[today’s plastic market] majority continue to rise! pe, ps, abs, eva, pet and others in the green, pc up 700

Summary: Summary of plastic market general material and engineering material prices and forecasts on January 14. In terms of general materials, potential geopolitical risks continue to influence and push costs higher. PE prices are running at high levels, with an overall increase of 29-93; PVC experiences partial fluctuations, with some prices rising or falling by 10-30; the PS market remains stable with some increases of 50-100; ABS continues to increase by 50-150; EVA sees some slight increases of 100-200. In terms of engineering materials, the PC market continues to rise, with some increases of 50-700; PET prices are rising, with some increases of 40-70; PMMA, POM, PBT, and PA6 remain stable overall.

General material

PE: Supported by news, prices continue to operate at a high level.

1. Today's Summary

2. Spot Overview

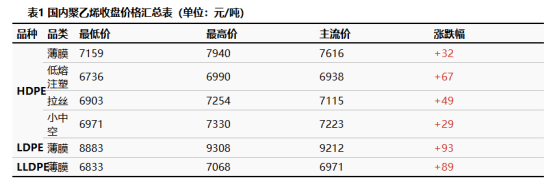

Due to the high costs of pre-sale delivery resources in the previous period, market vendors continue to adopt high quotation strategies. However, downstream buyers are cautious in their purchasing attitudes, with transactions mainly involving negotiations and bargaining. Specifically, the price fluctuation in the HDPE market ranges from 30 to 94 yuan/ton, the LDPE market price increased by 164 yuan/ton, and the LLDPE market price increased by 93 yuan/ton.

3. Price Prediction

In the short term, pre-sales before the Spring Festival are still ongoing, and they are intertwined with pre-sale orders for February, with a noticeable price difference. However, the overall shift in trading focus has strengthened production companies' confidence in scheduling production, and the industry's overall load remains stable. In the short term, there are no new facilities being put into operation to increase production, keeping social inventory pressure manageable. Merchants are likely to maintain a high quotation mentality. Considering that today's high-level transactions were obstructed, it is expected that tomorrow's polyethylene price increase will be limited, and it is likely to maintain a high-level operation trend.

PVC: Demand is dominated by sluggishness, with short-term export expectations under pressure.

1. Today's Summary

2. Spot Overview

Based on the East China Changzhou market, today's cash on delivery price for calcium carbide method Type 5 PVC in the East China region is 4,660 yuan/ton, a decrease of 10 yuan/ton compared to the previous trading day. The current domestic PVC spot market is sluggish, with cautious attitudes from end purchasers. The market prices are weakly fluctuating, and the focus of spot prices is shifting downwards to seek transactions. Due to limited improvement in the supply-demand pattern, industry inventory continues to accumulate, with the price range for calcium carbide method Type 5 PVC in East China between 4,600-4,720 yuan/ton, and the price range for ethylene method PVC between 4,750-5,000 yuan/ton.

3. Price Prediction

The operating rate of PVC production enterprises remains high, and overall supply is steadily increasing. Affected by the industry's off-season and insufficient downstream orders, terminal procurement demand is sluggish, and export growth has not met expectations. The industry still faces inventory pressure. Coupled with temporarily stable cost support, the spot market is expected to maintain a weak adjustment trend within a range. The price of acetylene-based type 5 in East China is likely to fluctuate in the range of 4600-4700 yuan/ton.

PS: Driven by the strengthening of the cost side, the market is stable with localized increases.

1. Today's Summary

2. Spot Overview

Today, the GPPS market price in East China remains at 7500 yuan/ton. The price of raw material styrene is fluctuating upwards, providing strong cost support to the PS market. The supply of goods in the industry is relatively ample, but some supplies are following the trend to slightly increase prices. Downstream purchasing is mainly based on rigid demand. Market activity has become more lively with the price increase, but overall transaction performance is average after the price rise.

3. Price Forecast

The raw material styrene market is expected to maintain a relatively strong consolidation trend, with cost support expected to persist. Market holders are likely to continue to follow up with price increases. However, downstream buying interest in chasing higher prices is mild, primarily focusing on just-in-time procurement. It is expected that the PS market will maintain a relatively strong consolidation pattern in the short term.

ABS: Manufacturers Raise Ex-factory Prices, Market Follow-up Trend Continues

1. Today's Summary

2. Spot Overview

Today, based on the regions of Yuyao and Dongguan, the ABS market prices in East China and South China have simultaneously risen. Trade transactions are performing reasonably well, with Shandong Lihuayi raising its ex-factory prices, and the major sales regions of PetroChina increasing their listed prices, driving market prices to continue rising, and trade transactions to increase in volume.

3. Price Forecast

Based on the regions of Yuyao and Dongguan, it is expected that the ABS market prices in East China and South China will maintain a strong trend. Today's market saw an increase in transactions and manufacturers continued to raise factory prices. It is anticipated that tomorrow some manufacturers will continue the trend of raising factory quotations, and the overall market trend is expected to remain strong.

EVA: High-level consolidation, slight increase in some grades.

1. Market Overview

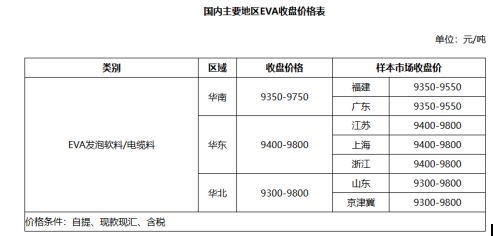

Today, the EVA market price is consolidating at high levels, with prices of some grades rising slightly. Baofeng has continuously raised its ex-factory prices, effectively boosting market confidence. The replenishment activities by traders for open positions provide some support for demand. However, the demand from downstream enterprises remains lackluster, and high-priced sources face significant resistance in transactions.

In the South China market, the mainstream transaction price range for EVA in the South China region today is 9,300-9,750 yuan/ton, with prices of certain grades rising compared to the previous trading day. Traders are offering firm prices, and spot inventory is at a low level. Short covering is boosting demand. End-user enterprises are mostly adopting a wait-and-see attitude, purchasing mainly based on immediate needs, and actual transaction prices need to be negotiated on a case-by-case basis.

In the East China market: Today, the mainstream transaction price range for EVA in the East China region is 9,400-9,800 yuan/ton, with prices for some grades rising by 100-200 yuan/ton compared to the previous trading day. Spot inventory is relatively low, and some traders are holding off on sales in anticipation of price increases. Downstream companies are cautiously observing the market, purchasing only as needed, with actual transaction prices determined through negotiation.

2. Market Forecast

The EVA market price is expected to remain in a stalemate and consolidate in the near future.

Engineering Materials

PC: The tight spot supply continues, and the market is steadily rising.

1. Market Overview

The domestic PC market continued its upward trend today. In the Yuyao market, the mainstream price range for domestic PC supplies was 11,550-12,300 yuan/ton, up 25 yuan/ton compared to the previous trading day. In the Dongguan market, the mainstream price range for domestic PC supplies was 11,900-12,800 yuan/ton, up 50 yuan/ton from the previous trading day. For foreign brands, prices for certain grades increased; the mainstream price range for Yuyao Lotte 1100 was 12,200-12,300 yuan/ton, up 100 yuan/ton from the previous trading day. The mainstream price range for Dongguan Covestro 2805 was 14,900-15,000 yuan/ton, up 100 yuan/ton from the previous trading day. On the same day, the price of raw material bisphenol A rose slightly, providing limited cost support to the PC market. The current tight supply situation in the market is difficult to alleviate, with some factory orders delayed until mid-to-late February for delivery. Market participants remain optimistic, and PC market offers continue to rise. Although downstream enterprises engaged in some purchasing activities due to bullish sentiment, the market atmosphere slightly receded compared to the beginning of the week.

Yuyao Market: Today, the Yuyao PC market has risen. The mainstream price range for Covestro 2805 is 14,900-15,000 yuan/ton, up 100 yuan/ton compared to the previous trading day. The mainstream price range for Lotte 1100 is 12,200-12,300 yuan/ton, also up 100 yuan/ton compared to the previous trading day. The mainstream price range for domestic PC supplies is 11,550-12,300 yuan/ton, up 25 yuan/ton compared to the previous trading day. Some offers continued to rise during the day, but the downstream enthusiasm for chasing the increase slightly declined, and the market's new order transaction volume decreased slightly, though overall performance was still acceptable. Today's collected samples all comply with the methodology collection principles, with no exclusions.

Dongguan Market: Today, the Dongguan PC market has risen. The main price range for Covestro 2805 is 14,900-15,000 yuan/ton, up 100 yuan/ton compared to the previous trading day. The main price range for Lotte 1100 is 12,300-12,400 yuan/ton, up 100 yuan/ton compared to the previous trading day. The main price range for domestic PC sources is 11,900-12,800 yuan/ton, up 50 yuan/ton compared to the previous trading day. Sellers slightly raised their offers for the day, and some downstream companies engaged in early procurement due to bullish sentiment, resulting in a moderate trading atmosphere for new orders in the market. The samples collected today all comply with the methodological collection principles, with no exclusions.

3. Market Forecast

The PC market is expected to rise slightly in the near future.

PET: Dual Support from Cost and Supply, Prices Fluctuate Upward

1. Today's Summary

2. Spot Overview

As a benchmark for the East China region, today's spot price for polyester bottle-grade PET closed at 6,150 RMB/ton, up 50 RMB/ton from the previous trading day, meeting morning expectations. The continuous rise in international crude oil prices has fueled excitement in the commodity market, coupled with a reduction in industry supply, jointly pushing up the focus of the polyester PET market. Factory quotes have generally increased by 40-80 RMB/ton. Market prices surged significantly in the morning and showed a slight decline in the afternoon. It is understood that the transaction price range for January supply is between 6,100-6,170 RMB/ton. Traders are mainly restocking for delivery, while end-use enterprises are only making minimal necessary replenishments, resulting in overall tepid trading. The basis has weakened, with the 2603 contract discounting 10 RMB/ton to a premium of 30 RMB/ton, and the spot processing fee has recovered to around 550 RMB/ton.

3. Price Forecast

The commodity market is resonating upwards, with significant support from the raw materials side, combined with continued contraction in industry supply. It is expected that the polyester bottle chip market will maintain a relatively strong and volatile operating pattern. Tomorrow, the spot price of polyester bottle chips for water bottles in the East China region is likely to fluctuate in the range of 6100-6250 yuan/ton. Special attention should be paid to changes in local geopolitical situations.

PMMA: Prices remain stable, downstream purchasing intentions improve.

1. Today's mainstream market price

2. Market Overview

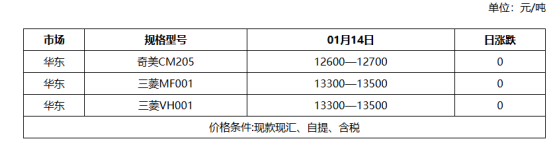

The main intention price range for PMMA Chimei CM205 in the East China market today is 12,600-12,700 yuan/ton, remaining unchanged from the previous trading day. In terms of raw materials, major factories in the Shandong market have raised their quotations, with the market operating rate remaining stable and a reduction in some spot supplies. Overall, market inquiries have increased, downstream purchasing intentions have improved, and transaction prices follow the market trend. Today's collected samples all comply with the principles of the methodology collection, with no exclusions.

POM: Low manufacturer inventory support, market transactions mainly driven by just-in-time demand.

1. Today's Summary

2. Spot Overview

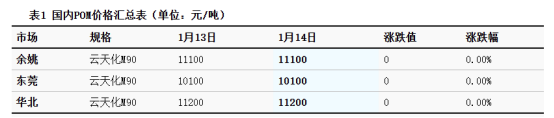

Based on the Yuyao region, the price of Yun Tianhua M90 closed at 11,100 yuan/ton today, remaining unchanged from the previous period. The domestic POM market maintained a stable and weak trend today, with fundamental support still present, and petrochemical companies continuing their intention to hold prices firm. However, the operating load of end factories is at a low level, demand orders are weak, and some traders have relatively flexible bargaining space, resulting in a sluggish market. As of the close, the tax-inclusive quotation range for domestic POM in the Yuyao region is 8,800-11,300 yuan/ton, and the cash transaction price range in the Dongguan region is 7,800-10,400 yuan/ton.

3. Price Forecast

The current fundamental guidance information is limited, and inquiries in markets across various regions have diminished, leading to heightened wait-and-see sentiment. In the short term, the market continues to intend to maintain prices, with the supply side showing relatively stable trends. Although petrochemical companies' inventories are low, some traders have inventory backlog issues, and downstream users have limited purchasing capacity. Merchants may appropriately expand their concession space to promote transactions. Longzhong Information predicts that the POM market will exhibit a volatile consolidation trend in the short term.

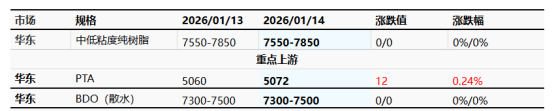

PBT: Cost support continues, market maintains stable price operation.

1. Today's Summary

2. Spot Overview

Taking the East China region as the benchmark, the mainstream price range for medium and low viscosity PBT resin today is 7550-7850 yuan/ton, remaining unchanged from the previous trading day. The PBT market is maintaining a temporarily stable and stalemated stance today, with the raw material side seeing a narrow consolidation in the PTA market and continued stalemate in the BDO market. Supported by cost factors, the PBT market is continuing with stable pricing operations, while positive trends in the macroeconomic and crude oil markets are providing favorable sentiment for the market. According to Longzhong Information, the transaction price range for medium and low viscosity PBT pure resin in the East China market is 7550-7850 yuan/ton.

3. Price Forecasting

The PBT market is expected to maintain a wait-and-see stance. On the raw material side, the PTA supply has slightly decreased, but there is an expectation of reduced polyester load, with insufficient demand support. The market lacks substantial drivers, and downstream purchasing enthusiasm is limited. In the short term, the PTA spot market is expected to remain weak. BDO supply support is generally moderate, with downstream industries primarily focusing on digesting inventory or following just-in-time contracts. Holders have a cautiously bearish view of the future market, with trading activity remaining light and stable. More information should be watched for any developments. The cost side is expected to continue running at a high level, providing some support to the PBT market. The focus of negotiations will remain within a fluctuating range. Therefore, Longzhong Information anticipates that the price range for medium-to-low viscosity PBT resin in the East China market will remain at 7,550-7,850 yuan/ton tomorrow.

PA6: Trading Atmosphere Warms Up, Market Adjusts and Operates

1. Today's Summary

2. Spot Overview

Today, the polyamide 6 (PA6) market maintains a consolidation trend. The raw material market has seen a slight decline, while polymerization companies, supported by cost pressures, keep their quotations firm. Downstream companies are entering the market to restock at lower prices, improving the market transaction atmosphere, with actual orders subject to negotiation. In terms of pricing, the cash short delivery price range for regular spinning standard grades in the East China region is 9,400-9,800 yuan/ton, and the current spot acceptance delivery price range for high-speed spinning is 9,900-10,200 yuan/ton.

3. Price Prediction

From the cost perspective, the price of upstream pure benzene is rising, the caprolactam market is experiencing ample supply and weak operation, and chip manufacturers are still facing pressure from losses. From the supply and demand perspective, market supply is expected to increase, downstream enterprises mainly replenish on a need-only basis when prices are low, and the sales situation of polymerization enterprises is improving. It is expected that the PA6 market will show a slightly favorable trend in the near future.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Supply Extremely Tight! LG Chem Declares Force Majeure on Export Contracts for Di-Octyl Terephthalate (DOTP)

-

Huntsman Introduces “War Surcharge” Amid Shipping Disruption and Soaring Energy Costs, Global MDI Prices Continue to Rise

-

Middle East Tensions Escalate Sharply: How Polyolefins Respond Amid Soaring Risk Premium

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

LG Chem Declares Force Majeure on DOTP Exports! SABIC Joins Five Giants to Redefine EV Safety