Overcapacity overwhelms europe, chinese white knight steps in

The European automotive industry has long been said to be standing at a crossroads. In the past, Europe and its automakers were faced with the choice of whether to transition to electrification; now, as the trend toward electrification becomes unstoppable, the wheels of history are beginning to roll toward the factories of these long-established traditional carmakers.

Recently, a number of foreign media outlets have reported that Europe’s once-roaring automotive assembly lines now stand silent, with factory after factory reduced to “zombie assets.” Weak demand following the pandemic in 2019, the heavy costs of the transition to electrification, and fierce competition from Chinese automakers have together pushed the continent’s auto manufacturing industry into an unprecedented संकट.

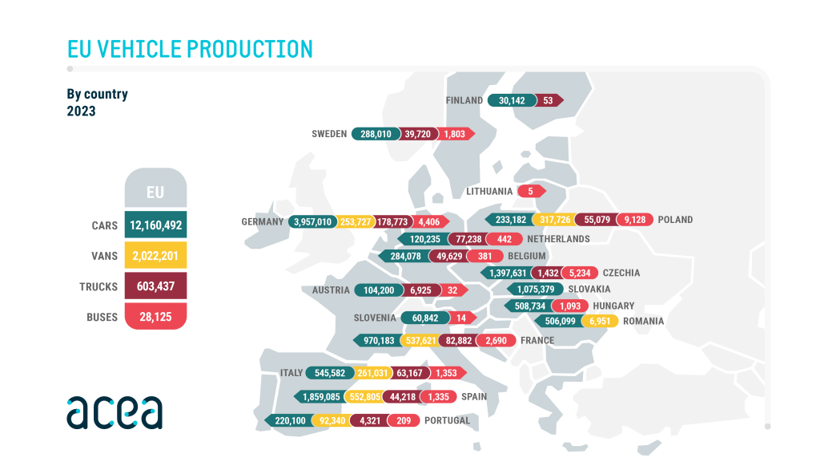

According to data from the trade union IndustriALL, annual automobile production in Europe has plummeted from 16 million vehicles in 2018 to 11.4 million in 2024, a drop of nearly 30%. Overcapacity and waves of layoffs have followed one after another. In 2024 alone, the automotive parts sector cut 54,000 jobs, with another 22,000 eliminated in the first half of 2025.

As European manufacturers struggle, Chinese electric vehicle companies, leveraging their technological strength and cost advantages, see Europe as a "new frontier." Three years ago, brands like BYD, MG, Chery, and Geely were almost unknown in Europe. Now, according to Dataforce data, they account for 9% of overall sales in Europe and 14% of electric vehicle sales.

However, EU tariff barriers and localization regulations require vehicles to be assembled in Europe in order to qualify for subsidies, pushing Chinese automakers to shift from exports to local production. As a result, European factories in urgent need of capacity reduction and Chinese automakers in urgent need of land to build plants have begun a round of negotiations in which each seeks what it needs.

01The familiar “joint venture” model

Faced with the harsh reality of persistently high factory idle rates, European automakers are making a decision that was once unimaginable: handing over their production lines to their former competitors, Chinese carmakers. Rather than pay the hefty price of shutting down plants and triggering social unrest, they are seeking Chinese partners to take them over. This strategy is evolving from isolated cases into an industry-wide trend.

In 2023, Chery Automobile took the lead in breaking the deadlock by acquiring a former Nissan factory located in Barcelona, Spain, with a planned annual production capacity of 200,000 units. This opened the floodgates for subsequent transactions. Last month, Chery further announced the establishment of a research and development center in Paris, specifically to develop a small electric vehicle, which will be produced and supplied to the local market in Europe.

Meanwhile, reports say Nissan is considering selling its factory in Sunderland, UK—its last plant in Europe—to Chery or China’s Dongfeng Motor. Felicie Burelle, CEO of French auto parts manufacturer OPmobility, commented that selling European factories to Chinese manufacturers “is a wise choice, rather than adding to overcapacity.”

Most notably, the French-Italian-American automotive giant Stellantis, the first European manufacturer to publicly make such a decision, announced that it is considering selling part of its Villaverde plant in Madrid to Leapmotor, while Stellantis itself holds a 51% stake in Leapmotor International.

Not only that, Stellantis has already planned to open a plant in Zaragoza, where Leapmotor will produce models under its own brand. An electric SUV under the Opel brand may also be co-produced with Leapmotor in Zaragoza. According to reports, Stellantis’ ambitions go far beyond this: it is considering selling three factories in France, Germany, and Italy to another long-time Chinese partner, Dongfeng Group. A union representative confirmed that a Dongfeng delegation recently visited the factory in France.

In fact, Ford has also joined this trend. Recently, Ford confirmed that it is in talks with China’s Geely Automobile over the partial sale of its plant in Valencia, Spain. Geely is already a co-owner of Renault’s plants in Brazil and South Korea, and this time it will produce a new model for the European market.

Volkswagen in Germany has also shown strong interest. Its CEO, Oliver Blume, recently admitted that the company is studying “whether our Chinese cars have a chance in Europe, or whether we can work with our partners in China.” He added that other options even include selling the factory to a defense manufacturer, but “the worst and most costly option is to close a factory.”

Meanwhile, some European models have already begun to deeply integrate into China’s supply chain. For example, Renault’s electric Twingo was designed in China and makes extensive use of Chinese components. In addition, Stellantis is openly working with Chinese partners to co-produce complete vehicles, rather than merely sourcing parts. According to Bernard Jullien, an automotive industry expert at the University of Bordeaux, this approach is a “shortcut” for manufacturers like Stellantis, which are steadily losing ground in Europe.

But where does this shortcut lead? Julian said that for manufacturers, suppliers, employees, and local officials, selling to Chinese companies rather than letting factories disappear altogether is indeed very tempting. “But this amounts to giving a powerful competitor an advantage in the heart of Europe, installing a powerful accelerator for it to penetrate our market.”

Because Chinese companies are leading in electric vehicle R&D, Julian does not rule out the possibility that European companies will outsource their entire electrification business to Chinese partners. He warned that this “every man for himself” strategy would ultimately boost Chinese manufacturers while “destroying the European automotive industry.”

However, in the context of continuously shrinking demand and a capacity utilization rate of only half, European car manufacturers have few options left. For them, the arrival of Chinese white knights can at least help preserve jobs in the short term, even if it means betting on a rival they once tried to resist.

02Increasingly skilled "localization"

There is no doubt that in the face of such a severe overcapacity situation, Europe urgently needs external forces to inject vitality. Chinese electric vehicle companies are the most reliable partners in this context, as they have also experienced the model of foreign brands entering into joint ventures in China. Therefore, they not only bring capital but also a commitment and action towards deep localization.

IndustriALL’s automotive and aerospace lead, Georges de Leotard, stated clearly: “As long as decent jobs can be protected or created through union representation and collective bargaining agreements, no affiliate union in Europe will reject investment, including investment from Chinese companies.”

This indicates that, in the eyes of European trade unions, Chinese capital is not a threat, but rather a positive force that can be negotiated with and cooperated with. In fact, Chinese investors generally commit to long-term operations locally and strictly recruit and train employees in accordance with EU standards, thereby effectively avoiding the social shock caused by large-scale unemployment.

Some early views had worried that Chinese investors might engage only in “screwdriver” assembly—importing complete knock-down kits from China and carrying out final assembly in Europe—thus bringing only limited benefits to local employment and supply chains. In reality, however, the mainstream Chinese automakers are doing just the opposite.

Justin Cox, Global Production Director at LMC Automotive, pointed out that in the face of rising trade protectionism, “many Chinese automakers are trying to overcome this barrier through localized production, using components sourced entirely from domestic suppliers,” with “domestic” here referring to Europe.

GlobalData analyst Jeremy Wallock also noted that the low localization rate had “prompted European industry stakeholders to call for the introduction of an ‘Made in Europe’ content threshold,” and Chinese automakers are actively responding to this demand by gradually increasing their procurement share in Europe, covering key modules such as batteries, motors, electronic controls, chassis components, and interior parts.

This kind of deep localization not only brings new orders to small and medium-sized suppliers in Europe but also promotes the alignment and mutual recognition of technical standards and certification systems between China and Central Europe, truly realizing the concept of "in Europe, for Europe." For example, Geely and Volvo demonstrate the positive value of Chinese ownership.

Under Geely Holding, Volvo Cars has not only preserved Sweden’s management culture and tradition of union consultation, but also achieved growth in both sales and profits, continued to increase its R&D investment, and steadily advanced its electrification transition. This fully demonstrates that Chinese investors are entirely capable of respecting and integrating into Europe’s labor governance system, while also bringing new vitality and market vision to enterprises.

Other Chinese automakers are actively drawing on this successful experience. Before entering the European market, they proactively communicate with local trade unions and sign collective agreements covering wages, working hours, occupational health, and safety. Some companies have also established China-Europe joint workplace committees at the factory level to regularly consult on issues such as production arrangements and skills training.

The EU previously imposed tariffs on Chinese electric vehicles following an anti-subsidy investigation, but the facts have shown that trade barriers cannot revitalize European manufacturing. The real way forward lies in openness and cooperation. The EU’s newly proposed Industrial Accelerator Act clearly emphasizes attracting foreign investment, creating local jobs, and promoting the deployment of green technologies. The localized production of Chinese electric vehicle companies in Europe is precisely the best response to this policy direction.

Compared with transporting complete vehicles over long distances from Asia, local production significantly reduces the carbon footprint, in line with the requirements of the European Green Deal. At the same time, these factories often make use of existing idle facilities for renovation, avoiding the additional consumption of land and resources associated with building new factories. Therefore, the arrival of Chinese automakers is by no means a threat to European industry.

Current discussions around Chinese overseas investment mostly focus on how to restrict it. Yet in Europe’s automotive sector, the interplay between struggling manufacturers, Chinese electric vehicle companies seeking to enter the market, and increasingly stringent localization rules could help stem the decline of the continent’s industrial base—provided all parties are able to participate.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Daily Review: Cost and Supply Support Push Polyester Bottle Film Market Higher

-

【Overseas News】Trump visits china, us auto industry issues collective appeal; china-us economic and trade talks held in south korea; celanese announces price increase

-

Major industry layoffs: BASF, Evonik, Dow, Wacker, and Others Cut 12,550 Jobs

-

【Overseas News】BASF Launches TPU Product Portfolio! Middle East Conflict Sparks Sulfur Price Surge! First Batch of Chinese Electric Vehicles Lands in Canada