Dual Risk Resonance! The Strait of Hormuz Closes Again + Typhoon Bavi Makes Landfall: These Energy and Chemical Products Deserve Attention

There is news on the situation in the Middle East.In the early hours of the 12th, the naval forces of Iran’s Islamic Revolutionary Guard Corps announced,The Strait of Hormuz is now closed, and no vessels are allowed to pass.。

Image: Satellite image released by Iran showing the U.S. military base in Jordan struck by missiles

The statement also warned that if the United States used this incident as a pretext to launch new strikes against Iran, Tehran would respond forcefully by targeting more U.S. bases in the Middle East. On the 11th, a statement posted on the social media account of Iran’s Supreme Leader Mojtaba said that it would “avenge” the late Supreme Leader Khamenei and those killed in the recent “two wars.” Overseas geopolitical confrontation between the United States and Iran has intensified once again, risk-averse sentiment in shipping through the Strait of Hormuz—the world’s key corridor for energy and chemical transport—has surged, and the risk premium on Middle Eastern feedstock supply has been steadily rising.

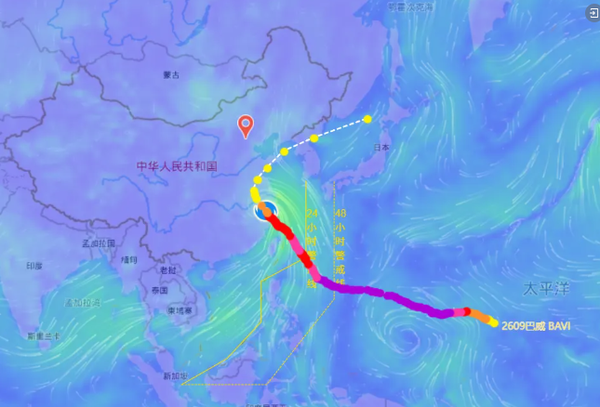

Meanwhile, translate the above content into English and output only the translation result directly, without any explanation.Typhoon Bavi, the 9th typhoon in China.Logged in twice at 11:20 p.m. last night and again in the early hours of the morning.Sweep across the core chemical industry belt in East China.Full typhoon-control measures have been implemented along the entire coastlines of Zhejiang, Jiangsu, and Fujian. Coastal ports have been fully closed, hazardous chemical logistics suspended across the board, and all terminal loading and unloading operations brought to a complete halt, directly disrupting the entire chain of East China chemical imports—from port arrivals and warehousing turnover to downstream delivery—significantly tightening spot market circulation in the short term.

Figure: Path of Typhoon Bavi

The dual-directional reshaping of the supply and demand pattern for chemical products, including core varieties such as methanol, ethylene glycol, styrene, chemical fiber raw materials, and polyurethane raw materials, has led to a shift in market logic.Zhuansu Vision dissects the differences in risks between the short and long cycles and the logic behind product differentiation in a single article, providing practical procurement, production, and risk-control guidance for enterprises in the plastics, chemicals, and upstream and downstream sectors.

I. Geopolitical Risks Intensify: U.S.-Iran Confrontation Escalates, Stability of Shipping in the Strait of Hormuz Declines

1.1 Objective Developments in the Situation

Recently, geopolitical friction in the Persian Gulf and the Strait of Hormuz has intensified, with an escalation in the confrontation between the U.S. and Iran. Navigation controls for regional commercial vessels and liquefied gas carriers have become stricter, leading shipowners to generally adopt risk-averse detour strategies. Ocean freight insurance premiums have increased, significantly raising the uncertainty of shipping for chemical exports from the Middle East.

According to Rystad Energy shipping tracking data, driven by geopolitical risk aversion, vessel traffic through the Strait of Hormuz has fallen significantly from normal levels. A large number of VLCC tankers and chemical tankers are either anchored in place or rerouting to avoid risks, while schedules for ocean-going chemical shipments originating in the Middle East have been widely delayed. Major global chemical shipping routes are showing a phased tightening, directly affecting the import supply and costs of various key chemical feedstocks in China.

1.2 Transmission Logic of the Domestic Chemical Market and Highly Sensitive Varieties

This round of geopolitical disruption has not involved extreme supply cutoffs or large-scale plant shutdowns. The core transmission channels are concentrated in rising costs, delays in ocean shipping schedules, and an increase in market risk premiums, representing a medium- to long-term slow-moving impact.

Cost pass-through: Crude oil and naphtha, supported by geopolitical risks, have fluctuated and strengthened, driving up the price centers of basic feedstocks such as PX, ethylene, and propylene, and passing the increase downstream to plastics, chemical fibers, modified materials, and rubber and plastic products.

Supply-side contraction: The arrival pace of long-haul cargoes from the Middle East, including methanol, ethylene glycol, LPG, and urea, has slowed, while domestic ports continue to destock. For low-inventory products, price elasticity has increased significantly, making spot supply prone to temporary tightness.

Highly sensitive product list: energy cracking chain (methanol, ethylene glycol, styrene, PTA), polyurethane feedstocks (MDI, TDI, sulfur), and general-purpose oil and gas downstream plastics (PE, PP).

II. Weather Disruptions Materialize: Typhoon Bavi Makes a Powerful Landfall, Bringing the Entire East China Chemical Industry Chain to a Standstill

2.1 Substantial Shock to the East China Chemical Supply Chain

East China is the core hub for the import, storage, circulation, and consumption of chemical products in China. More than 90% of the country’s imported ethylene glycol, styrene, PTA, and methanol rely on ports in Zhejiang, Shanghai, and Jiangsu to land. During the typhoon, Zhejiang’s maritime, transport, and emergency management departments activated a Level I typhoon response and introduced region-wide control measures, creating three rigid supply-side shocks to the regional chemical supply chain:

·Port operations fully suspended: As of 18:00 on July 10, all 1,247 port enterprises across Zhejiang had halted operations. Core chemical ports such as Ningbo-Zhoushan Port, Wenzhou Port, and Taizhou Port had completely suspended berthing and loading/unloading operations. All 858 coastal cargo vessels had stopped sailing and taken shelter from the wind, and navigation was prohibited across the East China Sea, Hangzhou Bay, and the Yangtze River estuary.

All hazardous chemical logistics suspended: Areas affected by the typhoon, such as Zhejiang and southern Jiangsu, have initiated "suspension of work, production, and transportation" for typhoon control. Road transport and inland river shipping of hazardous chemicals have been completely halted, and the transfer of raw materials and shipment of finished products in coastal factories has come to a complete standstill.

· Concentrated delays in import vessel schedules: A large number of oceangoing vessels are rerouting to avoid risks, and the arrival schedules of Middle Eastern imported chemical cargoes originally due in mid-July have generally been delayed by 3–7 days, passively tightening spot circulation in East China in the short term.

This typhoon is a short-term regional circulation disturbance and does not change the overall national supply of the chemical industry. After the typhoon passes and the risk is lifted, ports will resume operations in a concentrated manner, backlogged shipments and vessels will arrive in a concentrated way, and logistics will recover quickly. Market trends are expected to show a pulse-like rebound and then quickly return to fundamentals, with no basis for a long-term unilateral upward trend.

2.2 Chemical Product Categories Most Significantly Affected

Based on the port arrival structure, hazardous chemical transportation attributes, and regional consumption structure, the varieties most affected by weather shocks this time are concentrated in East China, particularly in high-import-dependence categories: chemical fiber raw materials (PTA, ethylene glycol, PX), liquid chemicals (methanol, styrene, acetic acid), imported general-purpose plastics (LLDPE, HDPE, PP), and chemical additives (sulfur, liquid ammonia, polyols).

III. Dual Risk Resonance: Short- and Long-Cycle Decomposition and Forecasts of Commodity-Specific Market Trends

3.1 Differentiated Impact Mechanisms of Two Types of Risks

U.S.-Iran geopolitical disruptions (a core medium- to long-term variable): They directly affect global seaborne supply, crude oil and naphtha costs, shipping freight rates, and market risk premiums, with a long-lasting and persistent impact that continues to underpin the price center of chemical products.

Typhoon weather disturbances (short-term pulse variable): affect only the short-term logistics, port inventories, and spot circulation pace for 7–10 days. After the disruption subsides, supply quickly recovers, the price rebound lacks sustainability, and there is no trend-driving power.

The current core market contradiction is that the short-term spot tightness is driven by typhoon-related logistics disruptions, while medium- to long-term price support is dominated by rising geopolitical costs, resulting overall in a composite pattern of short-lived spikes, a moderately strong medium-term trend, and no unilateral bull market.

3.2 Variety Market Forecast

Ethylene glycol: Supported by a dual bullish backdrop, with high reliance on Middle East imports compounded by delayed vessel arrivals in East China and low port inventories, spot prices are expected to remain firm with range-bound fluctuations in the short term. The medium- to long-term trend will hinge on developments in the U.S.-Iran situation and the pace of recovery in subsequent long-haul shipping schedules.

Styrene and PTA: Naphtha costs are providing steady support, while typhoons are tightening short-term spot circulation. End-use demand from textiles and packaging remains stable. Overall, the market is expected to maintain a rangebound yet slightly strong pattern, without strong momentum for a sharp unilateral rise.

MDI, TDI, and sulfur: Disruptions to Middle East export shipping routes have supported supply expectations, leading to slight increases in raw material costs across the polyurethane and fertilizer value chains, with market prices showing a mild recovery in line with fundamentals.

PE and PP commodity plastics: Crude oil costs provide bottom support, but with stable operating rates at domestic plants and lukewarm downstream domestic demand, overall price gains remain limited, and market elasticity is markedly weaker than that of liquid chemicals.

Hedging-independent varieties: domestically coal-based methanol, inland domestically produced urea, and other categories with high self-sufficiency and no dependence on Middle Eastern imports are subject to minimal impact from dual risk shocks, with market trends operating independently and volatility remaining manageable.

3.3 Enterprise Practical Risk Control and Procurement Strategy

Considering the differences between long- and short-cycle risks, provide tiered and actionable strategies for chemical trading, manufacturing and processing, and plastics enterprises:

Procurement side: Enterprises with rigid demand should maintain a moderate safety stock of 7–10 days, prioritize securing inland spot supply, and avoid chasing short-term price increases in typhoon-affected regions. Temporarily postpone concentrated long-term contract arrangements for Middle Eastern long-haul cargoes, and wait for greater clarity on shipping schedules and the geopolitical situation before restocking opportunistically.

· Production side: Enterprises along the East China coast should build up raw material inventories in storage tanks in advance, plan backup inland logistics routes ahead of time, and avoid the risk of reduced operating rates or shutdowns caused by disruptions to hazardous chemical transportation; proactively coordinate with upstream and downstream partners to clarify force majeure delivery clauses and reduce default risk.

Trading side: cautiously trade the short-term pulse driven by the typhoon, strictly set take-profit and stop-loss levels, and avoid emotional chasing. For medium- to long-term trades, focus on the main theme of geopolitical risk premium, maintain a range-bound yet moderately bullish mindset, and avoid blindly taking a one-way bullish view.

Core tracking indicators: vessel traffic data in the Strait of Hormuz, Middle East chemical product shipping schedule forecasts, the progress of port reopening and work resumption at major ports in East China, and weekly port inventory data for methanol, ethylene glycol, and styrene.

The current fluctuations in the chemical market are a typical resonance between short-term weather circulation disturbances and medium- to long-term geopolitical supply risks. These two types of risks differ completely in their impact cycles, intensity, and logic. Companies need to abandon extreme thinking of only bullish or bearish views, and instead differentiate between short-term circulation gaps and long-term cost support. In the short term, the focus should be on logistics recovery and inventory replenishment after the typhoon, while in the medium to long term, continuous monitoring of the geopolitical situation in the Middle East and changes in overseas supply is essential.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Off-Season Demand Weighs, Polyethylene Market Expected to Fluctuate Under Pressure

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape