Oil Prices Plunge Over 10% in a Week! Nylon Chain Splits Suddenly: PA66 Soars, PA6 Plunges into Losses

CNPett Info learned that the start of U.S.-Iran negotiations and the potential reopening of the Strait of Hormuz have triggered a drop in international oil prices by more than 10%, leading to a loosening of cost support in the chemical products market.

However, an unusual divergence has emerged within the nylon industry chain: PA66 prices have risen against the trend, supported by INVISTA’s force majeure event, while PA6 has fallen into profit inversion due to declining costs. With improving macroeconomic risk sentiment and intensifying fundamental supply-demand dynamics across the industry chain, the market has entered a critical observation period.

Macro and Geopolitics: U.S.-Iran Talks Begin, Oil Prices Drop Over 10% for the Week

The most significant recent geopolitical event is the advancement of U.S.-Iran negotiations.

On April 11 local time, U.S.-Iran negotiations officially commenced at the Serena Hotel in Islamabad, the capital of Pakistan. The Iranian delegation was led by Parliament Speaker Mohammad Bagher Ghalibaf and included Foreign Minister Abbas Araghchi, among others. The U.S. delegation comprised Vice President J.D. Vance, Presidential Envoy Witkoff, and others. The day before, U.S. President Donald Trump stated in Maryland that the Strait of Hormuz "will reopen very soon, one way or another," adding that the agreement the two sides are preparing to discuss will cover the issue of strait navigation. Brian Deese, Director of the White House National Economic Council, further clarified in an interview that the Strait of Hormuz is expected to resume navigation within the next two months, noting that the U.S. already has a "contingency plan."

As a result, international oil prices fell sharply. As of the close on April 10, the US oil futures contract closed at $95.63 per barrel, down 14.26% for the week; the Brent oil futures contract closed at $94.26 per barrel, down 13.55% for the week.

Xinhu Futures analyzed that oil prices are highly volatile in the short term, with subsequent trends heavily dependent on the progress of negotiations: even if an agreement is reached swiftly, it will take at least 10 days to clear the backlog of vessels in the Strait, and the 10 million barrels per day of production capacity shut down in the Middle East will require a phased resumption; full recovery is expected not earlier than the third quarter—or possibly even year-end—meaning the supply shortage cannot be alleviated in the near term, and oil prices are unlikely to fall below USD 80 per barrel. Should negotiations collapse, geopolitical risk premiums would reignite, potentially driving oil prices higher again.

Nylon Industry Chain: After a collective surge in Q1, market trends diverged sharply in April.

Q1 Review: The Entire Industry Chain Surged Collectively

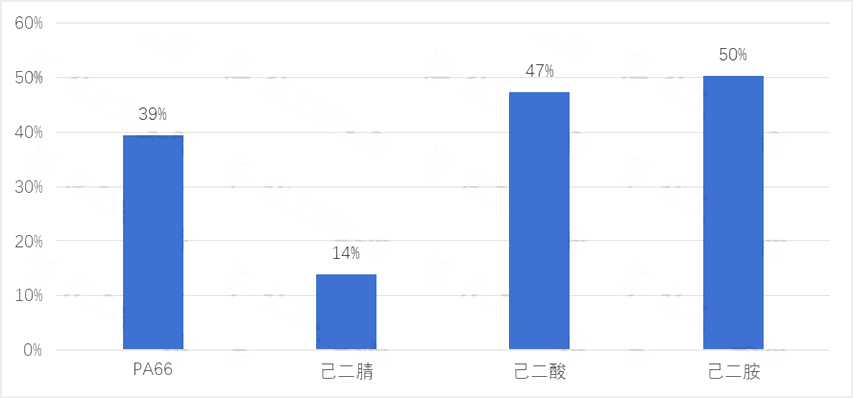

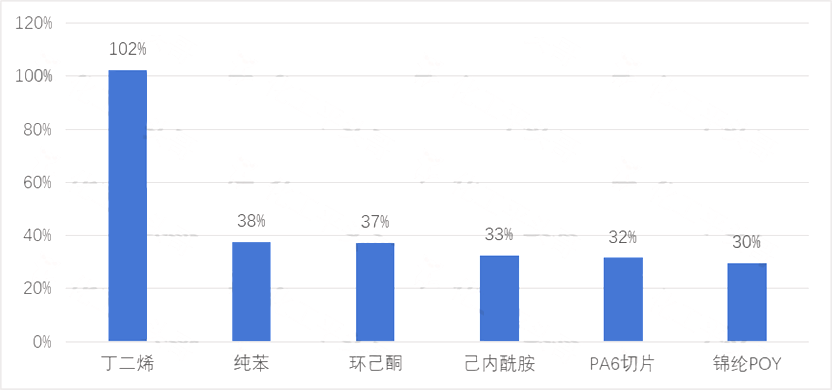

In Q1 2026, the nylon industry chain experienced an unusual collective price surge driven by rising costs. By the end of March, butadiene prices exceeded RMB 17,000 per ton, up over 102%; hexamethylenediamine rose to RMB 26,000 per ton, an increase of more than 50%; adipic acid surpassed RMB 10,000 per ton, rising over 47%; and nylon 66 exceeded RMB 21,000 per ton, climbing more than 39%. The average increase across the industry chain exceeded 20%, exhibiting a pattern where "the further upstream, the greater the price increase."

Cumulative Price Increase of Major Products in China’s Nylon Industry Chain from January to March 2026

Nylon industry related products 3-month cumulative increase

Source: Chemical Pingtouge

Cost-driven factors are the core drivers — Middle East conflicts have pushed up oil prices, thereby increasing the prices of basic raw materials such as benzene and butadiene. The maintenance and reduced production at Invista's Shanghai plant led to a supply contraction. Major enterprises have frequently announced price hikes, triggering panic-related inventory accumulation, forming a positive feedback loop of "price increase - inventory accumulation - further price increase."

Entering April: Macroeconomic Geopolitical Tension Eases and Industrial Chain Fundamentals Competition Intensifies

As the US-Iran negotiations began and oil prices plummeted, the cost support for the nylon industry chain has weakened. However, there is a rare divergence in the trends within the industry chain.

PA66: Going Against the Trend, Dominated by Force Majeure Events

As of April 7, the benchmark price of PA66 was reported at 22,966.67 yuan/ton, an increase of about 10.06% compared to 20,866.67 yuan/ton on April 1. Import high-end grades are now priced as high as 34,500 yuan/ton.

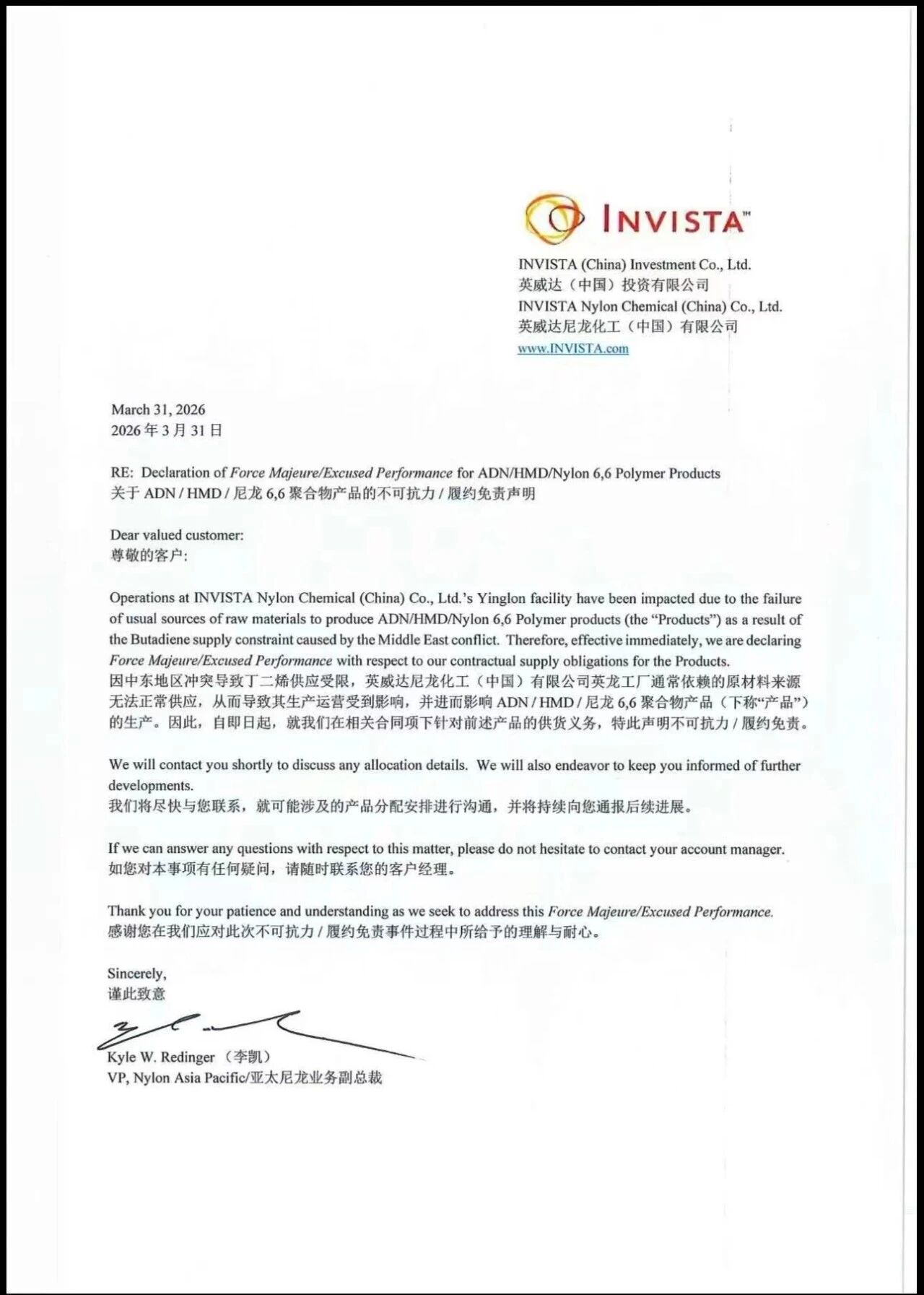

The core reason for the counter-trend rise in PA66 is the force majeure event at Invista.

On March 31, Invista Nylon Chemical (China) Co., Ltd. officially announced that due to the conflict in the Middle East leading to limited butadiene supply, the supply of regular raw materials for its Yinglei plant has been disrupted. Starting immediately, the company has initiated force majeure and liability exemption procedures for its three core products: adiponitrile (ADN), hexamethylene diamine (HMD), and PA66 polymer.

Image source: Invista official announcement

This incident has sparked strong market concerns about a contraction in import supply in May-June, reducing traders' willingness to sell at low prices and thereby providing support to prices.

The PA6 market trend has been markedly different. With benzene prices retreating—spot discussions on April 9 falling to a range of RMB 8,250–8,450 per ton—caprolactam spot prices have declined from early-April highs. As of April 7, the PA6 benchmark price stood at RMB 14,600 per ton, up 3.55% from the beginning of the month, though transactions at higher prices have faced resistance. According to Longzhong Information, weekly average profits for standard-grade PA6 chip have dropped to -RMB 400 per ton, pushing the sector into comprehensive losses. Downstream spinning mills are maintaining only (essential/minimum) purchasing, and in the East China market, mainstream offers for high-speed semi-dull standard chips range between RMB 13,700–14,300 per ton, with actual transaction negotiations remaining weak.

3. Milestone Events in Domestic Substitution

At a time of intense industry volatility, a major breakthrough has been achieved in the core raw material for domestically produced nylon 66.

On April 9, the 200,000-ton annual (ADN) project (Phase I: 50,000 tons) of Aidian, a subsidiary of China Pingmei Shenma Group, officially commenced operations, while the third phase of Aisan’s 100,000-ton annual amino adiponitrile (AAN) project simultaneously broke ground. The project employs the direct hydrocyanation of butadiene process, and all performance indicators meet internationally advanced standards. As a result, Pingmei Shenma has become the world’s only enterprise capable of producing both key raw materials for nylon 66—ADN and AAN—utilizing two distinct technological routes (butadiene-based and caprolactam-based processes), thereby breaking the long-standing foreign monopoly.

Image source: What's Up Updates

Outlook for the Future: Focus on Three Key Variables

1. Progress in U.S.-Iran negotiations and oil price trends

The current major variable remains the Middle East situation. Hasit expects the Strait of Hormuz to resume navigation within two months, but Xinhu Futures points out that even if a deal is reached quickly, the supply gap will be difficult to fill in the short term, and oil prices will find it hard to fall below $80 per barrel. If the negotiations break down, oil prices may surge again. The nylon industry is highly sensitive to oil prices, and the outcome of the negotiations should be closely monitored.

2. The progress of Invista's force majeure recovery

The impact of Invista's force majeure event on PA66 supply will gradually become evident in May and June. Currently, there is no timetable for recovery, and if the duration exceeds expectations, the price of PA66 may rise further. However, one must be wary of the risk of expectation gaps—if domestic ADN capacity ramps up quickly, or if Invista resumes production ahead of schedule, high prices may not be sustainable.

3. Downstream Demand Absorption Capacity

The PA6 industry has fallen into comprehensive losses, and the downstream automotive and electronic appliance sectors have limited capacity to absorb high raw material prices. If terminal demand does not improve, the current pricing system is unsustainable. After the panic inventory buildup in the first quarter, downstream companies need time to digest the high-priced inventory, and demand may experience a phase of weakening in the second quarter.

Theof macro geopolitical risks has brought significant pressure for a cost-side correction in the chemical market, but the fundamental differences within the nylon industry chain have led to a sharp divergence in market trends. PA66 remains at high levels under the dominance of supply-side force majeure, while PA6 is facing a double squeeze from both cost and demand. Corrected translation: The phased easing of macro geopolitical risks has brought significant pressure for a cost-side correction in the chemical market. However, fundamental differences within the nylon industry chain have led to a sharp divergence in market trends. PA66 remains at high levels due to supply-side force majeure, while PA6 is facing a double squeeze from both cost and demand.

The core mainline of the subsequent market will revolve around the actual outcomes of the U.S.-Iran negotiations, the duration of the force majeure at Inovyn, and the release schedule of domestic substitution capacity. Market participants need to be vigilant about the risk of sharp price fluctuations caused by expectations reversal.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Middle East Tensions Escalate Again? U.S.-Iran Talks Collapse Before Starting, Crude Oil Volatility and Plastic Futures Retreat, Plastics Market Faces New Test

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Saudi Core Petrochemical Zone Hit! Trump Issues "Final Deadline" Threat to Iran! Over 5 Million Tons of Production Capacity Halted in April

-

Magna Announces Sale Of Lighting And Roof Systems Business

-

Vimar Launches Linea Switch Range Using Envalior Recycled Material, Cutting Carbon Footprint by Over 80%