Commissioning! Surges by over 700%!

Recently, multiple PMMA project updates have been announced: 1. Jiangxi Jingsu Technology Co., Ltd. has publicized an 88,000-ton optical-grade PMMA project; 2. Zhejiang Huashuaite New Material Technology Co., Ltd. has commenced a 35,000-ton annual aviation PMMA project; 3. Yan'an Energy and Chemical plans to build a 50,000-ton/year MMA and 50,000-ton/year PMMA facility.

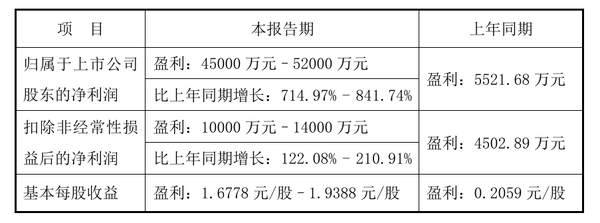

Notably, at the beginning of the year, Shuangxiang Corporation released its 2024 performance forecast: the net profit attributable to shareholders is expected to increase by 714.97% - 841.74% year-on-year; the net profit after deducting non-recurring gains and losses is projected to grow by 122.08% - 210.91% year-on-year. The significant growth in performance is mainly attributed to the gradual release of production capacity from its wholly-owned subsidiary, Chongqing Shuangxiang Optical Materials Co., Ltd., which includes a 300,000-ton annual PMMA, MS, and 40,000-ton special ester project.

A New Round of Expansion

A New Round of Expansion

A New Round of Expansion

A New Round of Expansion

A New Round of Expansion

A New Round of ExpansionCurrently, domestic PMMA still benefits from the demand for replacing high-end imported products, while some capacities with low integration levels, small scale, and limited technology will face the risk of being phased out.

Currently, domestic PMMA still benefits from the demand for replacing high-end imported products, while some capacities with low integration levels, small scale, and limited technology will face the risk of being phased out.At present, the PMMA industry has entered a new round of expansion. The rapid increase in the production scale of upstream MMA monomers and the replacement of imported products provide significant opportunities for the development of downstream industries.

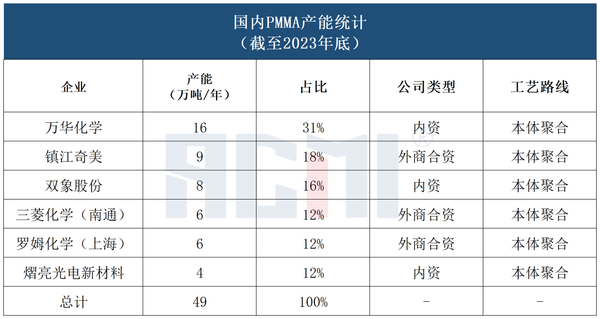

At present, the PMMA industry has entered a new round of expansion. The rapid increase in the production scale of upstream MMA monomers and the replacement of imported products provide significant opportunities for the development of downstream industries.As of 2023, the domestic PMMA capacity is about 800,000 tons/year, including 490,000 tons/year of PMMA resin pellets, 300,000 tons/year of PMMA sheet, and about 10,000 tons/year of other forms of PMMA. The specific distribution of PMMA resin is as follows:

From the perspective of imports and exports, primary form PMMA remains the main imported product. In 2024, the import volume of primary shape polymethyl methacrylate (PMMA) is about 163,000 tons, while the export volume is 54,000 tons. In 2023, the corresponding import volume was about 182,000 tons, and the export volume was 37,000 tons.

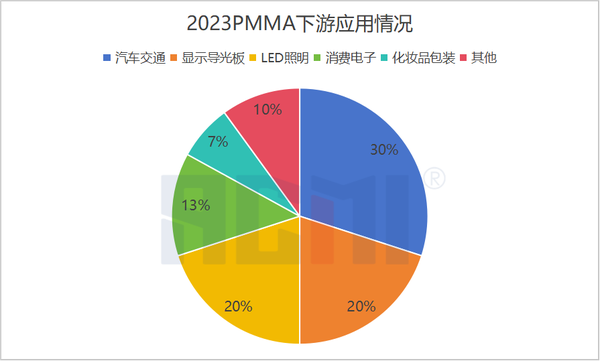

From the perspective of imports and exports, primary form PMMA remains the main imported product. In 2024, the import volume of primary shape polymethyl methacrylate (PMMA) is about 163,000 tons, while the export volume is 54,000 tons. In 2023, the corresponding import volume was about 182,000 tons, and the export volume was 37,000 tons.In terms of actual consumption, in 2023, the domestic consumption of PMMA (resin granules) was about 310,000 tons, a year-on-year increase of 3%. In the detailed demand for this market, the four major sectors—automotive transportation, display light guide plates, consumer electronics, and LED lighting—account for the majority of the market share.

In terms of actual consumption, in 2023, the domestic consumption of PMMA (resin granules) was about 310,000 tons, a year-on-year increase of 3%. In the detailed demand for this market, the four major sectors—automotive transportation, display light guide plates, consumer electronics, and LED lighting—account for the majority of the market share.

Based on a comprehensive analysis of domestic production capacity, customs import and export data, and other sources, China's PMMA resin production capacity has increased from 350,000 tons/year to 490,000 tons/year over the past five years, with an annual compound growth rate of about 7%. However, despite this, the corresponding import volume remains at a high level, while the operating rate of domestic PMMA facilities lingers around a low of about 60%. The main reason for this phenomenon is the overcapacity and high concentration of low-end products.

In addition, local companies such as Wanhua Chemical and Shuangxiang Co., Ltd. have begun to stand out, while foreign enterprises like Chimei Chemical (Zhenjiang) and Mitsubishi Chemical have experienced declines in capacity utilization and market share, indicating an accelerating trend of "domestic substitution."

PMMA Application Situation

Applications of PMMA

Applications of PMMA

Applications of PMMA

Applications of PMMA

Applications of PMMAWith the continuous increase in domestic production capacity, it is essential to place greater emphasis on developing diversified downstream applications in the future to maintain a competitive edge.

With the continuous increase in domestic production capacity, it is essential to place greater emphasis on developing diversified downstream applications in the future to maintain a competitive edge.

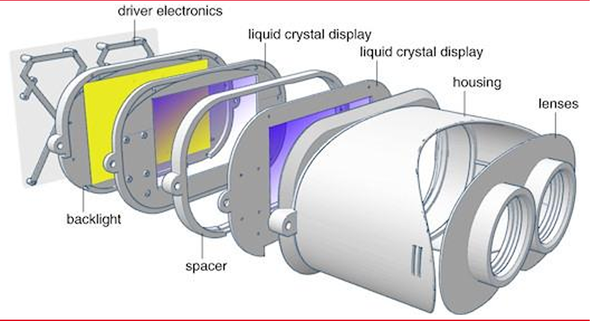

Light guide plates for liquid crystal displays

Light guide plates for liquid crystal displays

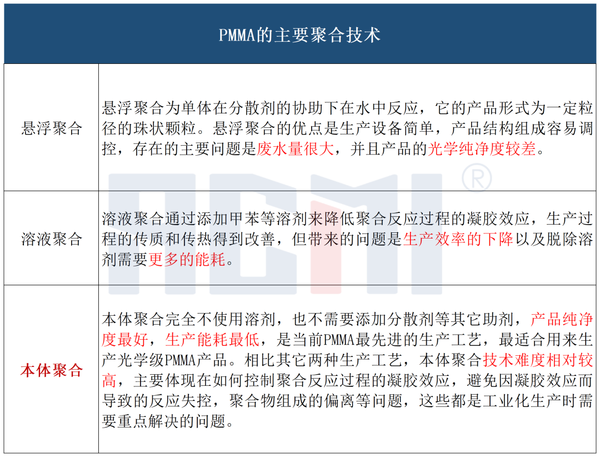

About the polymerization process of PMMA and global production capacity

About the polymerization process of PMMA and global production capacity

About the polymerization process of PMMA and global production capacity

About the polymerization process of PMMA and global production capacity

About the polymerization process of PMMA and global production capacity

About the polymerization process of PMMA and global production capacity

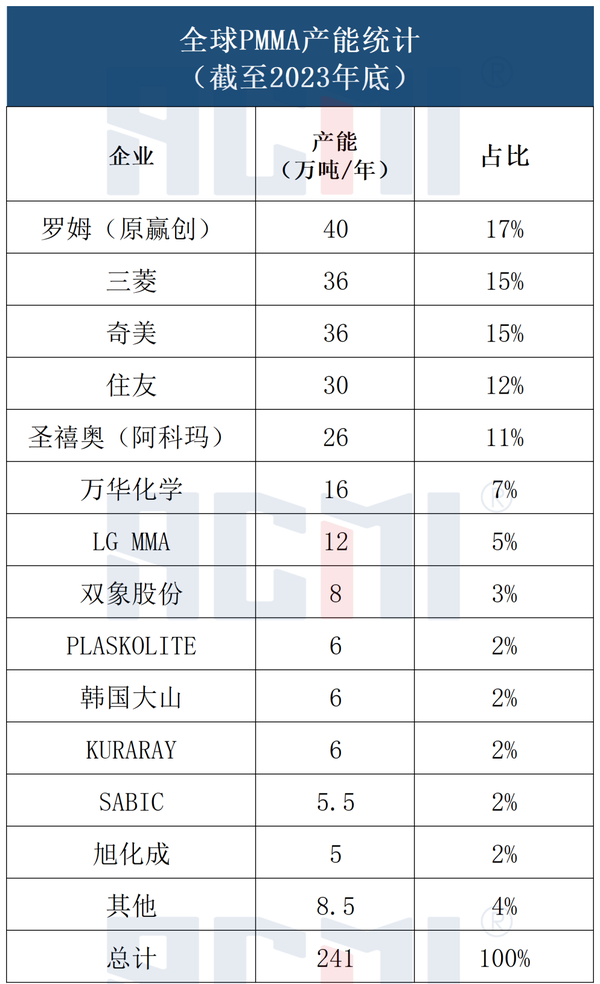

As of the end of 2023, the global capacity distribution of PMMA is as follows:

As of the end of 2023, the global capacity distribution of PMMA is as follows:

Source: Petrochemical Federation, Chemical New Materials, Donghai Securities, official websites of various companies

Source: Petrochemical Federation, Chemical New Materials, Donghai Securities, official websites of various companies【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift