In the second quarter, concentrated maintenance of polypropylene facilities alleviates supply-side pressure.

lead-inShort-term supply-side reduction trend, mainly due to the concentrated maintenance of units such as Jinneng Chemical's second line and Maoming Petrochemical's second line, leading to a future supply-side reduction situation. In the second quarter, with the concentrated maintenance of units, the supply-side pressure may ease.

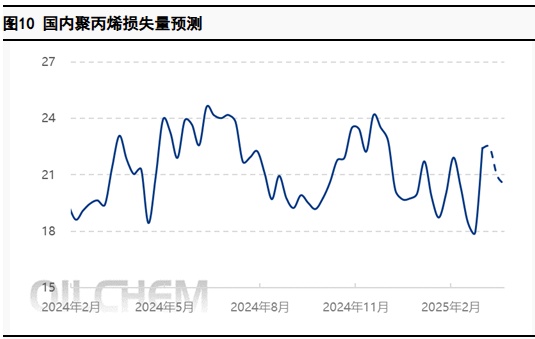

I. Polypropylene loss data trend stability analysis

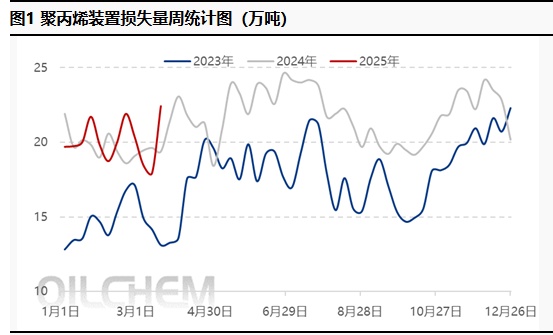

3.1 Conventional Data Analysis of Polypropylene Loss Quantity

As of March 20, 2025, the loss of polypropylene (PP) plant capacity in China was 224,270 tons, an increase of 25.10% from the previous week; among which, the loss due to maintenance was 159,840 tons, an increase of 60.43% from the previous week; the loss due to reduced load was 64,430 tons, a decrease of 19.24% from the previous week. Due to unexpected shutdowns of some large plants such as Zhongjing Petrochemical, and planned maintenance of plants like Pucheng Clean Energy, the domestic maintenance loss exceeded expectations. Affected by the widespread shutdowns, some plants with low operating loads have transitioned to a shutdown state, resulting in a slight increase in the loss due to reduced load for domestic polypropylene plants.

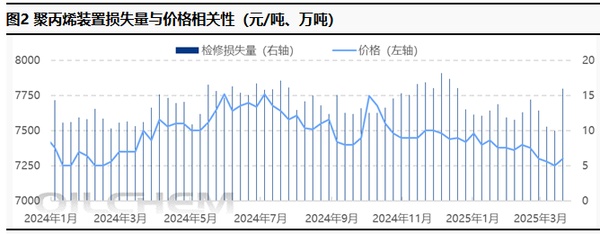

3.2 Loss Quantity Data Price Correlation Analysis

The weekly maintenance loss of polypropylene facilities in China increased by 60.43% week-over-week and 42.35% year-over-year. The maintenance volume of polypropylene facilities in China has hit a new high for the year, 60.43% higher than the lowest point of the year. The surge in maintenance losses of domestic polypropylene facilities has strengthened market support, leading to a significant rebound in market prices.

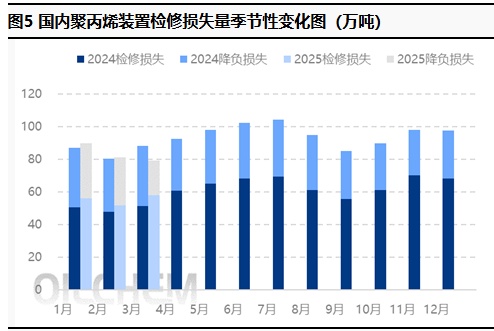

II. Seasonal Variation Analysis of Domestic Plant Losses

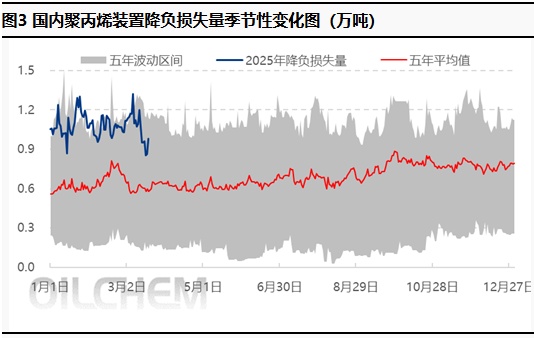

2.1 Seasonal Changes in Load Reduction Vectors

From the perspective of load reduction loss, as more polypropylene units are shut down and some units with low load enter a shutdown state, the load reduction loss of domestic production enterprises has rapidly declined and then experienced a slight rebound. In the future, as maintenance plans for the units gradually increase, the weekly load reduction loss may still have the possibility of fluctuating and declining.

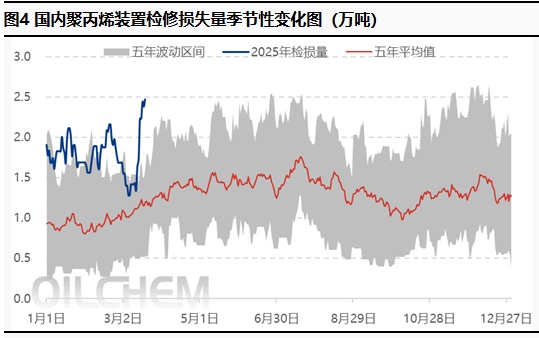

2.2 Seasonal Changes in Maintenance Loss Quantity

In late March, the peak consumption did not unfold as expected, and some production enterprises faced significant inventory pressure, leading to an increased willingness for maintenance. Additionally, unexpected shutdowns of some large facilities resulted in a greater-than-expected increase in maintenance losses. By March 20th, domestic maintenance losses had risen significantly, with the maintenance peak season slightly ahead of previous years.

2.3 Seasonal Changes in Monthly Losses of Domestic Polypropylene Plants

As of March 20th, based on the maintenance data currently available, it is estimated that the loss of domestic polypropylene facilities in March will be around 850,000 tons, with maintenance losses at 578,550 tons, an increase of 12.28% month-over-month and a 12.77% increase year-over-year.

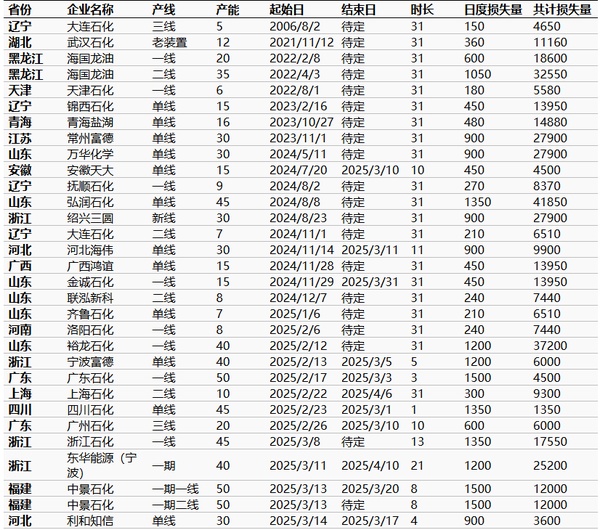

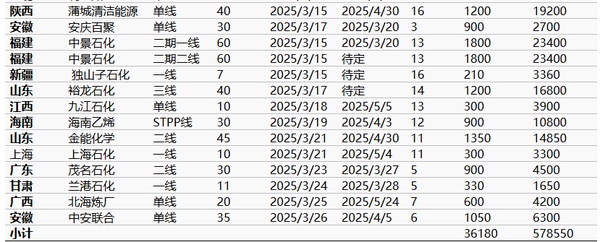

III. Details of Domestic Polypropylene Plant Maintenance

3.1 Domestic Polypropylene Maintenance Details for the Month

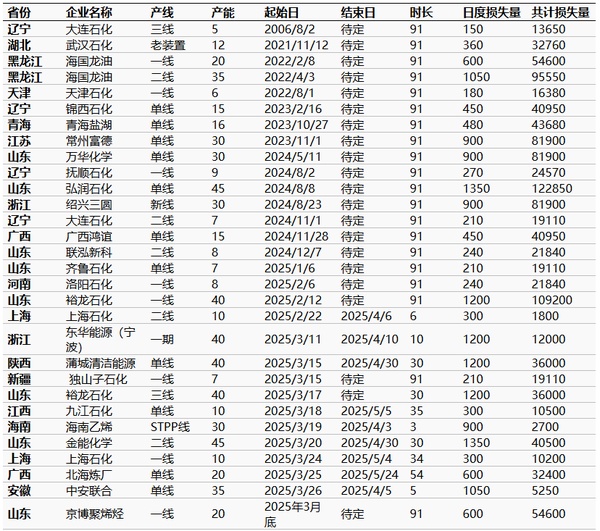

Table 1 March Domestic Polypropylene Plant Maintenance Statistics Table

unit: ten thousand tons/year, day, ton

In March, newly added parking facilities include Zhongjing Petrochemical, Yulong Petrochemical, Jinneng Chemical, and Pucheng Clean Energy. Restarted facilities include Lihe Zhixin, Ningbo福德化工和广州石化三线等。新增检修装置较多,装置检修集中在3月下旬。 翻译如下: In March, newly added parking facilities include Zhongjing Petrochemical, Yulong Petrochemical, Jinneng Chemical, and Pucheng Clean Energy. Restarted facilities include Lihe Zhixin, Ningbo Fude, and Guangzhou Petrochemical Line 3. There were many newly added maintenance facilities, with the maintenance concentrated in late March. 请注意,“宁波富德”在英文中被直接音译为“Ningbo Fude”。如果有官方的英文名称,请替换使用。

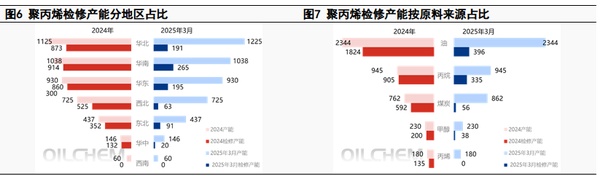

3.2 Domestic Polypropylene Maintenance Loss Volume Structure Analysis

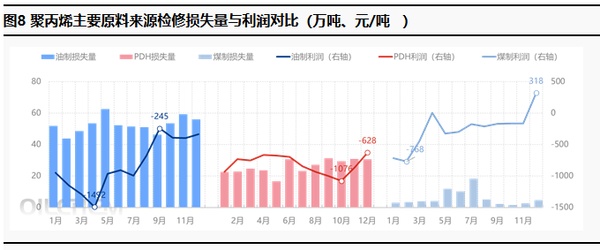

From the 2024 data analysis, the region with the largest maintenance capacity is South China, followed by East China and North China. From the perspective of raw material sources, oil-based, PDH-based polypropylene has a generally higher willingness for maintenance due to cost pressures compared to coal-based polypropylene. In March 2025, South China remains the region with the largest maintenance capacity, followed by North China, mainly because these regions have a larger capacity, and secondly, because the proportion of oil-based/PDH polypropylene in South China/North China is relatively high, leading to a higher preference for shutdown maintenance under the influence of cost pressures.

3.3 Analysis of the Impact of Profit on Polypropylene Plant Maintenance

Crude oil, coal, and propane, as the three main raw materials for polypropylene, account for 82% of the total production capacity of polypropylene. Therefore, these three raw materials are used to represent the profit and maintenance loss of polypropylene for analysis.

Affected by geopolitical influences from India, international crude oil prices remain high, leading to a high theoretical cost pressure for oil-based polypropylene facilities, which are on the brink of losses. Due to high freight rates and supply-demand relationships, propane prices have been high for a long time, making the gross profit margin of PDH facilities the lowest among the three types of raw material sources, thus the willingness for facility maintenance remains high. Domestic coal-based polypropylene facilities are mostly built at the mine mouth, with lower coal costs, resulting in less cost pressure and a significant price advantage; therefore, the willingness for maintenance of domestic coal-based polypropylene facilities is low, and the overall renovation rate of the facilities is also low.

IV. Domestic polypropylene is about to enter the peak maintenance season

4.1 Domestic polypropylene future maintenance plan

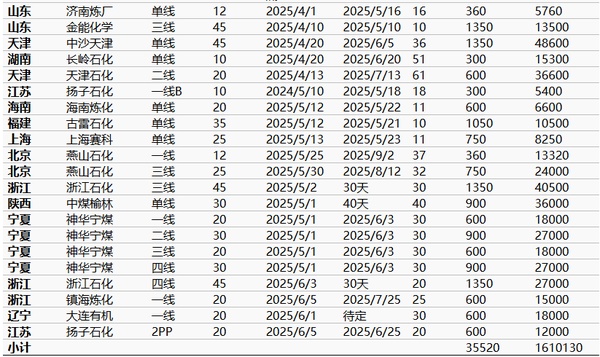

Table 2 Statistics of Domestic Polypropylene Plant Maintenance Plans for the Next Three Months

unit: ten thousand tons/year, day, ton

Regarding the future market, according to statistical data, at the end of March and beginning of April, maintenance plans for domestic polypropylene facilities remain relatively concentrated, with an increase in planned maintenance. It is expected that the overall loss of domestic polypropylene facilities will rise, and the peak maintenance period may occur at the end of May and in June. Pay attention to the impact of new capacity coming online and unexpected shutdowns.

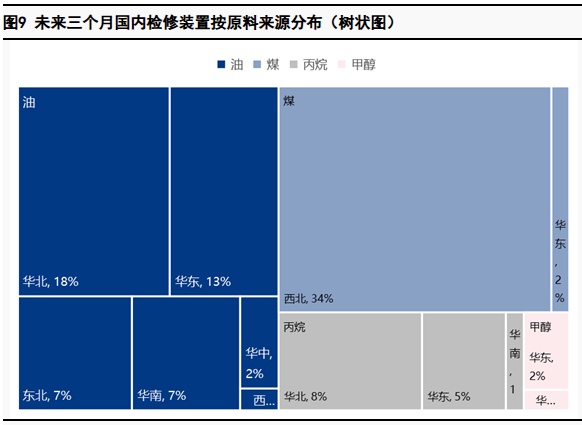

4.2 Future Domestic Polypropylene Maintenance Facility Structure Analysis

From the perspective of future facility maintenance, traditional oil-based polypropylene facilities will still undergo maintenance, and this is true for all major regions, with the highest proportion of oil-based enterprises in North China. For coal-based enterprises, their geographical location is more pronounced, concentrated in the northwest region. There are not many maintenance plans for propane dehydrogenation facilities, which are concentrated in the North China/North China region.

4.3 Maintenance loss prediction and price impact prediction

supply forecast:Expected supply reduction trend, mainly due to the concentrated maintenance of facilities such as Jineng Chemical's second line and Maoming Petrochemical's second line, leading to a future supply reduction situation. Recently, the enterprises under maintenance are concentrated in Pucheng Clean Energy, Anqing Baiju, Zhongjing Petrochemical Phase II Line 1/Line 2, and Yulong Petrochemical.

demand forecastingDownstream rigid demand procurement is the main focus, as the global economic downturn and overseas tariffs have affected some downstream export orders. Under the dual pressure of reduced domestic and international orders, the willingness of downstream raw material procurement to replenish inventory is low. According to plastic weaving data, the raw material inventory days for large enterprises in the plastic weaving sample increased by 2.60% compared to last week; the raw material inventory days for BOPP sample enterprises decreased by 5.39% compared to last week. The raw material inventory days for modified PP increased by 0.79% compared to last week.

cost forecast:Cost support still exists, although there is an expectation of easing in international oil prices, due to recent geopolitical benefits leading to a climb from recent lows in international oil prices; propane follows the trend of international oil prices, with recent downstream market entry supporting prices; propylene has seen limited high-end transmission recently, and is mainly stable in the short term.

In a comprehensive view:The continuous expansion and increase in the supply side contrasts sharply with the weak response from the demand side. The imposition of additional tariffs overseas has curbed downstream export orders, coupled with a slow increase in domestic demand, dragging down the mainstream market transactions. The bottom support for the market lies in the relatively stable cost side and ongoing maintenance benefits, alleviating downward pressure on the market. In the short term, the market will revolve around the confrontation and game between supply and demand and the cost side. It is expected that the market will fluctuate weakly within the range of 7250-7450 yuan/ton in the short term, with close attention to changes in additional tariffs overseas, progress in destocking of social inventory, and the status of demand-side variables. In the medium to long term, prices may see a slight rebound supported by maintenance benefits, fluctuating around 7500 yuan/ton.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)