium's share increased against the trend. A comparison of data from the past two years shows that market demand in the EU continues to weaken, coupled with trade frictions and the impact of the off-season in the industry, China's exports of polyester filament to the EU are facing significant downward pressure.

Source: China Customs

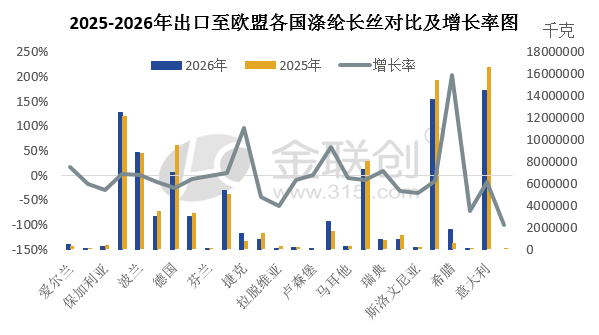

Compared with the same period in 2025, China’s exports of polyester filament yarn to the EU showed a significant divergence from January to April 2026. Among the 27 member states, only eight countries achieved positive growth. Greece recorded the most notable increase, reaching 202.98%; the Czech Republic followed with growth of 96.31%; and Romania ranked third, up 57.24%. Meanwhile, export volumes to the remaining 19 countries declined to varying degrees. Estonia posted the largest drop, down 100.00%, meaning there were no exports to the country this year; Hungary followed with a year-on-year decline of 73.35%; and Latvia ranked third, down 62.04%. Overall, demand expanded against the trend in a small number of countries, while import demand in most EU member states contracted significantly.

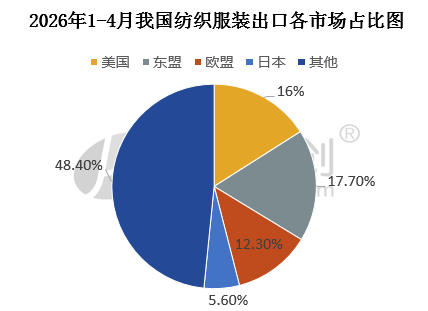

Data source: JLC

From January to April 2026, among China’s textile and apparel export markets, ASEAN was the largest destination, accounting for 17.7% of total textile and apparel exports. The United States ranked second, with a share of 16%, followed by the European Union at 12.3% and Japan at 5.6%. An escalation of the EU’s trade war against China would directly impact China’s textile exports. On the one hand, tariffs and non-tariff barriers—such as additional tariffs on cotton textiles and chemical fibers—would push up selling prices in Europe. If tariffs rise from 5% to 15%, corporate profit margins could be compressed by 10–15 percentage points. On the other hand, the environmental standards under the EU’s “Green New Deal,” such as requirements for biodegradable materials and carbon footprint certification, would increase compliance costs for enterprises and could lead to order losses in the short term. ASEAN, benefiting from low tariffs under RCEP and geographical proximity, has become a core alternative market, accounting for 48.4%, though vigilance is needed against low-end competition from countries such as Vietnam and Bangladesh. The U.S. market, with a 16% share, remains affected by uncertainties stemming from China-U.S. frictions, but demand for high-end textiles still holds potential.

Source: China Customs

From January to April 2026, China’s textile and apparel exports totaled US$91.13 billion, up 0.8% year on year, with the growth rate down 0.4 percentage points from the first quarter. Among them, textile exports reached US$46.896 billion, up 2.3% year on year; apparel exports totaled US$44.23 billion, down 0.9% year on year. In April alone, China’s textile and apparel exports to the world reached US$24.05 billion, surging 44.62% month on month and down 0.58% year on year, with the decline narrowing significantly from March. Among them, textile exports stood at US$12.71 billion, up 1.0% year on year; apparel exports amounted to US$11.35 billion, down 2.2% year on year.

Affected by the EU’s imposition of anti-dumping duties of up to 90.1% on nylon products, domestic nylon enterprises, represented by those in Fujian, have seen a significant decline in export orders and lost their price advantage. Production capacity originally destined for the European market has been forced to return to the domestic market, intensifying homogeneous competition and continuously narrowing profit margins. Although orders from the EU market have declined, some regions in Southeast Asia, South Asia, and Africa still show positive prospects; domestic sales, however, remain weak due to sluggish end-market demand.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

Lantiche Group To Shut Down Italian Adipic Acid Production Plant

-

Resin Market Trends Diverge: Buyers' Bargaining Advantage Hit by Geopolitical Uncertainty

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!