Polyethylene Supply Structure Changes! Largest Import Source Faces Safety Issues, China's Import Dependency Analysis

The global polyethylene supply landscape is undergoing accelerated restructuring, with geopolitical risks hanging like a sword of Damocles. The Middle East—particularly Iran—as a core source of China's polyethylene imports, directly determines domestic supply-demand balance and price trends through its production capacity, export stability, and logistics channels. Although the UAE ranks as China's top nominal importer, a significant portion of these imports is actually transshipped Iranian material, meaning Iran's actual contribution far exceeds what the surface data suggests.

Core Impact Directly Tackles LDPE Structural Pain Points

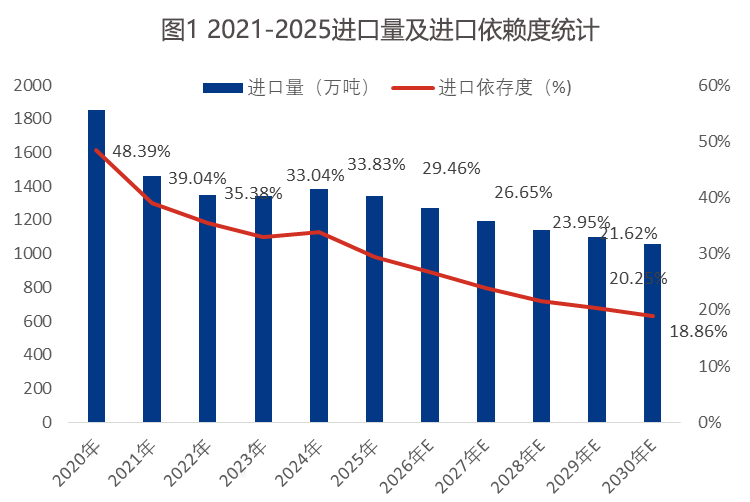

• China’s overall polyethylene import dependency exceeds 29%, whereas LDPE import dependency stands at over 49%, significantly higher than that of HDPE/LLDPE (24–30%).

Iran accounts for 13.8% of China's total LDPE imports, offering superior quality and extremely strong downstream stickiness, making it a typical "essential and irreplaceable material."

• Although the import volume of HDPE is larger (accounting for about 49%), the variety is more dispersed and the substitutability is stronger, leading to a relatively mild impact; LLDPE, which accounts for only 11%, has the least impact.

Iran’s polyethylene (PE) production capacity exceeds 6 million tons per year, accounting for approximately 4% of global output. Its PE exports amount to about 2 million tons annually, over 60% of which are destined for Northeast Asia, with China being the largest importer. Should geopolitical risks escalate—leading to reduced Iranian exports or logistical disruptions—domestic LDPE prices in China would be the first to react, triggering significant speculative activity and a structural price increase; the broader PE market would likewise follow suit amid this sentiment-driven volatility.

This analysis deeply dissects the real impact of Iranian sources on China's polyethylene from three dimensions: supply structure, import source distribution, and variety substitutability, providing key judgment references for companies in the industrial chain, traders, and investors for 2025-2026: under the large trend of accelerating domestic substitution, Iranian LDPE remains a "gray rhino" that is difficult to bypass in the short term.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Middle East Tensions Escalate Sharply: How Polyolefins Respond Amid Soaring Risk Premium

-

Middle East Polymer Export Hub Hit in Sudden Attack, Global Supply Chain Sounds Alarm

-

Middle East Tension Spikes Global Energy Pattern, Crude Oil and Plastic Industries Face Multiple Challenges

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Futures Surge Violently, Polyolefin Spot Prices Rise Sharply in Tandem