Stalling Out! April Auto Market Sales Slump, Dealing a Heavy Blow to the Rigid-Demand PA6 Market

Since May 2026, the PA6 chip market has remained caught between cost support and weak demand, struggling to move forward. Upstream crude oil and benzene prices have fluctuated at elevated levels, while geopolitical risks continue to intensify, keeping cost support relatively strong. However, downstream demand in end-use sectors such as automobiles and textiles has yet to see any substantial improvement. Profits across midstream and downstream enterprises remain severely squeezed, and purchasing continues to follow a “small-volume, just-in-time” model, with no sign of centralized restocking. As a result, PA6 spot prices have fluctuated narrowly within the range of RMB 12,500–12,900/ton, and the market as a whole has shown a pattern of “weak stability with a slight downward bias” and “narrow-range fluctuations.”

Geopolitical conflicts escalate, while cost pass-through continues to exert pressure.

The core driver of this round of PA6 price movements remains the strong pass-through of upstream costs. Around March 2026, geopolitical conflict in the Middle East escalated sharply, and Iran imposed a blockade on the Strait of Hormuz, directly cutting off a critical transit route for roughly 20% of global oil and 30% of liquefied natural gas shipments, triggering severe disruptions across the global energy supply chain. As the supply gap widened, international oil prices surged rapidly from their lows at the beginning of the year, with the average monthly price of WTI crude in March rising by as much as 41% month-on-month, while Brent crude once approached USD 120 per barrel.

Entering May, the U.S.-Iran negotiations have remained deadlocked, and it is difficult to reach an agreement in the short term. According to data from Ping An Securities Research Institute, from May 8 to 15, 2026, the settlement price of WTI crude oil futures rose by 10.48%, while the settlement price of Brent crude oil futures rose by 7.87%. At present, traffic through the Strait of Hormuz is far below normal levels. As of 16:00 on May 15, only 8 vessels had passed through the strait in the previous 24 hours, and the tightening of global oil supplies is still unfolding. GF Futures pointed out that even if the Strait of Hormuz can resume navigation in the short term, it will take some time for logistics and supply to return to previous levels, which to some extent limits the downside of international oil prices.

The surge in oil prices has quickly been transmitted down the industrial chain. According to data from Longzhong Information, from May 8 to 14, the operating rate of petroleum benzene fell month-on-month to 66.04%, and the operating rate of hydrogenated benzene declined month-on-month to 67.99%, leading to a month-on-month drop in domestic pure benzene production. Meanwhile, port inventories in East China continued to decline, falling to 148,000 tons as of May 18, down 8.64% month-on-month. Against the backdrop of tight supply, pure benzene prices have moved higher. Monitoring data from Zhuochuang Information show that as of May 18, the mainstream market closing price of pure benzene in East China stood at 8,360 yuan/ton, up 110 yuan/ton from the previous trading day. With pure benzene costs remaining at high levels, coupled with caprolactam plants proactively cutting production to support prices, the cost-side support for PA6 remains relatively strong.

Downstream procurement is cautious, and the wait-and-see sentiment is strong.

Despite continuous pressure from the cost side, the performance of the downstream market has struggled to support a significant rise in PA6 prices. The core contradiction in the market lies in the "inability to smoothly transmit high prices to the downstream."

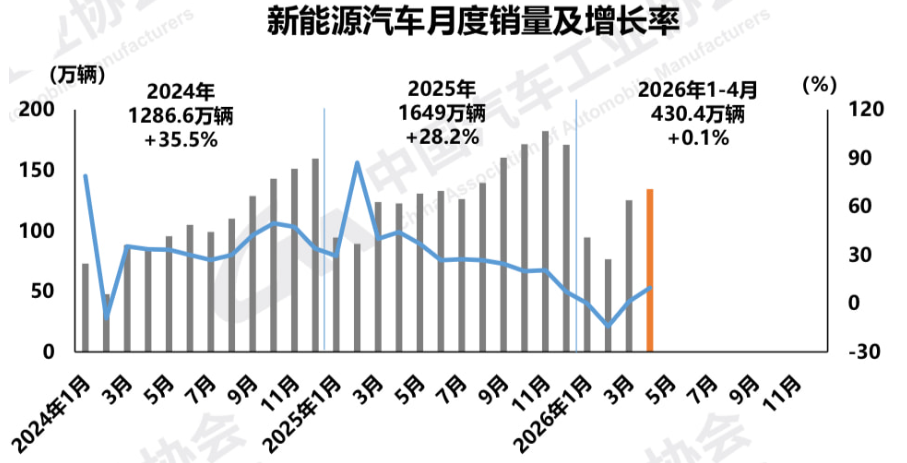

From the perspective of the automotive sector, an important downstream field for PA6, end-market demand is not ideal. According to the latest data released by the China Association of Automobile Manufacturers (CAAM), in April 2026 China’s automobile production and sales reached 2.575 million and 2.526 million units respectively, month-on-month decreases of 11.7% and 12.9%, and year-on-year decreases of 1.7% and 2.5%; from January to April, cumulative automobile production and sales were 9.614 million and 9.574 million units, down 5.5% and 4.8% year-on-year respectively. Domestic automobile sales in April amounted to only 1.625 million units, a year-on-year decline of 21.6%, and domestic sales of conventional-fuel vehicles fell 21% year-on-year, with consumer waiting-and-seeing sentiment remaining strong. Although new energy vehicles performed relatively steadily (production and sales in April rose 5.5% and 9.7% year-on-year respectively), the overall auto market is still in a period of domestic demand adjustment, which limits the demand pull for upstream chemicals such as PA6.

In the textile and chemical fiber industry, although full production has resumed in the second quarter, the growth of terminal orders remains weak, and downstream weaving enterprises generally have a low acceptance of high-priced raw materials. According to a research report by Caitong Securities, the current operating rates of petroleum asphalt, polyester filament, and PTA have significantly declined and are at historically low levels. Polyester filament and PTA correspond to the manufacturing of textiles, garments, and other chemical fibers, and high oil prices are causing a demand feedback loop from the bottom of the industry chain. In the first quarter of 2026, the average operating load of nylon is expected to be about 68%, a significant decrease of 14.01 percentage points compared to the same period in 2025. Downstream factories are mostly adopting a "small orders based on demand, purchasing as needed" strategy, lacking centralized replenishment and large order transactions, with a strong sense of caution prevailing. Data from the China Association of Automobile Manufacturers shows that domestic automobile sales in April fell sharply by 21.6% year-on-year, which is a typical reflection of weak terminal demand.

A tug-of-war between cost support and demand pressure

Under the intertwining forces of bulls and bears, the PA6 chip market has not continued the one-sided surge seen in March, but has instead entered a correction phase followed by a period of oscillation. According to Jinlianchuang's tracking, the current spot price of PA6 is hovering around 12,500 to 12,900 yuan/ton, showing an overall trend of "weak stability, slightly weak, and narrow fluctuations."

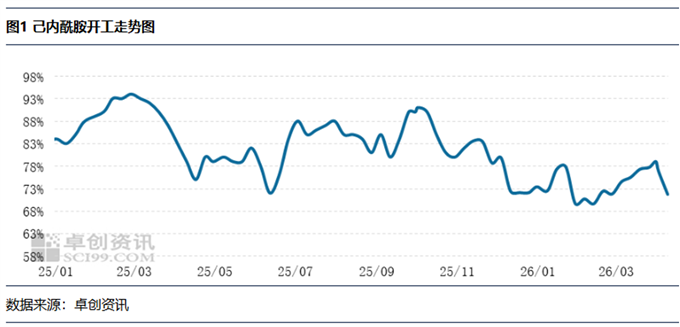

Caprolactam, as the direct upstream raw material of PA6, is also at a critical stage of bullish-bearish competition. According to SCI99, caprolactam plants gradually initiated production cuts after the holiday, with the overall operating rate reduced by 10%; the industry’s current operating rate stands at around 74%. As of May 11, the reference price for the East China caprolactam market was RMB 12,200/ton, down RMB 150/ton from the end of April. At present, upstream and downstream players remain locked in a stalemate, and some low-priced PA6 chips have already inverted against caprolactam prices, highlighting mounting loss pressure on producers.

From the supply side, China’s total PA6 output is expected to reach around 7 million tons in 2026, up 240,000 tons year on year. However, due to high costs and weak market demand, some polymerization enterprises have reduced operating rates, keeping supply pressure relatively manageable. On the demand side, however, momentum remains insufficient, with downstream companies’ profit margins severely squeezed and cost pass-through to end users proceeding poorly, leaving the market without strong incentives for concentrated restocking.

Geopolitical situation and downstream restocking are key variables.

In the short termThe PA6 market is highly likely to remain in a tug-of-war between fluctuations in raw material prices and downstream buyers’ actual willingness to restock. If the situation in the Middle East does not deteriorate further to an extreme extent and downstream demand fails to recover substantially, PA6 prices will continue to struggle between cost support and demand pressure.

From the perspective of oil price driversPing An Securities’ research report believes that the short-term supply crisis in energy and chemical products has not yet been resolved, and that oil and chemical product prices are unlikely to return to pre-conflict levels. However, Guotou Anxin Futures also pointed out that if the geopolitical situation eases quickly and the strait gradually resumes navigation, crude oil prices may fall rapidly. Nevertheless, since restoring shipping and resuming oilfield production both take time, it is expected to be difficult for prices to fall back to low levels. As for benzene, given the current loss-making state of downstream sectors, demand is weak and there is resistance to high-priced feedstock, which to some extent limits benzene’s upside. However, arrivals at major East China ports are limited, inventories continue to decline, and prices are likely to remain steady with a slight upward bias.

From the mid to lower reaches.According to a research report from Open Source Securities, the inventory of fabric at weaving enterprises is currently at a historic low level. As of April 17, the inventory of greige fabric at textile enterprises was only 17.91 days, placing it in the 0.4 percentile since 2018. In the future, as crude oil prices stabilize and with the increase in demand for apparel in the second half of the year, weaving enterprises are expected to enter a replenishment cycle for chemical fiber raw materials. However, the pace at which the replenishment demand materializes still needs to be observed in relation to the recovery of terminal orders.

In summary, all things considered.At present, the PA6 market is in a complex stalemate characterized by “high costs, weak demand, squeezed profits, and intense bargaining.” As long as costs do not fall significantly, chip prices will retain some support at the bottom. However, if downstream demand remains sluggish and orders fail to recover meaningfully, the market is likely to continue fluctuating on the weak side. Going forward, close attention should be paid to the progress of U.S.-Iran talks and changes in navigation through the Strait of Hormuz, trends in international crude oil and pure benzene prices, as well as tangible signs of improvement in downstream automobile production and sales and textile orders.

Sources: Zhuansu Shijie, JLC, CAAM, MIIT, SCI99, OilChem, Ping An Securities Research Institute, SDIC Essence Futures, CSC Futures, Caitong Securities, Kaiyuan Securities, Xinhua Finance, Ruida Futures, etc.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

$80 Million Hammered Down! TMD Business Acquired By TNJ Ohio After Judicial Ruling

-

Daily Review: Cost and Supply Support Push Polyester Bottle Film Market Higher

-

【Overseas News】Trump visits china, us auto industry issues collective appeal; china-us economic and trade talks held in south korea; celanese announces price increase

-

[PVC Weekly Review] Policy Support Weakens, Market Continues Downward Trend