Consumables National Procurement Continuation Results Announced, Consumables Volume-Based Procurement Officially Enters a New “High Quality, Fair Price” Cycle

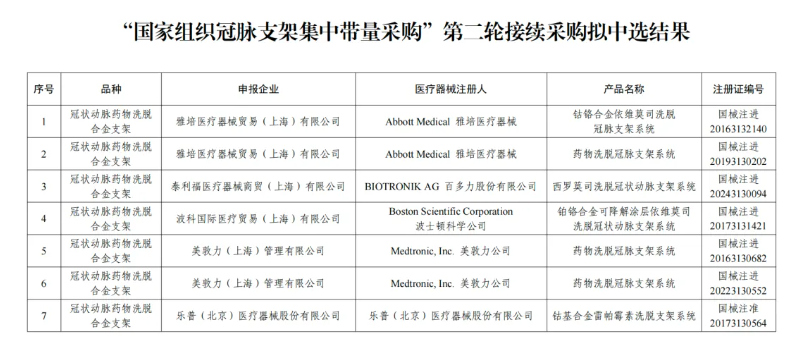

On May 20, 2026, in Tianjin, a highly anticipated “exam” came to an end here—the second round of the National Volume-Based Procurement for coronary stents was officially opened. A total of 15 companies, bringing 30 products, participated, and in the end all companies passed, with 27 products securing proposed winning qualifications. This “zero elimination” continuation sends a far richer signal than the “pass rate” itself—it marks the coronary stent national procurement as having officially moved from a “price war” into a “value cultivation phase.”

From “10-in-6” to “everyone gets through”: a profound shift in the logic of centralized procurement

Six years ago, when coronary stents were first included as one of the initial batches of high-value medical consumables in the nationally organized volume-based procurement program, the bidding scene was filled with intense maneuvering and an air of uncertainty and tension. At that time, the rule was that 27 products competed for 10 winning slots—a true “elimination battle” in which the average price cut reached as high as 92.5%. With the implementation of the first batch of heart stent centralized procurement in 2020, stent prices fell from an average of 13,000 yuan to around 700 yuan, and the abrupt end of the “ten-thousand-yuan era” sent shockwaves throughout the industry.

By the first round of procurement launched in 2022, however, the rules had already changed: any bidder could win as long as its submitted price was no higher than the highest valid bid, with the elimination of differential cutoffs becoming the biggest highlight. The average price of winning products rose by 25.3%.

As time moved into May 2026, the second round of continuous procurement continued the “inquiry-based pricing” model: as long as a company’s quoted price reached a certain threshold, it could be selected, and different price levels corresponded to different proportions of the “volume” awarded, reflecting the principle of exchanging volume for price and linking price with volume. More notably, before this bidding, the highest valid declared price for alloy stents had been raised from RMB 848 per unit to RMB 949 per unit, an increase of about 11.91%. This stands in sharp contrast to the aggressive “price-cutting to the bottom” style seen in 2020.

The shift from "elimination by difference" to "passing upon meeting standards" is primarily due to the fact that after six years of centralized procurement practice, coronary stents have moved from the "price squeezing" stage to a new cycle of stable supply, stable clinical use, and quality assurance. Lu Yun, director of the Pharmaceutical Price Research Center at China Pharmaceutical University, pointed out that following previous centralized procurement, a market-driven reasonable price for coronary stents has been established.

The National Healthcare Security Administration has made it clear that the continuation of this procurement will adhere to the principles of "stabilizing clinical practices, ensuring quality, combating involution, and preventing collusion." The significance of the phrase "combating involution" cannot be underestimated. In recent years, the rules for high-value medical consumables procurement have been continuously optimized. For example, in the sixth batch of high-value medical consumables procurement in 2026, the selection will no longer simply rely on the lowest price to calculate price differences. Instead, when the lowest price is excessively low, a control benchmark of 65% of the average qualifying price will be used. All of this points to a common proposition: procurement will no longer be solely focused on low prices, and industry competition is moving towards a positive cycle.

14 familiar models "continue," with several upgraded new products "making their debut."

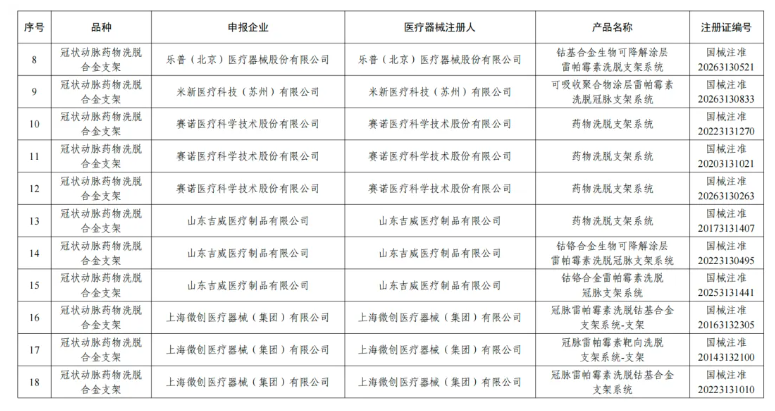

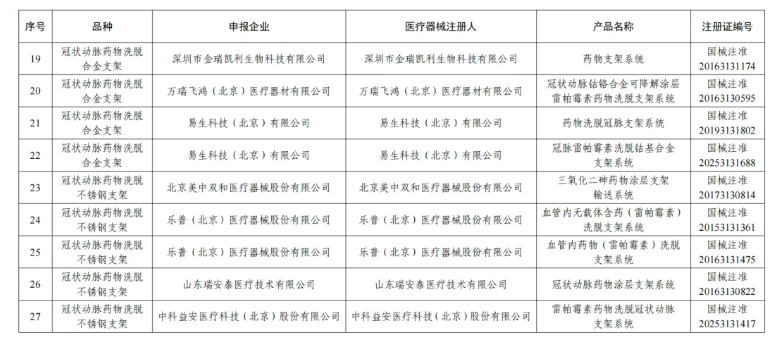

An interesting phenomenon is that although all companies have successfully “made it ashore,” competition has not disappeared. Judging from the preliminary selection results, all 14 stent products that were previously selected have continued to be selected, including products from foreign companies such as Medtronic, Abbott, and Boston Scientific, as well as products from domestic companies such as Shanghai MicroPort, Beijing Lepu, and Shandong JW. This means that the mainstream product chains long familiar to and trusted by clinical users have remained highly stable, and doctors and patients do not need to “readjust” their treatment habits.

At the same time, this round of continuation procurement added several upgraded products. New-generation products approved for market in recent years, such as Medtronic’s “Resolute Onyx” stent and Shanghai MicroPort’s “Firehawk” stent, were also included on the list of selected products. Lu Yun, director of the Pharmaceutical Pricing Research Center at China Pharmaceutical University, revealed that among the 27 products proposed for selection, 13 are newly added products, of which six are upgraded new products.

It is evident that “trading price for volume” is no longer merely a price-based game, but has also catalyzed the iterative upgrading of products themselves. With the addition of high-end upgraded products, the centralized procurement market is gradually entering a new pathway of “premium quality at premium prices.”

2.5-Fold Growth in Eight Years: Clinical Usage Casts a Vote of Confidence

Compared with the list of winning bidders itself, a set of data on demand is equally intriguing.

The annual procurement demand of medical institutions is approximately 2.73 million units, representing a 155% increase from the 1.07 million units in the first round of centralized procurement and a 47% increase from the 1.86 million units in the previous renewal round. Meanwhile, the number of medical institutions participating in volume reporting rose from 2,408 in the first round to 4,468, an increase of 86%. In analyzing these figures, Lu Yun stated that the number of reporting hospitals increased from more than 2,400 to more than 4,400, nearly doubling, while the committed procurement volume grew from just over 1 million units to more than 2.73 million units, an increase of over 1.5 times. “This reflects clinical recognition of the selected products.”

But behind this lies a deeper logic: when stent prices became affordable, medical demand was released. According to statistics, the number of coronary intervention procedures performed by medical institutions nationwide reached about 1.9 million in 2024, a sharp increase from about 1 million in 2020 before the centralized procurement program. In other words, from before to after centralized procurement, the decline in stent prices released treatment demand that had previously been suppressed by high costs, enabling more patients to undergo interventional therapy. This is the most direct manifestation of the centralized procurement policy of “trading price cuts for higher volume”—lower prices not only did not restrain clinical use, but instead expanded the overall foundation of medical services.

Moreover, it is encouraging that the number of medical institutions performing cardiac stent implant surgeries has increased from over 2,400 in 2020 to over 3,600 in 2023. Among these, the number of secondary medical institutions has grown from 1,200 to nearly 1,700. More and more county-level hospitals are now equipped to perform stent implantation procedures, allowing acute myocardial infarction patients to receive treatment closer to home. As the Joint Procurement Office has pointed out, this will win more valuable time for the nearby treatment of acute myocardial infarction patients and save lives.

90,000 cases of real-world data: Price reduction of centralized procurement stents without compromising quality.

“Prices have dropped so much — can quality still be kept up?” This has been a question shared by patients and doctors for many years. Starting in 2024, Fuwai Hospital of the Chinese Academy of Medical Sciences (National Center for Cardiovascular Diseases) took the lead, together with eight hospitals nationwide that have a high volume of coronary stent procedures and high standards of clinical quality, in conducting a real-world study on the use of coronary stents in more than 90,000 patients before and after centralized procurement. On May 19, 2026, the National Healthcare Security Administration released this reassuring answer.

The study divided the data into two groups: before the volume-based procurement program (2019) and after its implementation (2022). The results showed that the number of coronary interventional procedures performed in the eight hospitals was 43,000 before the program and nearly 50,000 after it, representing a 15% increase—indicating that the program did not make doctors less willing to perform procedures or patients more reluctant to undergo them. Meanwhile, the average number of stents used per case declined from 1.5 before the program to 1.3 after it, a 13% decrease, suggesting that clinical use of consumables became more standardized, with physicians more often using longer stents to cover lesions and avoiding the previous inappropriate practice of using more stents instead of longer ones.

In terms of the most closely watched clinical efficacy outcomes, a comparison of major adverse cardiovascular events (MACE) within two years after surgery showed no statistically significant differences in the incidence rates of any indicators among patients, and the incidence of most adverse events even declined slightly after centralized procurement. For example, the two-year rehospitalization rate for heart disease decreased from 5.5% to 5.4%; the incidence of new myocardial infarction fell from 1.8% to 1.6%; and the rate of in-stent thrombosis dropped from 0.3% to 0.2%.

In terms of costs, this has also delivered tangible benefits: before the centralized volume-based procurement program, the average total inpatient cost for a single coronary intervention was nearly RMB 60,000; after the program, it decreased to RMB 44,000. After medical insurance reimbursement, patients’ out-of-pocket burden is further reduced, and medical institutions’ willingness to participate in the program is correspondingly higher.

This large-scale real-world evidence, drawn from over 90,000 patients across eight top-tier hospitals, scientifically addresses public concerns that “you get what you pay for” — the data show that while stents have become cheaper, their efficacy has not been compromised, and their safety has even seen a slight improvement.

Industrial Collaboration Behind Scaffold Renewal: The “Ripple Effect” of National Volume-Based Procurement

The continued centralized procurement of coronary stents has effects that extend far beyond coronary stents themselves. Since the first batch of national centralized procurement, the categories covered by centralized procurement of medical consumables have expanded comprehensively from coronary stents to include joints, spine, intraocular lenses, cochlear implants, peripheral vascular stents, and other categories. To date, more than 10 million centrally procured selected stents have been used clinically, benefiting approximately 7 million patient visits.

More notably, the price-constraint effect unleashed by the centralized procurement of coronary stents is transmitting across the entire vascular intervention sector. According to statistics, after the centralized procurement of coronary stents, the usage share of another type of interventional medical device — drug-coated balloons — rose from 5% before procurement to 15%. As an alternative treatment technology to stents, drug-coated balloons previously carried high prices, with listed prices generally above 20,000 yuan. However, in the sixth batch of national procurement for high-value consumables in January 2026, drug-coated balloons were formally included in the procurement scope, allowing companies to bid significantly reduced prices for hospital procurement. With both stents and balloons — the two core coronary interventional products — included in national procurement, overall consumable costs have been further compressed, producing a strong "synergistic cost-reduction" effect.

Notably, this continuation procurement explicitly states that, during the procurement cycle, newly approved products may apply to be added to the list of selected items in accordance with the rules. This means that industry technological innovation will not be "locked out" by collective procurement, and a smooth market channel for subsequent new products is preserved. Under this dual-track regulatory framework of "guaranteeing basics" and "embracing innovation," companies' R&D drive continues to be nurtured.

"New Competitive Logic": Moving from Price Competition to Value Competition

Reviewing the evolution of China’s national centralized procurement of coronary stents over the past six years, several clear milestones outline a gradual policy shift: from the brutal bidding of 2020, with an average price cut of 93%, to the mild price increases and non-differential elimination in the 2022 follow-up procurement, and then to the inquiry-based winning bids and tiered volume-price mechanism in 2026. The policy focus has progressively shifted from price control toward rule optimization and quality improvement.

As demonstrated by this round of follow-on centralized procurement, newly approved products may apply to be added as winning bids during the procurement cycle in accordance with the rules, thereby preserving market access for subsequent innovative products. The principle of “anti-involution” has been further institutionalized, helping to prevent irrational price wars among enterprises. The increase in the maximum valid bid price has also given companies clearer expectations. Under the new regulatory framework, the logic of competition for enterprises is no longer about “trading price for survival,” but instead returns to the right track of product competitiveness, R&D capabilities, and supply chain stability.

The influence of centralized national procurement of medical consumables continues to expand, and a new competitive logic is already beginning to reshape the industry in profound ways. For companies, this means moving beyond the quagmire of low-price “involution” and returning to the cultivation of core competitiveness built on technological barriers and product quality. For medical institutions and patients, the human-centered value of centralized procurement policies is becoming embedded in every diagnosis and treatment in a more sustainable way—high-quality coronary stents, at affordable prices, are being implanted in more people who need them. And for China’s medical consumables industry as a whole, the continued procurement of coronary stents is more than just the renewal of a single product category; it is a mirror reflecting the transformation of governance over high-value medical consumables in China from addressing symptoms to tackling root causes.

Just as seen in the news broadcast: after the bidding results were announced, there was no expected tension or noisy back-and-forth bargaining at the bidding site; instead, there was calm and composure. Everyone understood that this “final battle” of the national procurement was not the end, but the beginning of a new value cycle with greater resilience and vitality.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Two Major Chemical Giants to Shut Down, Sell Again

-

$80 Million Hammered Down! TMD Business Acquired By TNJ Ohio After Judicial Ruling

-

Global chemical industry shaken again! amsty and plastic energy announce bankruptcy, accelerating plastics sector shake-up

-

ENGEL at Plastpol :2026 Intelligent production solutions for stable manufacturing processes