BASF Cuts Core Business As It Exits All Non-Core Operations, Triggering A New Round Of Industry Restructuring

On May 21, BASF issued two announcements simultaneously: it will sell its silicates business to PQ Corporation, and it announced the launch of a cross-divisional transformation project named “CoreShift.”For those who have been following this German chemical giant for a long time, this is not news but rather a confirmation that a strategic logic that has been ongoing for several years is entering its final phase in 2026.

To understand this matter, one must first understand the knife BASF made itself — its Winning Way Forward strategy.

Image source: BASF

One word to sum up BASF over the past three years: subtraction.

If one were to sum up BASF's main theme over the past three years in one sentence, it would be “doing less.”

BASF internally divides its businesses into two categories:Standalone Businesses and Core BusinessThe former refers to businesses that have weak synergy with the core business and can be operated independently or even listed separately; the latter refers to traditional chemical businesses that are deeply embedded in an integrated value chain and tightly interlocked across upstream and downstream operations.

In the past two years, BASF's main actions have focused on the divestiture of its "operational businesses": agricultural solutions segment, coatings business, vitamins and functional food ingredients, and some specialty chemicals... one piece after another has been sold, spun off, or introduced to external investors. This process is officially described as "almost fully completed."

On May 20, the sale of the silicate business was another transaction in this winding-down phase. Silicates may sound unremarkable, but they are upstream raw materials for rubber reinforcement and white carbon black used in green tires, as well as for paints and cleaning agents—typical traditional businesses that have low synergy but significant scale. PQ Company took over, and the logic is clear: the buyer is a specialist player in this niche field, making the acquisition more competitive than staying with BASF.

CoreShiftBlade edge turns inward toward the core.

“The subtraction of ‘autonomous businesses’ has been done; now it’s the turn of the ‘core business’ to cut into itself — that is the essence of the ‘CoreShift’ project.”

According to BASF's official definition, "core business" encompasses four major segments:Chemicals, Materials, Industrial Solutions, and Nutrition & CareThe global sales amount to approximately 40 billion euros.

For the plastics processing industry, “Materials” is the most directly relevant of these four segments: isocyanates such as MDI/TDI, engineering plastics (polyamides, PBT, POM), and polyurethane system materials all go directly into markets such as automotive lightweighting, electrical and electronics, and building insulation, making them names that many domestic processors cannot avoid on their annual procurement lists. The dispersants, lubricant additives, paper chemicals, and other products in “Industrial Solutions,” though less prominent, likewise hold pricing power in specific niche markets.

CoreShift’s goal is quite specific:Reduce net cash fixed costs in the core business by up to 20% by 2029, using 2024 as the baseline.Julia Raquet, who is in charge of this project and formerly served as BASF’s President for Europe, the Middle East, and Africa, reports directly to CEO Markus Kamieth, which in itself indicates the project’s strategic priority.

Julia Raquet, responsible for the CoreShift project, former President of BASF Europe, Middle East and Africa Region (Image source: BASF)

Reducing costs by 20%—what does that mean in the current cycle? For a business with a scale of 40 billion euros, if fixed costs account for 15% of revenue, that results in a cost base of 8 billion euros. A 20% reduction means an absolute saving of 1.2 billion to 1.6 billion euros—this figure is higher than the annual revenue of many mid-sized chemical companies.

Ludwigshafen: The Glory and Burden of Integration

When it comes to CoreShift, Ludwigshafen cannot be overlooked.

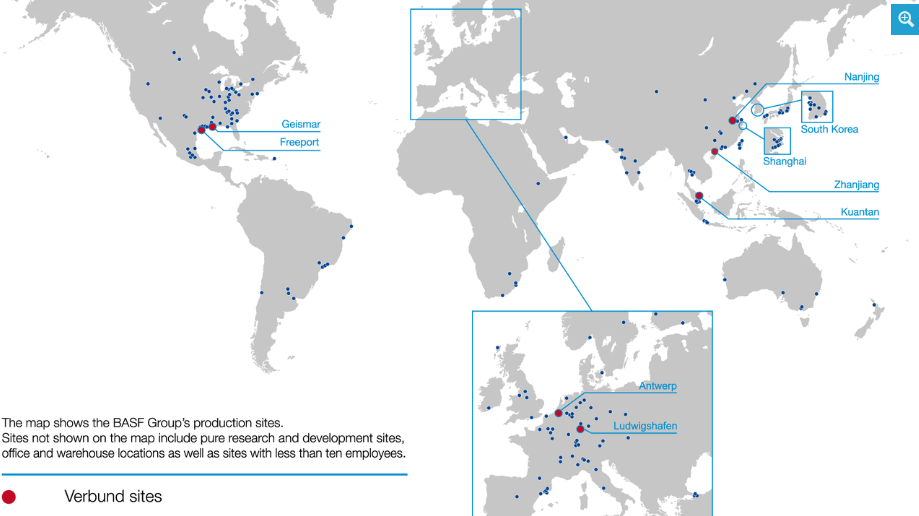

Figure: Distribution of BASF Verbund Sites (Source: BASF)

This small town in southwestern Germany has become one of the largest integrated chemical production bases in the world due to BASF: over 200 production facilities, more than 2,000 kilometers of pipelines, and about 33,000 employees, consuming electricity and steam equivalent to that of a medium-sized European city each year. The integrated (Verbund) system is BASF's proudest competitive advantage—synthesis gas enters upstream, and hundreds of products come out downstream, with by-products serving as raw materials for each other, theoretically achieving much higher energy efficiency than independent factories.

However, this system is becoming a burden in an era of high energy costs. After the Russia-Ukraine conflict, natural gas prices in Europe remained high for an extended period, and the energy cost advantage of the Ludwigshafen site has almost completely disappeared. The other side of integration isVery high fixed costsThe facilities cannot be shut down, the workforce structure is complex, and the pressure from fixed-asset depreciation is heavy. Since the beginning of 2024, the Ludwigshafen plant has already lost about 2,800 jobs, but an agreement reached between the company and the union at the end of 2025 stipulates that there will be no compulsory redundancies for operational reasons before the end of 2028—effectively providing a buffer period while also limiting the scope for radical restructuring.

Julia Raquet said that “the restructuring of the Ludwigshafen site is now in full swing.” How should this be understood? It most likely refers to optimizing facilities and adjusting the product portfolio without large-scale layoffs: shutting down loss-making marginal capacity, concentrating resources on high-value-added products, and advancing the use of digitalization and AI in production scheduling. Meanwhile, the Antwerp site had previously announced plans to cut fixed costs by €150 million by the end of 2028 and eliminate around 600 jobs—roughly one-sixth of its total workforce, a fairly substantial move.

Global Chemicals “Winter”: BASF Is Not an Isolated Case

BASF’s pressures are by no means an isolated incident, but rather a structural predicament collectively faced by the traditional chemical industry across Europe and even globally.

In their 2025 annual financial reports, the chemical giants almost wrote the same script:

- Dow Chemical CompanyNet loss of US$2.4 billion, followed by the announcement of approximately 4,500 layoffs worldwide (about 13%), and plans to shut down its basic silicones plant in the UK by mid-2026;

- CovestroNet loss of 644 million euros, polycarbonate business remains under pressure.

- SABICNet loss was approximately US$6.87 billion, following the prior sale of its European petrochemicals and engineering thermoplastics businesses for a total of US$950 million.

- LyondellBasellNet loss of $738 million.

- INEOSLoss of 660 million euros, selling stake in Italian chlor-alkali business under INEOS Inovyn.

- After laying off 850+ employees in 2025, it will cut another 1,000 jobs in 2026;

- Wacker Chemie: Net loss of €805 million; announced layoffs of about 1,600 employees in May 2026.

Recent relevant developments also illustrate the seriousness of the issue.

Celanese will shut down its Singapore plant and optimize nylon 66 production capacity in North America; DOMO Chemicals plans to sell its engineering materials business, including PA6 and PA66; Mitsubishi Chemical will exit its PBS biodegradable plastics business in Thailand; and Asahi Kasei plans to streamline its Mizushima plant by fiscal 2030, involving shutdowns or production cuts across multiple products, including styrene monomer, LDPE, HDPE, and acrylonitrile.

Any single item on this list would be industry news on its own; taken together, they mark a turning point in an era.

The difficulties facing Europe’s chemical industry have structural roots: persistently high energy costs, continued output from Chinese capacity, and weak demand at home, with both the automotive and construction sectors in the doldrums. Meanwhile, Plastic Energy and Trinseo have respectively entered administration and bankruptcy restructuring—one a chemical recycling company for plastics, the other a traditional player in specialty polymers and styrenic materials. Different types of companies are exiting in different ways, but both are pointing to one thing:This cycle is not merely a simple supply-demand mismatch, but a reshuffling at the level of business models.。

What does it mean for the domestic plastics industry?

From the perspective of practitioners in China, there are several key points worth paying close attention to regarding the developments mentioned above.

First, the repositioning of the supply landscape.SABIC’s sale of its European engineering thermoplastics business, DOMO’s planned divestment of its PA6/PA66 business, and Asahi Kasei’s reduction of HDPE capacity are all events that will directly affect the global supply structure of engineering plastics and general-purpose resins. In the short term, they may lead to supply tightening and price support in certain product categories; in the medium to long term, they present a window of opportunity for domestic substitution in China.

Second, the scope of the contraction of BASF’s “core business.”CoreShift requires focus, which means BASF’s commercial investment in certain non-core products and markets will decline. Domestic agents and distributors should take note: some product lines that previously involved higher service costs may see adjustments in channel policies.

Third, enhancing cost competitiveness driven by ERP and AI.CoreShift has clearly stated that it will drive standardized IT solutions based on a “dedicated ERP system for core business operations” and the broader application of AI. This is not merely an IT project, but a move that will further enhance BASF’s digital capabilities in pricing, supply chain responsiveness, and customer service. Domestic competitors with similar products need to recognize this gap.

What BASF is doing, in its own words, is “building a more focused and synergistic core business.”From an outsider's perspective, it was a chemical empire that once tried to do everything but ultimately embraced the competitive logic of "doing fewer things but doing them well." This shift in logic, in itself, may be more noteworthy than any specific asset sale.

Editor: Lily

Source of materials: BASF official announcement, DT New Materials, Chemical New Materials, May 2026.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Two Major Chemical Giants to Shut Down, Sell Again

-

Global chemical industry shaken again! amsty and plastic energy announce bankruptcy, accelerating plastics sector shake-up

-

$80 Million Hammered Down! TMD Business Acquired By TNJ Ohio After Judicial Ruling

-

ENGEL at Plastpol :2026 Intelligent production solutions for stable manufacturing processes